- Scrap imports may cross 1 mnt amid relaxed norms

- Move to aid shift from BF to lower-emission EAF route

China will relax restrictions on metal scrap imports starting in August, including easing quality standards for steel scrap and allowing shipments of battery recycling residue known as “black mass”, the government announced Monday.

The move supports China’s broader decarbonisation goals, aiming to reduce reliance on overseas iron ore and promote greener production methods. Looser scrap import norms — first introduced in 2021 — are expected to accelerate the shift towards electric arc furnace (EAF)-based steelmaking. The steel industry, responsible for nearly 15% of China’s total carbon emissions, is now covered under the national carbon trading market.

In parallel, imports of black mass will be permitted from both lithium iron phosphate (LFP) and nickel/cobalt battery chemistries. Although China is the world’s largest producer of EV batteries and processor of black mass — a powder rich in lithium, cobalt, and nickel — recyclers face low utilisation due to chronic domestic overcapacity. Strict quality standards may still limit the volume of qualifying shipments.

Possible impact:

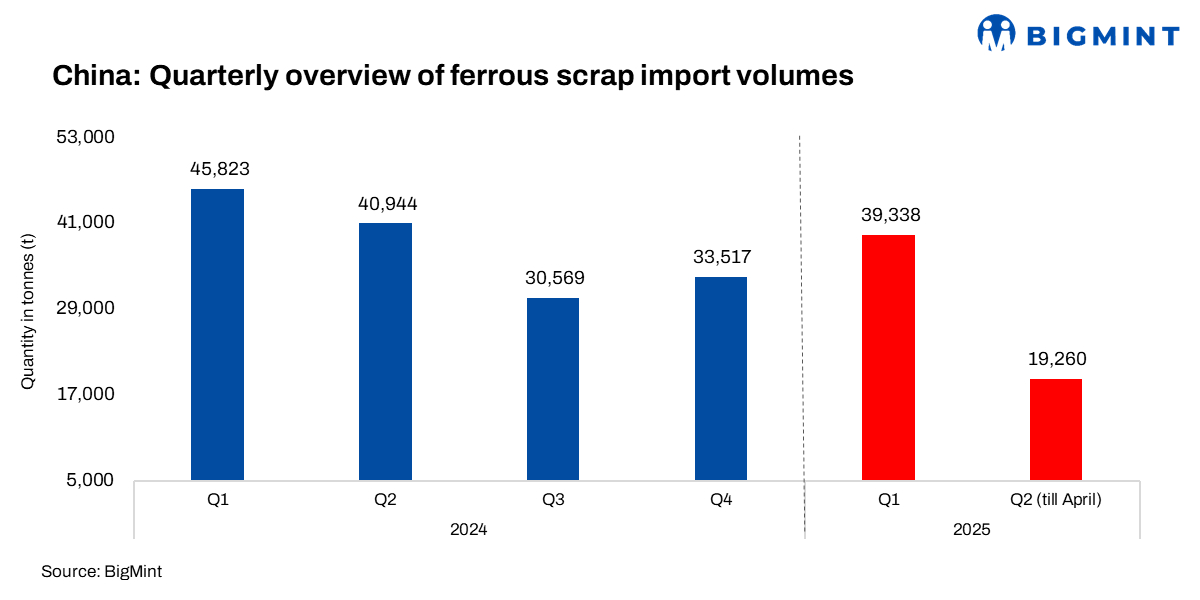

As per market insiders, China’s steel scrap imports could exceed 1 million tonnes (mnt) annually, rising sharply from under 200,000 t in 2024, driven by relaxed import rules.

While a positive step for greener steelmaking, the volume remains modest compared to the 1.2 billion tonnes (bnt) of iron ore imported last year — most of which fed traditional, high-emission blast furnaces.

Wider market indicators:

Iron ore prices are nearing their lowest since September amid seasonal demand weakness and signs of production cuts at Chinese steel mills.

- Weaker iron ore demand due to lower steel production and slow construction activity signals a general softening in steel demand. This also puts downward pressure on scrap consumption, particularly in electric arc furnaces (EAFs), which rely heavily on scrap.

Meanwhile, Goldman Sachs projects new home demand to remain 70-75% below the 2017 peak in the coming years, reflecting persistent weakness in the real estate sector.

Meanwhile, Goldman Sachs projects new home demand to remain 70-75% below the 2017 peak in the coming years, reflecting persistent weakness in the real estate sector.

- Sluggish real estate demand directly affects steel consumption, especially for long products like rebar. With fewer construction projects, mills reduce output, which in turn reduces scrap demand–whether imported or domestic.

Outlook

Looking ahead, even if China ramps up its scrap imports, the change is likely to be marginal when stacked against the country’s massive annual steel output. China boasts being the largest scrap consumer with over 220 mnt in 2024; the overall market equation is not expected to shift dramatically anytime soon. For now, this looks more like a supportive tweak than a game-changer.

Leave a Reply