- OMC cuts base prices for upcoming iron ore auction

- Active pre-monsoon restocking supports offers

Iron ore concentrate price tags in India’s Jabalpur remained stable this week. Active trades ahead of the heavy monsoon season have helped support iron ore concentrate prices. However, the recent drop in base prices of the Odisha Mining Corporation (OMC), coupled with declining sponge iron and steel tags and continued volatility in the pellet and iron ore markets, has added downward pressure – making the near-term price outlook increasingly uncertain.

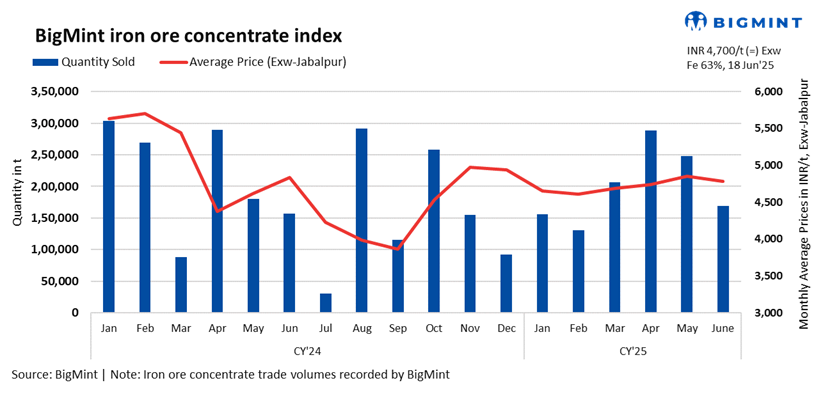

BigMint’s weekly iron ore concentrate index was assessed at around INR 4,700/tonne (t) ($54/t) exw-Jabalpur, stable as against the last assessment on 14 June 2025. Meanwhile, the market is closely watching the outcome of OMC’s upcoming iron ore auction, which is expected to offer clearer insights into the direction of future price trends.

Rationale

- Three (3) trades of 42,000 t were recorded in the publishing window, and all were taken into consideration, receiving 50% weightage.

- Nine (9) offers and indicative prices were observed, of which seven (7) were taken into consideration as T2 trades, which received the balance 50% weightage.

What’s driving pressure on concentrate prices?

- OMC reduces base prices for Jun’25 iron ore auction: OMC has scheduled an iron ore auction on 19 June, offering 2.05 million tonnes (mnt), including 0.98 mnt of lumps and 1.07 mnt of fines. The miner has reduced base prices by INR 500-700/t ($6-8/t) for fines and INR 500/t ($6/t) for lumps compared to the previous month. The reduction comes in response to a sharp decline in pellet and sponge iron prices across central and eastern India.

- Sponge PDRI prices drop w-o-w: Sponge PDRI prices in Raipur decreased by around INR 400/t ($5/t) w-o-w on 18 June. Sponge iron prices declined primarily due to the continued weakness in both semi-finished and finished steel markets, driven by subdued demand. Sluggish offtake in downstream segments, including construction and infrastructure, led to lower steel prices, which in turn reduced procurement appetite for sponge iron. As a result, sponge manufacturers faced margin pressure, prompting price corrections to stay competitive and align with prevailing market dynamics.

- Subdued steel market sentiments pressure concentrate prices: The semi-finished steel market witnessed a slight decline, as fresh inquiries remained subdued. Demand weakened across both semi-finished and finished steel segments, with buyers largely staying on the sidelines after having secured adequate volumes in recent days. BigMint’s daily billet index decreased significantly by INR 600/t ($6/t) w-o-w on 18 June 2025.

Outlook

Market participants are adopting a cautious stance, awaiting clearer pricing cues or signs of recovery across the steel, iron ore, and pellet markets. Although pre-monsoon restocking has lent some support to offers, a more definitive trend is expected to emerge following the outcome of the OMC auction.

Leave a Reply