- Sellers face pressure to clear stocks before quarter-end

- HRC export index falls $15/t w-o-w on weak EU demand

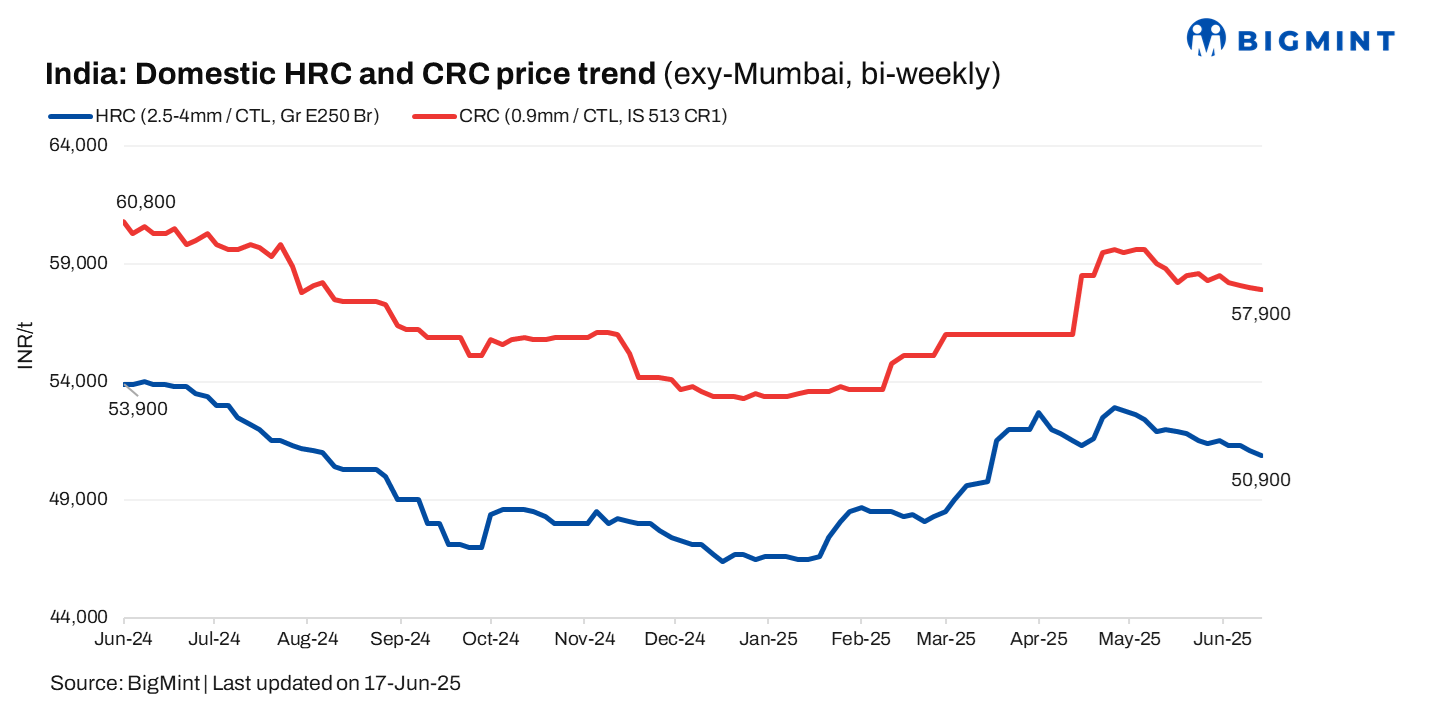

Trade-level prices of hot-rolled coils (HRCs) in India declined marginally by up to INR 500/tonne (t) w-o-w to INR 50,900-52,900/t ($596-616/t) across markets. Meanwhile, cold-rolled coil (CRC) prices remained range-bound w-o-w at INR 57,000-60,900/t ($659-718/t).

Market speculation suggested that a particular mill offered a rebate of INR 1,000/t for the previous month, and this adjusted pricing might continue into the current month. However, this information could not be confirmed directly with the mill.

BigMint’s benchmark assessment (bi-weekly) for HRCs (IS2062, Gr E250, 2.5-8 mm/CTL) dropped by INR 500/t w-o-w to INR 50,900/t ($601/t) on 17 June 2025. Additionally, CRC (IS513, Gr O, 0.9 mm/CTL) prices declined by INR 200/t ($1/t) w-o-w to INR 58,100/t ($684t). These prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

Market updates

Market faces demand slowdown: Distributors experienced weaker demand, with a decline in inquiries and even slower conversion to actual sales. Purchases were limited and need-based, often in smaller quantities. As the quarter-end approaches, there is increased pressure to clear inventory and manage capital rotation efficiently.

“The market expects mills to offer price support soon; if not, the trade segment may incur significant losses. Meanwhile, the supply of CRCs is improving due to increased production from mills,” a market participant noted.

Economic indicators point to bearish trends: The Purchasing Managers’ Index (PMI) declined for the third straight month to 57.6 in May 2025, signalling a gradual slowdown in manufacturing and services activity.

Meanwhile, apparent steel consumption fell to 10.93 mnt in April from 12.96 mnt in March, indicating weakening demand.

Import volumes: India’s bulk imports of HRCs and plates touched 117,381 t as of 16 June, based on vessel line-up data from BigMint. Around 106,060 t of additional cargo are expected by the month-end.

Export trends: BigMint’s India HRC (S275) export index fell by $15/t w-o-w to $555/t FOB East India, as EU demand remained weak due to sluggish automotive and construction activity. Trade also slowed because of the Corpus Christi holidays. Meanwhile, Indian mills held back HRC offers to the Middle East amid stiff competition from other regions.

Outlook

The near-term outlook for Indian flat steel prices, particularly for HRCs and CRCs, suggests continued downward pressure or range-bound stability, primarily driven by weak domestic demand and challenging export conditions.

Leave a Reply