- HRC, CRC prices drop by INR 300-500/t w-o-w

- IF rebar prices recover as mill inventory levels fall

- Primary mills may roll over or reduce flat steel prices for Dec’25

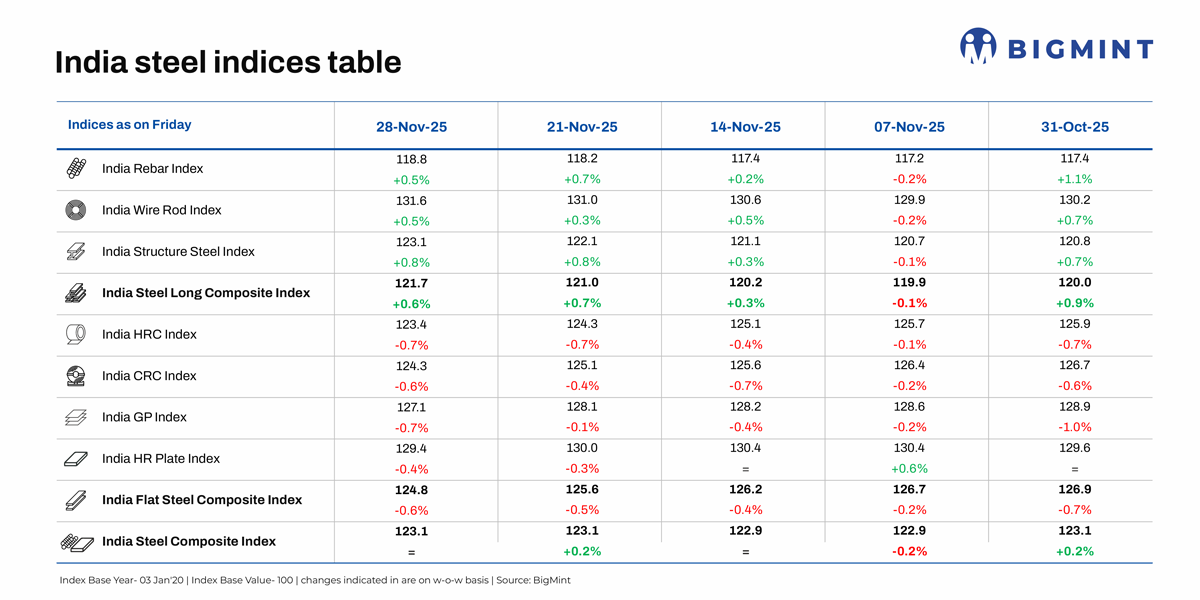

Morning Brief: BigMint’s India steel composite index, a barometer of steel market movements in the country, remained flat w-o-w, as assessed last on 28 November 2025, with steel prices in different regions of the country remaining under pressure.

However, induction furnace (IF)-based long steel prices witnessed a recovery in certain key regions, which propped up the longs composite index while the flats index edged down by 0.6% w-o-w. Any real improvement in market conditions is not yet discernible after an anticipated post-festive improvement in prices failed to materialise and hikes by the primary mills were ill-absorbed by trade market participants.

Highlights of steel price movements

HRC market weakens: BigMint’s benchmark assessment (bi-weekly) for HRCs (IS2062, Gr E250, 2.5-8 mm/CTL) dropped by INR 300/t ($3/t) w-o-w to INR 46,200/t ($518/t) on 24 November against INR 46,500 ($521/t) on 18 November. CRC (IS513, Gr O, 0.9 mm/CTL) prices decreased by INR 500/t ($6/t) w-o-w to INR 54,300/t ($609/t). These prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

Domestic HRC market sentiments were muted as demand remained moderate, but oversupply and high inventory levels weighed on sentiment. Incidentally, the government’s decision to suspend BIS norms for certain segments of steel product imports into the country is expected to lead to higher supplies in the domestic market which is inconducive to a price recovery. Buyers are delaying purchases, anticipating December’s price revision and expecting further price declines amid excess availability and weak overall demand.

Demand pull lifts IF rebar: IF-origin rebar prices recorded an increase across major markets supported by a moderate improvement in material lifting and reduced inventory pressure at mills. Fresh bookings and firm semi-finished steel prices further aided the upward trend. Sentiments remain positive, with expectations of continued price improvement in the near term. IF rebar prices inched up by INR 100/t ($1/t) w-o-w to INR 42,800/t ($478/t) exw-Mumbai on 28 November.

However, muted trading activity across markets, with sellers offering discounts to clear inventories, and surplus material in the trade channel intensified pressure on BF rebar prices, market sources indicated. Prices fell to a five-year low as rising production from the primary mills in October was not absorbed due to low demand leading to an inventory buildup.

Outlook

The steel composite index had gained 0.2% on-week the week before last but failed to carry that positive tempo into December. The market is prepared for a fresh round of list price announcements by the primary mills which, by the look of things, point to the possibility of a reduction or rollover at best.

Soft demand, elevated inventories and liquidity constraints are curbing buying interest and the global steel market slowdown, especially declining production in the major economies except the US, is obviously weighing on domestic market sentiment.

Leave a Reply