- Cheaper Asian billet restricted upside for GCC producers

- Turkish rebar strength continued pulling global billet prices higher

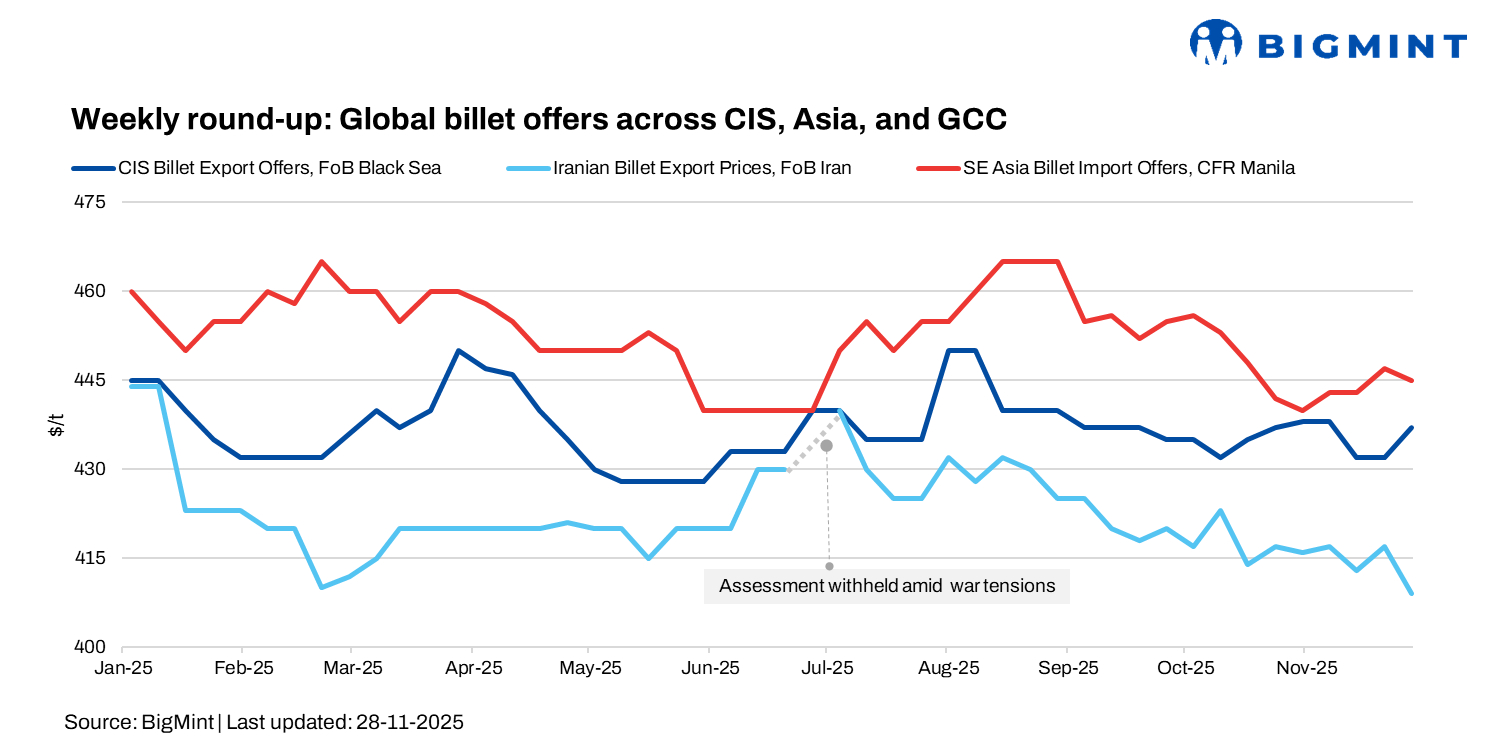

Global billet and scrap markets strengthened in the week ended 28 Nov, driven by firmer rebar sentiment, tightening supply, and steady buying interest across Turkiye, Asia, and the GCC. Suppliers in the Black Sea, CIS, and Asia raised offers, with several regions securing solid bookings despite uneven demand.

Turkiye’s imported scrap market stayed firm, supported by better rebar demand and tight availability. US-origin HMS 80:20 traded at between $361-364/t CFR, while EU cargoes moved at between $356-358/t CFR, with limited supply and firm freight keeping offers elevated.

Black Sea and CIS market

CIS billet suppliers entered the week with renewed confidence as firmer Turkish rebar prices, stronger scrap, and a rising rouble pushed export offers higher. Russian mills lifted prices to $440-450/t FOB Black Sea, supported by tight mid-January availability.

Turkiye’s billet market also strengthened, with both domestic and imported offers rising in line with improved rebar sentiment. Kardemir raised prices by $15/t from its last round, selling roughly 45,000 t almost immediately at $515-525/t exw — effectively $510-520/t exw after some bulk-buyer discount.

Other Turkish mills aligned at $515-520/t exw, up from $510-515/t last week. In imports, CIS-origin billet offers firmed to $455-460/t CFR, leaving buyers divided between accepting the uptrend and resisting the sharp weekly increase. Far Eastern Russian suppliers sold over 25,000 t at $420/t FOB, while Chinese semis hovered near $470/t CFR.

Asian billet market

Asia’s billet market moved unevenly, driven more by sentiment than strong downstream demand. Chinese mills lifted offers slightly to $435/t FOB, supported by firmer domestic prices and positive futures, with recent trades to the UAE at $458-460/t CFR reinforcing their competitiveness. Indonesian Dexin held steady at $430-432/t FOB, focusing on volume rather than price — reportedly selling 50,000- 55,000 t to Turkiye.

Southeast Asia saw workable levels inch up; the Philippines moved to $445-450/t CFR, while bids across Vietnam and Indonesia hovered below offers at $450-455/t CFR, cautious buying amid a still-soft economic backdrop.

In Taiwan, weakened construction activity kept billet demand low, with cheap Chinese and Russian offers at $445-440/t CFR weighing on sentiment.

China’s domestic market

Chinese billet prices edged up by RMB 30/t ($4/t) to RMB 2,980/t ($421/t) in the week ended on 28 Nov, supported by tight supply, steady costs, and stable iron ore. Slightly better coated billet demand and a four-month low in social inventories added mild support, though overall momentum stayed limited.

SHFE rebar futures also rose by RMB 53/t ($8/t) to RMB 3,110/t ($440/t), but export activity slowed–particularly for HRC and coated products—keeping sentiment cautious as the market entered a seasonally weak December and awaited policy cues.

Iranian market

Iran’s billet export market is facing structural disruption rather than price weakness. New controls on commercial-card usage and the phased rollout of the secondary exchange mechanism hindered traders’ ability to confirm offers, limiting exports to mills with cleared foreign exchange obligations. This regulatory shift sharply reduced liquidity and complicated price discovery.

Despite this, indicative levels held steady, two steel mills sold billet at $414/t and $405-410/t FOB, respectively, and small lots were booked at $400/t FOB. With only factories formally allowed to export and most facing administrative delays, the market is in a holding pattern — high uncertainty, tight availability, and upward cost pressure.

Middle East (GCC) market

The GCC billet segment saw improved trading activity, but pricing remained capped by Asian competition. Chinese suppliers secured a sizeable 50,000 t booking at $458/t CFR, undercutting GCC mills, whose recent deals closed around $480-485/t CFR/CPT — well below their target levels.

While Qatari and Omani producers sold out December tonnage, margins remain squeezed, pushing mills to prioritise rebar production over billet sales. Domestic rebar demand in the region is firm, but cheaper billet inflows continue to limit the room for upward adjustment. In the wider MENA region, Turkish mills lifted rebar to $570-600/t exw, supported by scrap and domestic buying, though exports remain lethargic with workable levels near $560/t FOB.

Leave a Reply