- ICSG cuts 2025 global mine supply growth forecast to 1.4%

- 2025 demand forecast unchanged, expected to grow 3%

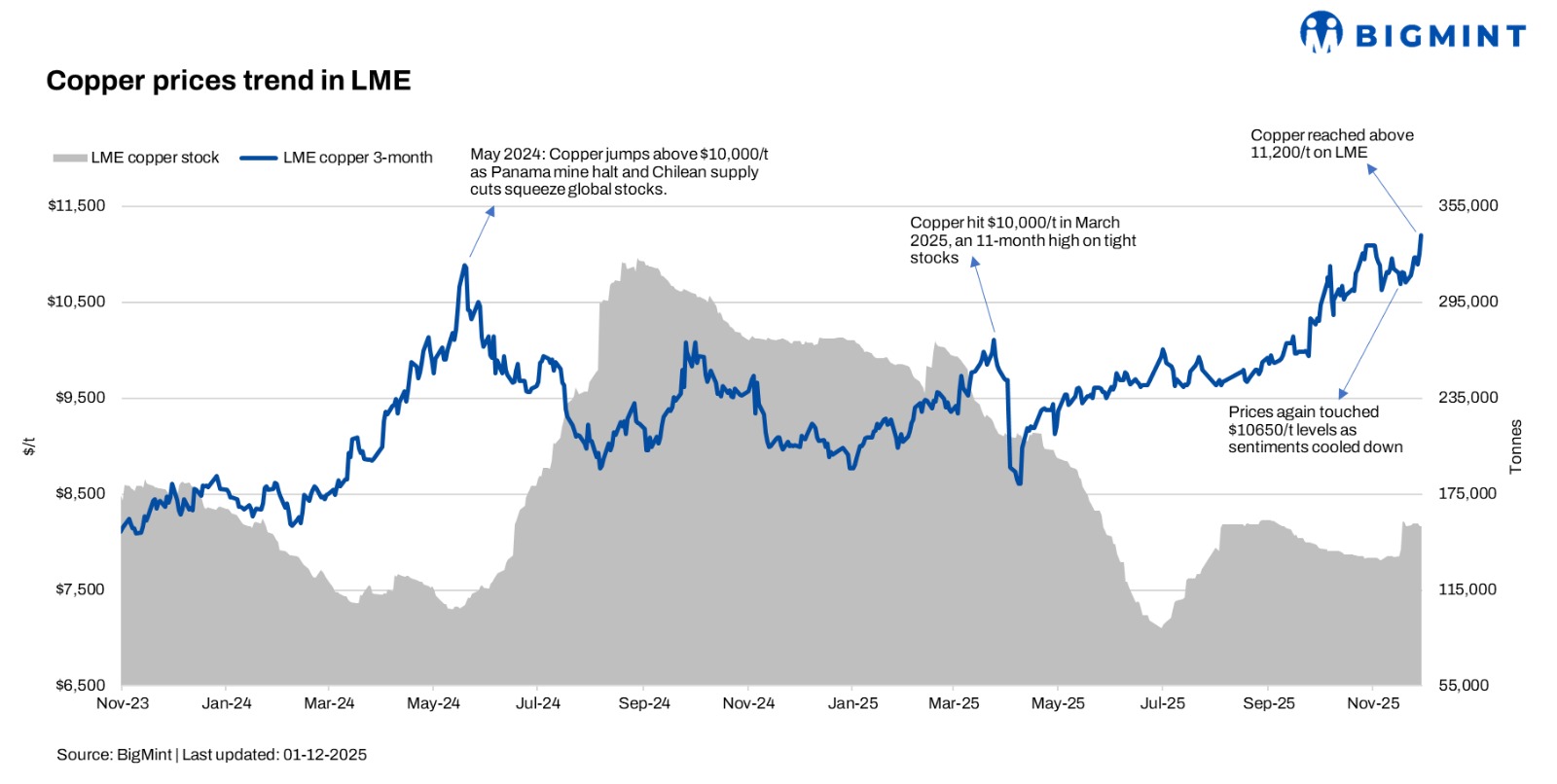

LME copper prices climbed sharply w-o-w, rising from around $10,700/t on 21 November to nearly $11,200/t on 29 November — a solid 4.7% increase.

LME stocks, meanwhile, remained broadly steady to slightly lower during the same period, holding near 156,000 t.

The latest market signals strongly justify copper’s upward momentum on the LME, with structural and short-term fundamentals both pushing prices higher. The International Copper Study Group (ICSG) has sharply cut its 2025 global mine supply growth forecast to just 1.4%, down from 2.3% earlier. Meanwhile, global demand is still expected to grow close to 3%, immediately widening the expected deficit in 2025. This downgrade alone has lifted bullish sentiment as it reinforces a clear tightening trajectory.

Adding to the squeeze, disruptions at Kamoa-Kakula (DRC), Teck’s Quebrada Blanca and Highland Valley mines, and multiple smaller operations have collectively removed tens of thousands of tonnes from 2025 supply guidance. These unplanned outages directly reduce concentrate availability, tighten refined output, and push investors to price in higher future scarcity.

China’s import-export dynamics also strengthened the rally. Refined copper imports fell sharply in October to 282,000-320,000 t, down 13-20% y-o-y, as high domestic prices discouraged buying. At the same time, China exported over 60,000 t, the highest level in months, because domestic premiums opened an export arbitrage window. More refined metal leaving China — at a time when LME inventories remain low and stable — has added a clear bullish signal to global markets.

The Chinese smelter sector is also squeezing supply. Refined output rose nearly 12% y-o-y in Jan-Sep 2025, but concentrate tightness has become more severe. With TC/RCs hovering near multi-year lows and even turning negative on spot, several top smelters are preparing production cuts of 10% or more heading into early 2026. This means refined output is likely to slow just as demand picks up.

New smelting capacity — including Tongling Nonferrous’s two new plants totalling 800,000 t/y — is ramping up faster than new mine supply. This intensifies competition for concentrate and structurally tightens the refined balance, putting upward pressure on prices even before deficits fully materialise.

On the demand front, global copper consumption is still projected to rise 2.5–3% annually in 2025-26, supported by grid expansion, renewable energy systems, electrification, data centres, AI-driven infrastructure, and EV-related cabling. Because demand growth remains steady and visible, any supply disruption — even small — quickly reinforces the “higher for longer” narrative.

Additionally, macro sentiment has strengthened copper’s move: a softer US dollar, improving PMIs, and expectations of earlier rate cuts have encouraged fund inflows back into commodities.

Overall, the market is now pricing in a structural deficit, tighter refined availability, and improving macro demand — all of which justify copper’s firm rise toward and above the $11,000/t mark on the LME.

Leave a Reply