- US bulk scrap exports to Bangladesh surge by 40% m-o-m

- Sep’25 to see cautiousness continue despite monsoon end

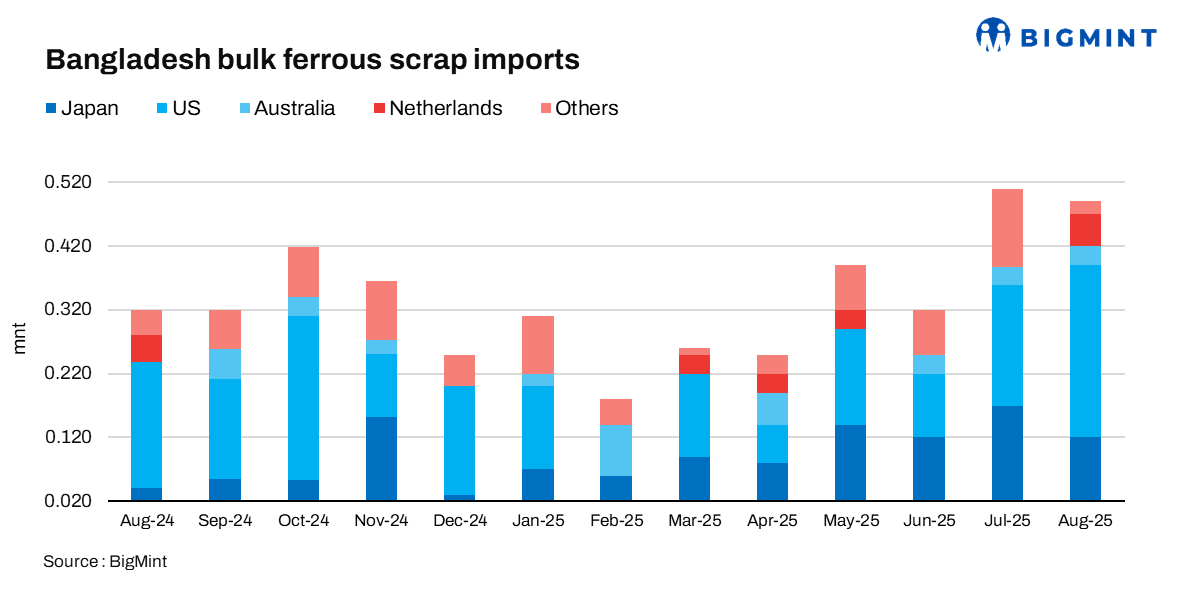

Bangladesh’s total ferrous scrap imports, including bulk and containerised cargoes, rose slightly by 4% to 0.565 million tonnes (mnt) in August 2025 from 0.54 mnt in July. Bulk scrap imports, however, slipped marginally by 4% to 0.49 mnt in August from 0.51 mnt in July.

Factors driving scrap imports

Suppliers remained cautious throughout the month, avoiding large-volume sales due to delayed mill payments and tight liquidity. Slow banking responses to financing needs added to cash flow pressures, while some buyers faced letter of credit (LC) related challenges, further limiting trade activity.

Persistent heavy rains continued to disrupt construction and suppress finished steel demand. Mills maintained a cautious approach, refraining from major bookings and closely monitoring end-user demand trends.

- Bulk HMS 80:20 offers in August rose slightly by $2/t m-o-m to $354/t CFR from $352/t in July.

- Japan’s H2 scrap offers held steady at $342/t CFR, unchanged from July.

- European-origin HMS (80:20) prices were down $1/t m-o-m to $354/t.

- European-origin containerised shredded inched up by $3/t m-o-m to $374/t.

Currency appreciates slightly: The Bangladeshi taka strengthened slightly, averaging 121.6/USD in August, compared to 122.25/USD in July.

Country-wise bulk scrap exporters

The US and Japan remained the top exporters to Bangladesh, supplying the majority of bulk scrap volumes.

- US: Imports from the US surged 40% m-o-m to 270,000 t in August, from 190,000 t in July, and 34% y-o-y from 200,000 t in August 2024.

- Japan: Shipments from Japan climbed up by 47% m-o-m to 175,171 t while more than doubling compared to 84,772 t in August 2024.

- New Zealand: Imports from New Zealand more than doubled to 50,000 t from 30,000 t in July, with no shipments recorded in August 2024.

- Australia: Imports from Australia remained stable m-o-m at 30,000 t, while no shipments were recorded in August 2024.

Ship-breaking market weakens sharply in Aug’25

Ship demolition activity slowed in August, with total tonnage down 57% m-o-m to 43,830 LDT from July’s 101,179 LDT. Bangladesh also slipped 8% in terms of the number of units demolished, to 11 units from 12.

Outlook

Bangladesh’s steel and scrap market is likely to see cautious activity in September, though the end of the monsoon is expected to bring some improvement in construction demand. Mills may stick to limited bookings as liquidity concerns and currency fluctuations persist, keeping price sentiment under pressure. Seasonal demand recovery and possible government policy clarity could lend support, but a significant rebound in scrap prices remains unlikely in the immediate term.

Leave a Reply