- BDI extends losses for third session

- Supramax hits highest since Aug’22

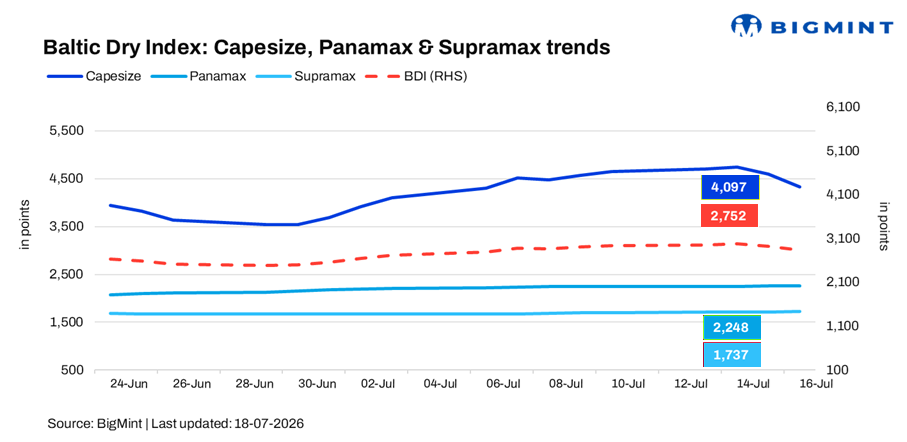

The Baltic Exchange Dry Bulk Index (BDI) extended its losses for a third consecutive session on 17 July 2026, declining by nearly 3% (88 points) d-o-d to 2,752 points, its lowest level in two weeks.

The decline reflected weaker sentiment across the dry bulk market, primarily weighed down by softer Capesize earnings and easing cargo activity on key trading routes.

Segment-wise performance

- Baltic Capesize Index (BCI): BCI fell 5.1% (242 points) d-o-d to 4,097 points on 17 July 2026, as weaker cargo enquiries and a rise in prompt vessel availability created downward pressure on spot rates. Softer fixture activity, especially in the Pacific basin, further weighed on Capesize earnings.

- Baltic Panamax Index (BPI): BPI slipped marginally by 0.4% (9 points) d-o-d to 2,248 points on 17 July 2026. Compared with the sharper losses in the Capesize segment, Panamax rates remained relatively resilient, supported by stable cargo volumes despite easing market sentiment.

- Baltic Supramax Index (BSI): BSI edged up by 0.4% (7 points) d-o-d to 1,737 points on 17 July 2026, reaching its highest level since August 2022. The gains were supported by healthy regional cargo demand, particularly in the Atlantic basin, and balanced vessel availability, which continued to underpin Supramax earnings.

Outlook

The benchmark index is expected to remain under pressure in the near term as softer Capesize activity, particularly in the Pacific basin, easing iron ore cargo availability, and higher prompt vessel supply weigh on freight sentiment.

However, resilient Atlantic cargo programmes, steady Panamax and Supramax demand, and firm bunker prices may limit further downside. A recovery in iron ore exports from Brazil or Australia, along with stronger coal and grain shipments, could lend support to the index.

Leave a Reply