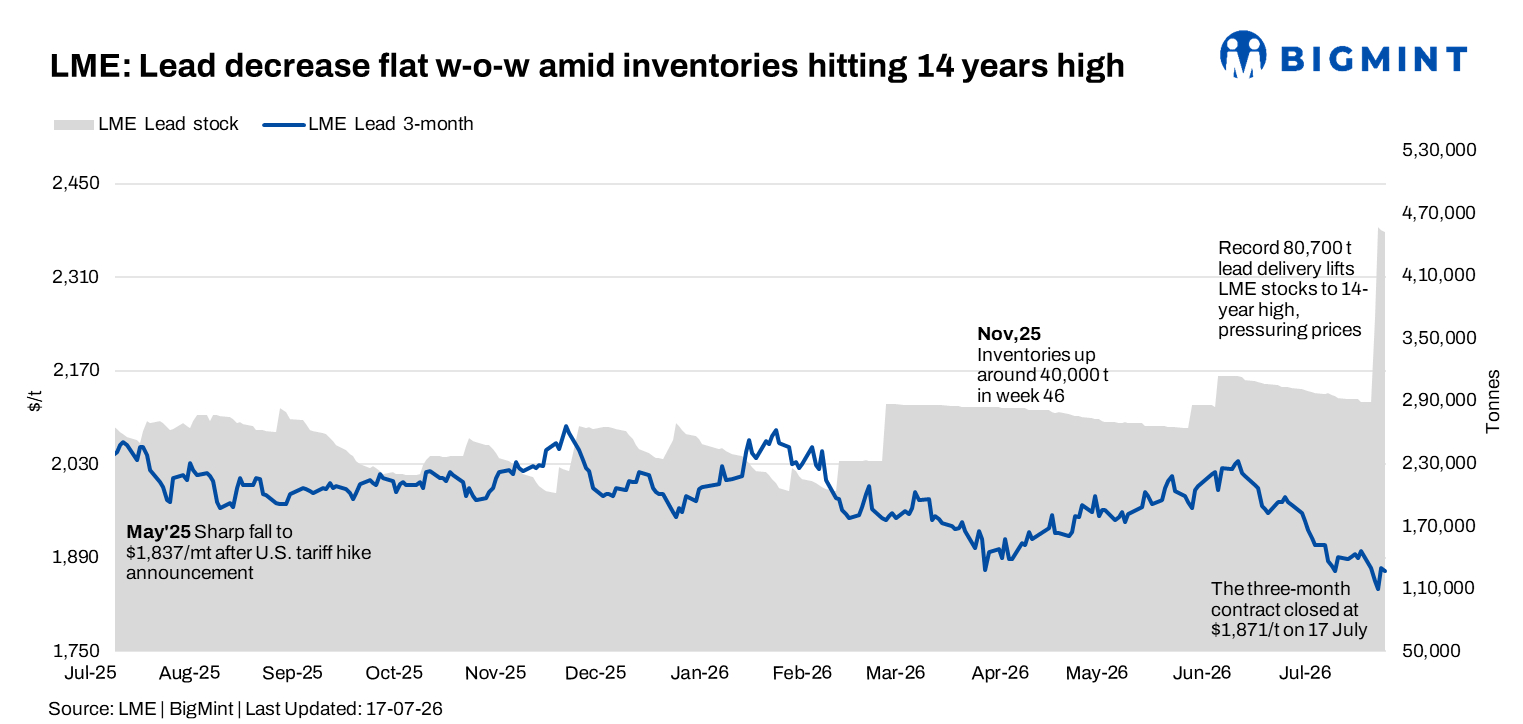

- Record 80,700 t lead delivery lifts LME stocks to 14-year high, pressuring prices

- SHFE lead declines; MCX futures remain resilient despite weekly losses

Lead prices on the London Metal Exchange (LME) weakened during the week ended 17 July 2026, with prices falling to a one-year low amid a sharp increase in exchange inventories. The reported delivery of 80,700 t of lead by Trafigura into LME warehouses lifted inventories to a 14-year high, significantly weighing on market sentiment.

Subdued industrial demand and cautious sentiment across the broader base metals complex added to the pressure, despite a partial recovery in prices towards the end of the week.

On a w-o-w basis, LME cash lead prices declined to $1,821/t on 17 July from $1,851/t on 10 July, marking a fall of $30/t, or around 1.6%. The three-month contract also weakened, closing at $1,871/t on 17 July compared with $1,899.5/t in the previous week.

The sharp increase in LME inventories emerged as the key bearish factor during the week, with stocks rising by 162,700 t w-o-w.

Price trends

LME cash lead prices opened the week at $1,832/t on 13 July, before falling sharply to $1,803/t on 14 July. Prices declined further to $1,797/t on 15 July, marking the lowest level of the week. Lead prices subsequently recovered to $1,828/t on 16 July before easing marginally to close the week at $1,821/t on 17 July.

The three-month contract followed a similar trend. Prices started the week at $1,875/t on 13 July and fell to $1,856/t on 14 July. The contract declined further to $1,843/t on 15 July before recovering to $1,875/t on 16 July. Prices closed the week at $1,871/t on 17 July.

Both contracts continued to trade below the psychological $1,900/t level. The sharp mid-week decline reflected pressure from rising exchange inventories and cautious demand sentiment, although prices recovered modestly in the second half of the week.

Inventory analysis

LME lead inventories recorded a sharp increase during the reporting week, reversing the steady drawdown observed in the previous week.

Exchange stocks stood at 289,375 t on 13 July, before rising sharply to 370,075 t on 14 July. Inventories increased further to 456,575 t on 15 July, before easing slightly to 454,025 t on 16 July and 452,075 t on 17 July.

Overall, LME lead stocks increased by 162,700 t w-o-w, or around 56%, from 289,375 t on 10 July to 452,075 t on 17 July.

The sharp inventory build was reportedly driven in large part by Trafigura delivering a record 80,700 t of lead into LME warehouses, lifting exchange inventories to a 14-year high. The sudden inflow of metal significantly weakened the near-term fundamental outlook and contributed to increased selling pressure in the lead market.

The inventory surge coincided with LME lead prices falling to a one-year low during the week, highlighting the immediate impact of the large warehouse delivery on market sentiment. Although stocks eased marginally during the final two trading sessions, inventories remained significantly higher than the previous week, keeping market participants cautious.

SHFE lead trends

Lead prices on the Shanghai Futures Exchange (SHFE) weakened during the week, reversing the gains recorded in the previous reporting period.

SHFE lead prices opened at $2,239/t on 13 July and edged up marginally to $2,240/t on 14 July. Prices then declined to $2,220/t on 15 July and fell further to $2,216/t on 16 July. The contract closed the week at $2,191/t on 17 July.

Overall, SHFE lead prices declined by $48/t, or around 2.1%, during the week. The decline suggests weakening sentiment in China’s domestic lead market, with softer global prices and cautious downstream demand weighing on buying interest.

MCX lead trends (13-17 July)

On the Multi Commodity Exchange (MCX), lead futures remained relatively resilient despite recording a marginal weekly decline.

The July futures contract settled at INR 199,200/t on 13 July before easing to INR 198,000/t on 14 July. Prices declined further to INR 197,900/t on 15 July, before recovering to INR 199,000/t on both 16 and 17 July.

The contract declined by INR 200/t w-o-w from INR 199,200/t on 13 July to INR 199,000/t on 17 July.

Open interest increased from 521 lots on 13 July to 525 lots on 14 July and 523 lots on 15 July. It then declined to 502 lots on 16 July and further to 484 lots on 17 July.

The combination of a recovery in prices during the second half of the week and a decline in open interest suggests that the recent gains were largely supported by short covering rather than aggressive fresh long additions. Trading volumes remained moderate, with market participants continuing to adopt a cautious approach amid weak global cues.

Market updates

Market sentiment turned sharply bearish during the week as a major inflow of lead into LME warehouses triggered a steep rise in exchange inventories. Trafigura reportedly delivered 80,700 t of lead into LME warehouses, lifting total inventories to a 14-year high and contributing to a sharp decline in lead prices to a one-year low.

LME lead stocks increased by 162,700 t w-o-w, significantly reversing the previous weeks’ warehouse drawdown. The sudden inventory build raised concerns over near-term availability and demand conditions, while also weakening the support that declining stocks had previously provided to prices.

LME cash lead prices fell below $1,800/t during the middle of the week before recovering slightly, but remained well below the psychological $1,900/t level. In China, SHFE lead prices declined during the second half of the week, indicating softer domestic sentiment. Meanwhile, MCX lead futures remained comparatively resilient, recovering from mid-week lows as domestic prices tracked the recovery in overseas markets.

Outlook

BigMint expects LME lead prices to remain under pressure in the near term, with the sharp increase in exchange inventories likely to cap any significant recovery. Subdued industrial demand and cautious downstream buying are expected to keep market sentiment weak, although a stabilisation in inventories could provide some support.

Immediate support is likely around $1,780-1,800/t, while resistance is expected near $1,850-1,880/t. A sustained recovery above the $1,900/t mark appears unlikely in the near term unless inventory growth slows and downstream demand improves.

Inventory movements, Chinese demand, broader base metals sentiment and macroeconomic developments will remain key indicators for price direction. In India, buyers are expected to continue following a need-based procurement strategy amid adequate availability and cautious demand sentiment.

Leave a Reply