- Indonesian portside coal market stable; recovery expected

- Coking coal index edges up on steady trade activity

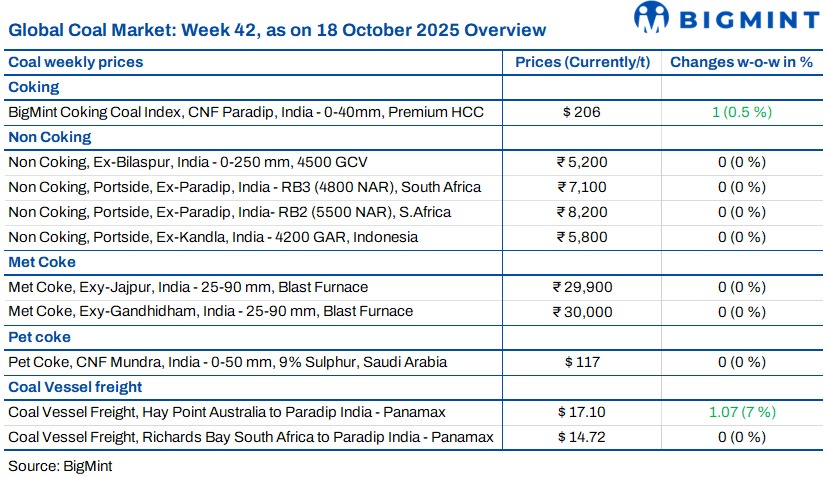

India’s coal market sentiment remained largely subdued this week as festive holidays and muted industrial activity slowed procurement. Traders adopted a wait-and-watch stance ahead of SECL auctions, while portside trading activity was slightly lower w-o-w on falling sponge prices. Freight rates showed mixed movement, reflecting soft demand from South Africa and Indonesia, though steady Australian inquiries offered some support. Market participants expect activity to pick up gradually post-Diwali as industrial operations normalise.

Indonesian coal prices steady amid festive lull

Indonesian thermal coal prices at Indian ports stayed largely unchanged this week as the festive lull and low industrial activity curbed buying. BigMint assessed 5000 GAR at INR 7,100/t (Kandla) and INR 7,050/t (Vizag), while 4200 GAR was steady at INR 5,800/t and INR 5,700/t, respectively. Only 3400 GAR eased INR 100/t to INR 4,400/t (Navlakhi) amid surplus stock. Port operations in Gujarat remained slow, though restocking may pick up post-Diwali. With Indonesian seaborne prices inching up, India’s portside market is likely to recover gradually by mid-November.

South African coal prices hold firm

South African portside coal offers in India stayed steady this week, with RB2 at INR 8,200/t and RB3 at INR 7,100/t across Paradip, Vizag, and Gangavaram. Some traders raised RB2 offers to INR 8,500/t after seaborne indices rose by $2-2.5/t, though no major deals occurred. Portside trades stayed limited, while inventories increased 9% w-o-w to 13.26 mnt on improved arrivals. Export offers inched up to $71.5/t FOB for RB2, with freight steady at $14.72/t. Sponge iron prices fell INR 750/t to INR 24,500/t amid weak steel demand. South African coal offers are likely to stay supported near term.

Domestic coal prices stable

Domestic coal prices stayed steady this week, with 5,000 GCV assessed at INR 6,250/t ex-Bilaspur and 4,500 GCV at INR 5,200/t. Market activity remained subdued as delays in order deliveries from earlier auctions limited fresh buying. Traders refrained from offering new quotes, awaiting clarity from SECL’s upcoming auctions on 24 and 25 October, which will offer 507,000 t and 356,000 t, respectively. Participants expect a clearer pricing trend to emerge once auction results and delivery schedules are confirmed, guiding near-term market direction.

BigMint coking coal index edges up

BigMint’s PHCC index rose $1/t w-o-w to $206/t CNF Paradip on 17 Oct’25, supported by consistent trade activity. Around 2-3 cargoes were booked, including a 30,000t Australian PHCC at $206-207/t CFR India and another 25,000t at $203/t. Stable domestic met coke prices and balanced Chinese supply further supported sentiment. BF-rebar prices in India dropped INR 200/t ahead of the festive period, reflecting muted steel demand. Overall, the market outlook remains steady with limited volatility expected in the near term.

Met coke prices steady

Domestic met coke prices held firm this week amid low buying activity ahead of festive holidays. BF-grade met coke stood at INR 29,900/t ex-Jajpur and INR 30,000/t ex-Gandhidham, while foundry-grade softened slightly to INR 35,500/t ex-Rajkot. Weak pig iron demand and slow industrial activity restricted restocking despite a fall in Australian PHCC prices by $2/t w-o-w to $188/t FOB. Imported Colombian met coke offers stayed steady at $265-275/t CFR India. In Durgapur, pig iron dropped INR 350/t to INR 31,500/t. Prices are expected to stay range-bound in the near term amid stable supply and muted demand.

Imported pet coke prices stable

Imported pet coke offers into India stayed stable this week as festive holidays kept trading quiet. Sellers maintained firm quotes, with US-origin material at $118-120/t CFR and Saudi-origin coke at $117-119/t CFR. Market activity remained normal, supported by steady demand and balanced freight rates. Participants expect prices to remain stable through December, with limited near-term movement as buyers await clearer consumption trends post-festive period.

Dry bulk coal freights show mixed picture

Dry bulk coal freight rates to India showed mixed movement this week, with the Pacific routes seeing some activity while the Atlantic remained quiet. The Indonesia-India Supramax route eased slightly to $16.19/dmt amid weak chartering and lower bunker costs, while South Africa-India Panamax freights stayed steady at $14.72/dmt on limited fixtures. In contrast, Australia-India Panamax rates rose to $17.10/dmt, supported by fresh spot buying from Indian steelmakers like SAIL and tighter vessel supply in the Pacific.

Leave a Reply