- Domestic steel prices dip on weak demand, cautious buying

- Pellet, coal, ferro chrome markets show mixed movements

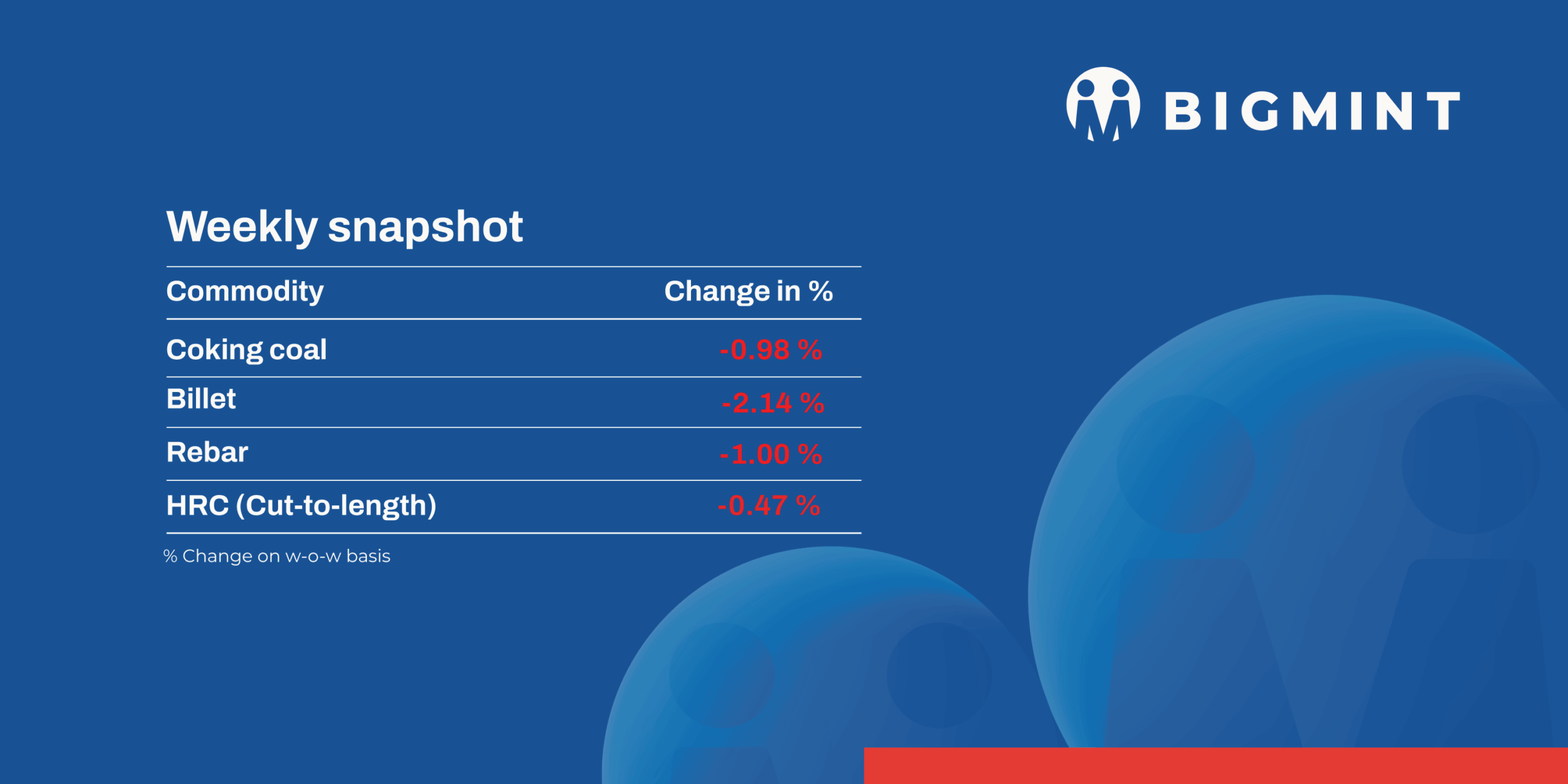

Domestic induction furnace finished long steel offers witnessed a downtrend in prices. Prices dropped INR 100-900/t. Trade-level prices of hot-rolled coils (HRCs) in India remained range-bound w-o-w.

Iron ore and pellet

- PELLEX, BigMint’s bi-weekly domestic pellet (Fe63%) index for Raipur, remained stable w-o-w at INR 10,350/t ($117/t) DAP on 29 August. Raipur-based producers kept their offers for Fe 63% (+/-0.5%) at INR 10,100-10,300/t ($115-117/t) exw. Deals of around 40,000 t pellets were concluded in Raipur this week.

- An Indian manufacturer recently concluded an export deal for 50,000 t of pellets (63%Fe, 1.5-2%Al2O3). The deal was heard concluded at $111-112/t FOB India, as per sources. Meanwhile, another 80,000-t export deal was heard from a western India-based supplier for Fe63.5%, 1.5% alumina material for loading in the last week of September.

- BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index remained largely stable w-o-w at $65.5/t FOB east coast on 28 August. Some suppliers said that buyers are offering 19% discounts for Fe 57% fines cargo, while Indian suppliers are quoting discounts closer to 16-17%. This discrepancy is causing negotiations to stall.

Coal

- South African RB2 and RB3 coal prices held steady at Gangavaram this week, though some eastern ports saw offers ease by INR 100-200/t on weak buying. Two RB2 deals were heard – 12,000 t at INR 8,000/t ex-Paradip and 7,000 t at INR 8,325/t ex-Krishnapatnam – but overall market activity stayed low amid uncertain offers and thin trader stocks.

- Domestic coal prices in India rose this week, supported by lower stock availability. BigMint assessed 5,000 GCV at INR 5,700/t ex-Bilaspur, up INR 450 w-o-w, while 4,500 GCV increased by INR 300/t to INR 4,800/t. Tight inventories pushed prices higher, while SECL auctions also drew stronger bids despite muted interest from sponge iron players.

- BigMint’s PHCC index rose by $6/t w-o-w to $206/t CNF Paradip on 29 August, even as trade remained thin. Australian offers eased by $5/t, with market chatter placing quotes at $215-218/t CFR India, while buyers view $200-205/t as workable. A miner reportedly sold 75,000 t GYC cargo at $189/t FOB Australia, though Indian participants pegged tradable levels closer to $185-186/t FOB.

- Met coke prices in India stayed stable w-o-w, with BF-grade assessed at INR 29,000/t ex-Jajpur and INR 30,000/t ex-Gandhidham, while foundry-grade held at INR 35,600/t ex-Rajkot. Supplies remained limited, and imports stayed muted as buyers resisted high-cost cargoes above $300/t CFR.

Ferrous scrap

- India’s imported scrap market stayed weak through the week as competitive domestic scrap kept buyers away from imports. Offers for HMS 80:20 for UK/EU stayed at $325-330/t CFR but demand was thin and bulk cargoes remained unworkable due to weak finished steel demand. Falling steel prices further dampened sentiment and reinforced buyer resistance to higher offers.

- Shredded offers stayed at $360-365/t CFR against bids of $358-362/t, while HMS 90:10 at $340-345/t met bids near $340/t, reflecting persistent buyer resistance.

Ferro alloys

- Silico manganese: Indian silico manganese prices (60-14) decreased by INR 830/t ($9/t) w-o-w to INR 69,700-69,900/t ($791-793/t) in the key regions of Durgapur, Raipur, and Vizag. Silico manganese prices in Raipur hit a three-month low due to weak global demand, limited export inquiries, and continued sluggish buying interest in overseas markets.

- Ferro manganese: Indian ferro manganese (HC 70%) prices dipped slightly by INR 140/t ($2/t) w-o-w to INR 70,500/t ($800/t) exw in Durgapur. However, prices, exw-Raipur, remained unchanged at INR 70,700/t ($802/t) w-o-w amid modest demand and increased availability from select producers in Durgapur.

- Ferro silicon: Indian ferro silicon prices dropped by INR 1,550/t ($18/t) w-o-w to INR 91,200/t ($1,035/t) exw-Guwahati. Meanwhile, Bhutan’s offers dipped by INR 1,000/t ($11/t) to INR 92,500/t ($1,049/t) exw. The market stayed quiet with few inquiries, while rising imports continued to exert downward pressure on overall sentiment.

- Ferro chrome: Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices rose by INR 6,000 ($68/t) w-o-w to INR 109,500/t ($1,242/t) exw-Jajpur. Prices reached their peak since November last year as material availability was limited which led to the rise in offers.

- Additionally, at OMC’s ferro chrome auction on 25 August, 3,050 t were sold from the 3,600 t offered. As per reliable sources, the 1,500 -t lot (Cr: 60-64%, Si: 4%, 10-100 mm) was booked in the price range of INR 108,700 – 108,800/t exw, up by INR 9,100- 9,200/t over the base price.

Semi-finished

- Indian semi-finished steel prices showed downward trend due to subdued demand that continued to pressure spot offering in the market as per BigMint’s assessment. Domestic billet prices in all key locations moved down by INR 100-900/t across regions. A major drop of INR 900/t was seen in Mandi Gobindgarh. Sponge iron prices witnessed bearish sentiments as need-based procurement was seen due to uncertainty in the market. In almost all key locations, prices moved down by INR 150-700/t.

- Indian DRI export offers increased by $1/t to $333/t CPT Raxaul, while CPT Benapole offers increased by INR 4/t to $342/t.

Finished long steel

- IF-rebar: India’s IF-route finished market is currently experiencing a slowdown due to weak sentiments and a lack of fresh customer inquiries, leading to sluggish order bookings. Manufacturers are being forced to lower their prices to liquidate inventories, which are seeing a 10-12 day idling period. This pressure is intensified by the volatility in raw material prices, monsoon rains and festivities that are causing buyers to procure cautiously. Market players feel prices have already hit the bottom and thus may rebound once the weather turns favourable specifically in the northern and western regions.

- On a weekly basis, rebar steel prices plunged in the range of INR 200-800/t across regions, as per BigMint’s assessment.

- The trade reference price of 10-25 mm Fe500 grade rebar manufactured via the IF route was assessed at INR 39,300-39,700/t exw Raipur, and at INR 43,000-43,600/t exw-Jalna.

- Trade reference prices of heavy structural steel with a base size of 150mm stood at INR 41,700-42,200/t exw-Raipur.

- Trade reference prices of wire rods hovered at INR 40,100-40,600/t ex-Raipur.

- BF-rebar: India’s trade-level blast furnace (BF) rebar prices dropped w-o-w across major markets. Some steel majors reduced their prices amid subdued domestic demand this week.

- Trade-level BF rebar prices decreased by INR 600/t ($7/t) w-o-w to INR 47,300/t ($538/t) exy-Mumbai, as per BigMint’s assessment on 29 August 2025. Prices are exclusive of GST at 18%.

- In the projects segment, prices dropped w-o-w to INR 46,000-47,000/t ($523-535/t) FOR Mumbai. Market activity was muted, as buyers stayed cautious during the monsoon season and the festive week. Construction momentum was further dampened by logistical challenges, leading to project delays and subdued procurement.

Flat steel

- Trade-level prices of hot-rolled coils (HRCs) in India remained range-bound w-o-w at INR 49,000-51,000/tonne (t) ($560-582/t). Similarly, cold-rolled coil (CRC) prices held steady w-o-w, ranging within INR 55,300-59,000/t ($631-673/t). The monsoon and key festive holidays impacted trade activity.

- BigMint’s benchmark assessment (bi-weekly) for HRCs (IS2062, Gr E250, 2.5-8 mm/CTL) fell by INR 300/t ($3/t) w-o-w to INR 49,700/t ($567/t) on 26 August 2025 against INR 50,000/t ($570/t) on 19 August 2025. However, CRC (IS513, Gr O, 0.9 mm/CTL) prices held stable w-o-w at INR 57,000/t ($650/t) on Tuesday. These prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

- India’s bulk imports of HRCs touched 290,767 t as of 23 August, based on vessel line-up data. Around 229,139 t of additional cargoes are expected by the second week of September.

- India’s bulk exports of HRCs touched 107,085 t as of 23 August, based on vessel line-up data with BigMint. Moreover, around 47,855 t of additional cargo are being shipped.

Leave a Reply