- Aluminium demand outlook in China remains supportive

- Market cautious ahead of US Fed rate revision

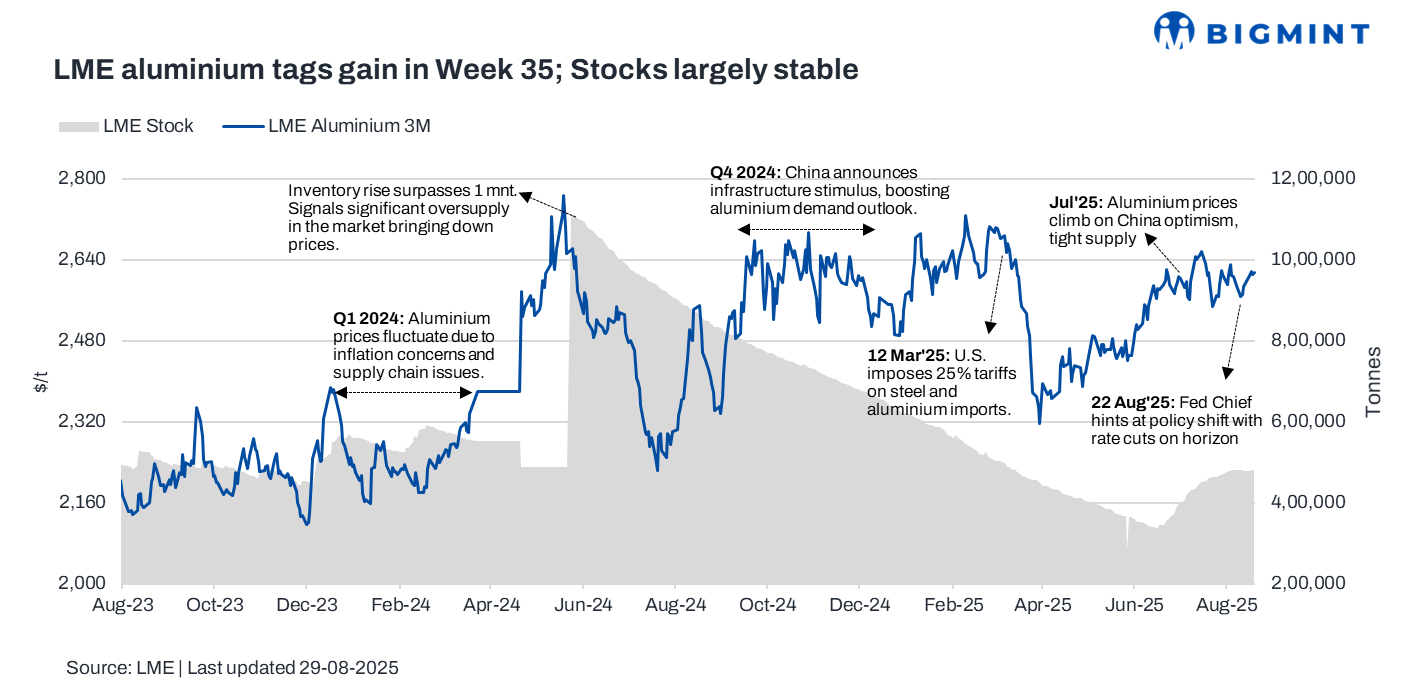

London Metal Exchange (LME) aluminium prices saw an overall saw a gain during Week 35 of CY’25 (25-29 August 2025).

Aluminium prices gained modestly, supported by signs of tightening supply and firm demand prospects. Lower inventories in key markets and an improving consumption outlook in China lent stability to prices despite ongoing global macroeconomic uncertainties.

Price performance, inventory trends

LME aluminium prices averaged about $2,613/t in Week 35, marking a 1.4% rise from Week 34 (18-22 August). The week began on a softer note at $2,609/t, but prices strengthened mid-week to $2,616-2,617/t and held steady towards the close at $2,616/t.

Meanwhile, aluminium stocks at registered warehouses saw minor inflows of 0.2%, to 480,381 t in Week 35 from 479,365 t in Week 34.

Global alumina output up 4% in Jul’25

Global metallurgical alumina production rose 4% to 12.13 million tonnes (mnt) in July 2025 from 11.72 mnt in June, supported by stronger refinery operations and fresh capacity additions in Asia, according to the International Aluminium Institute (IAI).

On a y-o-y basis, production was also up 4.14% from 11.65 mnt recorded in July 2024, underlining a steady expansion trend.

China remained a key driver of July’s alumina growth, with metallurgical-grade output rising 3% m-o-m as operating capacity and utilisation improved to around 81.6%. Northern plants expanded production notably, while southern refineries stabilised operations after routine maintenance, offsetting earlier disruptions.

Outlook

LME aluminium prices may remain rangebound next week as supply-side concerns and lower inventories lend support. The widening of US tariffs on aluminium products and ongoing sanctions on Russian supply could keep sentiment cautious, while steady Chinese demand and improved consumption prospects may underpin stability. However, global macroeconomic headwinds and signals from the US Federal Reserve on interest rates remain key factors that could cap sharp gains.

Leave a Reply