Domestic induction furnace-finished long steel prices showed slight improvement even as the steel market as a whole witnessed mixed trends.

Iron ore and pellet

- SteelMint’s bi-weekly domestic pellet (Fe 63%) index, PELLEX, remained stable w-o-w at INR 9,550/tonne (t) DAP Raipur on 16 February 2024. A deal of 15,000 t was recorded at INR 9,550/t DAP Raipur from the Raipur region in the last one week. Buyers were not interested in booking material currently as it was not feasible for them. Most buyers remained cautious and expected price reductions from the plant in the coming days.

- Odisha Mining Corporation (OMC) has scheduled an auction for 2.79 mnt of iron ore ( 1.546 mnt of fines and 1.243 mnt of lumps) on 19 February. OMC has reduced the base price m-o-m by INR 300-400/t and INR 50/t for the majority of fines and lumps lots, respectively. The fall in pellet and sponge iron prices has resulted in price cuts by the miner.

- Gujarat-based steel mills booked around 50,000 t of raw pellets (Fe65.5%) at INR 12,800/t ($154/t) DAP Kandla port this week from a central India’s pellet producer, sources informed BigMint. On the other hand, Jindal SAW pellet (Fe63%) offer was recorded at INR 12,200/t ($147/t) DAP Kandla today. The buyers booked 10,000 t of pellets at the same offers.

- Asia-Pacific Supramax dry bulk (50,000-55,000 t) freight rates for an iron ore vessel from the east coast of India to China was recorded at $14/tonne (t) on 14 February, down marginally by $1/t w-o-w, according to BigMint’s assessment. Dry bulk freight trade remained dull this week amid Chinese New Year holidays. However, the market is bullish as enquiries have been exhibiting a positive trend, which has kept rates supported.

Coal

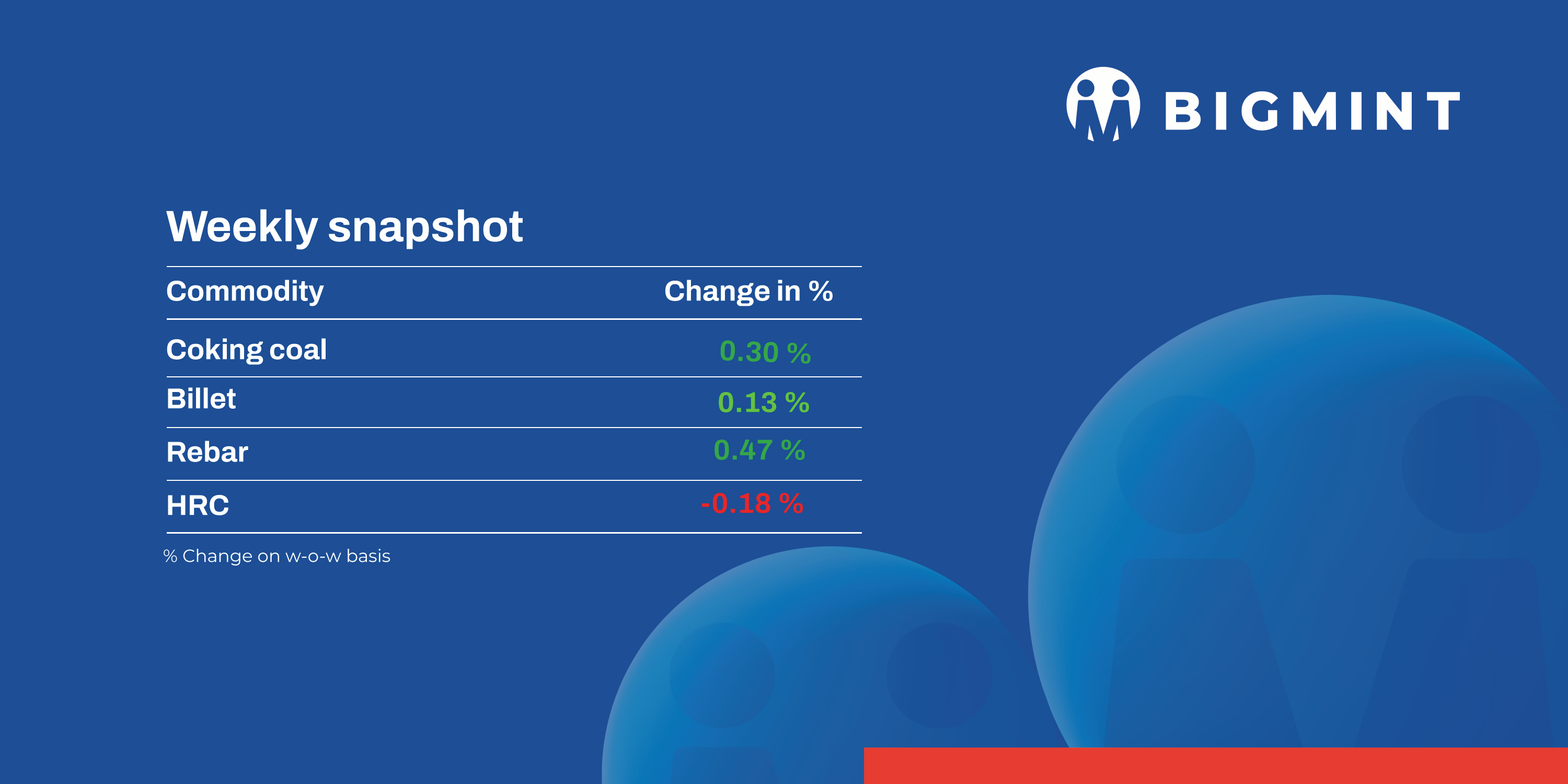

- Australian premium hard coking coal prices remained unchanged w-o-w to $315/t FOB and $331/ t CNF on 17 February amid tepid demand from India.

- RB1 (6000 NAR) grade prices remained stable w-o-w to $92/t FOB. Similarly, RB3 remained unchanged w-o-w at $63/t FOB Richards Bay, South Africa.

- Portside prices of South African RB3 (4800 NAR) thermal coal at Vizag Port recorded at INR 7,300/t, stable w-o-w.

Ferros Scrap

- This week, market activities in India remained lackluster as buyers leaned towards domestic scrap procurement and other available alternatives due to a significant gap between landed imports and domestic scrap prices. On a weekly average basis, import offers for shredded scrap from Europe edged up slightly by $1/t to $416/t CFR Nhava Sheva from $415/t CFR in the previous week, while HMS (80:20) offers dropped by $9/t on the week to $389/t CFR.

- A representative from a trading company remarked, “The current market suggests that shredded scrap should not exceed $400/t. However, indicative prices from the EU/UK are higher at $430-435/t, creating a $30/t gap that makes it economically unviable.”

- Another trader commented, “Imports have become economically impractical in India, leading buyers to favor local sources or alternatives like sponge. The few transactions happening involve arrival cargoes, with the maximum price for HMS capped at $385/t. Fresh bookings in the market are currently scarce due to these prevailing circumstances.”

- Throughout the week, approximately 1,000 t of shredded scraps were sold at $419/t CFR, followed by 500 t of HMS (80:20) at around $365-370/t CFR and around 250 t of Turning boring scraps at $345/t CFR.

Ferro Alloys

- Silico Manganese: Indian silico manganese prices continue to grow, owing to an increase in export inquiries and active bookings in the domestic and overseas market. Export prices for silico manganese (60-14) were $845/t FOB, up $7/t from Vizag/Haldia, while silico manganese (65-16) was valued at $945/t, up $10. On February 16, silico manganese (60-14) was trading at around INR 68,300-68,500/t ($823-$825/t) exw Durgapur, Raipur, and Vizag, up INR 550/t ($7/t).

- Ferro Manganese: Ferro manganese (HC70%) prices rose as export inquiries continue to move on an upward direction w-o-w. Ferro manganese prices in Durgapur and Raipur on 16 February varied between INR 68,300 and INR 68,500/t ($823-$825/t), up INR 525/t ($6/t).

- Ferro Silicon:Indian ferro silicon (FeSi:70%) prices remained largely stable with a minor drop by INR 50/t ($1/t) ex-Guwahati and Bhutan. Bhutan’s prices were sturdy as deals concluded at discounts resulted in slight decline in domestic prices. As of 16 February, BigMint reported ferro silicon prices in India at INR 106,900/t ($1,288/t), down INR 100/t ($1/t) exw-Guwahati and INR 106,850/t ($1,287/t) exw-Bhutan, down INR 150/t ($2/t).

- Ferro Chrome: On 16 February, Indian ferro chrome (HC 60%, Si:4%) prices stayed stable showing a slight decrease. Prices inched down by INR 700/t ($8/t), reaching INR 117,800/t ($1,419/t) exw-Jajpur. Vedanta-FACOR’s ferro chrome auction was closed at INR 117,900 ($1420/t), market awaits OMC’s chrome ore auction on 19 February for further clarity on prices. Prices for 304 grade stainless steel increased INR 3,000/t ($36/t) w-o-w to INR 176,000/t ($2,120/t) exw-Mumbai. The primary cause of it was the rise in raw material and futures prices.

Semi-Finished

- Indian semi-finished steel prices increased, as per BiglMint’s assessment. Domestic billet prices increased by INR 50-500/t in all key regions, with a major increase of INR 500/t seen in Mandi Gobindgarh market. However, billet prices in Mumbai, Ramgarh and Durgapur showed a slight drop of INR 100-300/t. Similarly, sponge iron prices in some key locations also increased by INR 50-300/t, with a major increase of INR 300/t seen in Raigarh and Mandi Gobindgarh market. However, sponge iron prices in Ramgarh and Durgapur fell by INR 50-700/t respectively.

- SAIL-Rourkela Steel Plant held an auction for 3,800 t of steel grade pig iron on 16 February. Out of total quantity, 1,000 t was booked at an average price of INR 36,700/t exw.

- SAIL’s Durgapur Steel Plant held an auction for 2,100 t of steel grade pig iron. The total quantity was booked at an average price of INR 37,850/t exw.

- NMDC’s steel plant in Nagarnar, Chhattisgarh, conducted a steel-grade pig iron auction for a total of 30,000 t on 13 February. The whole quantity was booked at an average price of INR 34,900/t.

- Indian DRI (Direct Reduced Iron) exports offers decreased by approximately $2-3/t, reaching $353/t on CPT Raxaul, and $360/t on CPT Benapole.

Finished-long steel

- India’s finished long steel market of induction furnace route observed an improvement in trading activities this week, which varied across regions. Buyers opted for a wait and watch policy to place orders and closely monitored market movements. From the middle of the week, manufacturers gradually started receiving moderate booking orders in rebar, structural and wire rod steel along with smooth lifting of previously booked material. Considering the current prices and low margins in finished steel made buyers confident as they gained clarity about market direction and procured the material. Along with the previously mentioned factors as well as the rising prices of raw material (Sponge iron and Billet) also supported which led to improvement in trading activities in spot market. However, in few locations mills are still lacking somewhere to receive healthy bookings, BigMint learned.

- On a weekly basis, in rebar steel prices fluctuates in the range of INR 100-600/t across the regions except few markets stable as witnessed as per BigMint assessment shows.

- The trade reference price of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size was assessed at INR 42,500-42,900/t exw Raipur, INR 48,000-48,500/t exw Jalna.

- Trade reference price of heavy structural steel for base size 150mm channel stands at INR 45,000-45,400/t exw Raipur.

- Trade reference prices of wire rod hovering at INR 42,800-43,200/t ex Raipur.

BF-rebar

- Trade-level prices of blast furnace (BF) rebars dropped w-o-w amid slow buying interest. Meanwhile, prices were range-bound during the week and buyers procured on urgent need basis only. Inventories in the distribution network have increased and participants have been destocking considering the subdued domestic demand and market uncertainty.

- Current week’s rebar prices (12-32mm, Fe500D) in the trade segment dropped by INR 300/t w-o-w to INR 51,800/t exy-Mumbai. Prices are exclusive of GST at 18%.

- In the projects segment, prices are hovering around INR 50,000-50,500/t FOR Mumbai basis, unchanged against last week’s price levels. Demand remained need basis only due to subdued market sentiments.

Finished flate steel

- Trade level hot-rolled coil (HRC) and cold-rolled coil (CRC) prices have remained range-bound in key markets of Mumbai, Faridabad and Chennai. However in the other markets under assessment there have been mixed trends. HRC prices edged down in other markets under assessment weighed down by the subdued market activity driven by need-based buying, liquidity concerns, and imports pressure.

On the other hand, CRCs showed an increase in some regions as distributors started quoting higher because of the constrained supplies, although the demand remains lacklustre, informed sources. - BigMint’s bi-weekly benchmark assessment for HRC (IS2062, Gr- E250, 2.5-8mm) at INR 54,000/t and CRC (IS513, Gr-O, 0.9mm) at INR 61,600/t. The prices mentioned are on an exy-Mumbai basis for cut-to-length form, and excludes GST at 18%.

- BigMint’s India HRC (SAE 1006) export index for the Middle East and Vietnam dipped to $587/t FOB, down from $599/t FOB east coast India, reflecting weakened global market sentiment.

Meanwhile, Indian HRC export offers to the European Union decreased by $10/t w-o-w to $705-710/t CFR Antwerp, impacted by sluggish domestic demand and buyer hesitancy amidst market uncertainty. - Notably, India’s bulk HRC and plates imports increased, reaching 2,19,655t till 10 February 2024, marking a significant rise from the previous month. Total import volumes for January 2024 reached 6,60,344 tonnes, surpassing December 2023 figures.