- BF-route rebar prices witness further decline

- Lesser HRC imports so far in Feb, but demand dull

- Stable raw materials keep finished prices in check

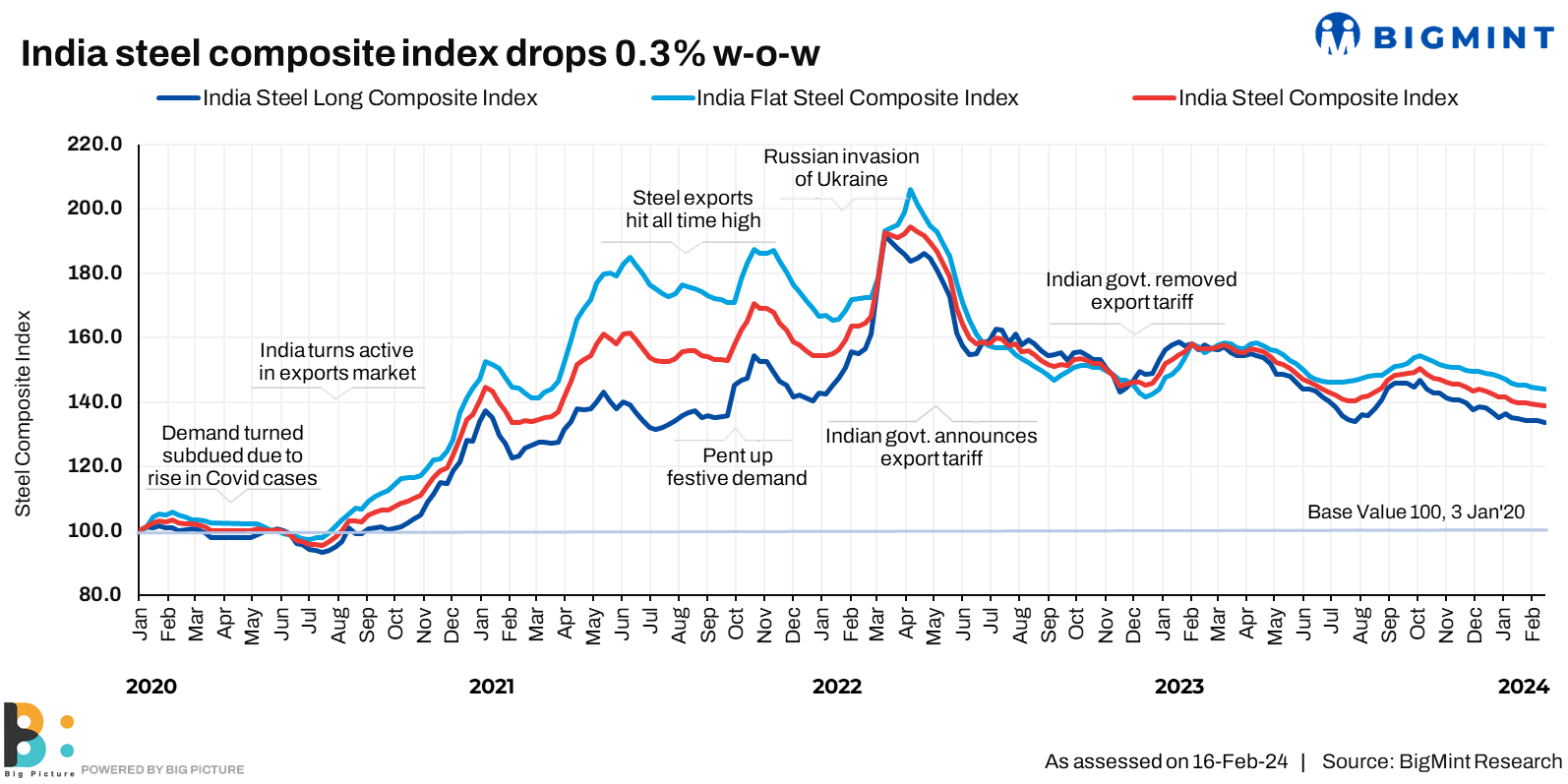

Morning Brief: The India Steel Composite Index fell to an almost two-year low for the week ended 16 February, 2024, although on a w-o-w basis, it remained flat at 138.80 points compared to 139.20 in the preceding week. Levels comparable to last Friday’s closing were seen on 26 March, 2021 (136.8).

Factors pushing the index downward

Overall, it was a highly range-bound week in all aspects (raw materials to finished) which aggravated the sluggishness in the market.

BF-route rebar falls further on tepid demand: Trade-level blast furnace-route rebars slid down further by INR 300/tonne (t) ($4/t) to INR 51,800/t ($624/t) ex-Mumbai, minus 18% GST. Project segment prices remained static at INR 50,000-50,500/t ($602-608/t).

Procurement was entirely need-based as demand was highly tepid. Consequently, inventories have piled up. It may be recalled, rebar inventories were already up 8% m-o-m in January.

IF-route prices inert w-o-w: The slide in the BF segment was partly a knee-jerk reaction to the dullness prevailing in the induction furnace (IF) rebar space which commands 65-70% of the market. Prices here remained flat w-o-w at INR 48,100/t ($579/t). Here too, lacklustre buying amid rising inventories did not allow mills any space to raise offers.

With the BF-route prices sliding further, the average spread with induction furnace (IF) material has normalized to INR 3,500-4,000/t (42-48/t). However, the worrisome aspect here is that the spread normalization has happened at lower price points.

Dullness prevails in flats segment: In flats, sentiments similar to rebar prevailed – buyers continued to make need-based procurements.Thus, trade-level hot rolled coil (HRC) prices remained stable w-o-w at INR 53,500-54,500/t ($646-657/t) while cold rolled prices were also static at INR 61,500-62,500/t ($741/-753/t). Factors like lacklustre domestic demand, imports, inventory glut and range-bound raw material prices have been converging for months now, to keep prices under check. However, import volumes, so far into February, have dropped somewhat to 0.20 million tonnes (mnt) from January’s 0.66 mnt levels as fresh bookings have been easing amid the prevailing market dullness.

Exports dull amid Lunar holidays: Export offers also inched down in a market characterized by the Lunar New Year and Tet induced lull in China and Vietnam. BigMint’s HRC export index inched down $12/t w-o-w. Overall, global sentiments were also subdued as offers to the European Union also dropped $10/t as buyers are well-stocked in an already sluggish overseas market.

Raw material prices flat w-o-w: There was little scope to raise rebar prices because key raw materials also remained range-bound. BigMint’s iron ore index for Fe62% fines remained flat w-o-w at INR 5,800/t ($70/t), although coking coal inched up slightly to $331/t CNF Paradip over last week.

For the IF mills especially, sponge iron, (PDRI, ex-Raipur), remained flat w-o-w at INR 26,300/t ($317/t). BigMint’s billet index, exw-Raipur, was also inert w-o-w at INR 39,200/t ($472/t) w-o-w.

Outlook

Market fundamentals are expected to remain the same in the short term. Factors like liquidity crunch, dull domestic demand, and geo-political uncertainties will continue to impact the steel market. In India, the run-up to the general elections this year may also see a slowdown in demand.

India Steel Composite Index

The India Steel Composite Index is assessed on a weekly basis, every Friday at 18:30 IST, as per the weighted average prices based on manufacturing capacity and production.

BigMint considers the Composite Index with the base year being 3 January 2020 (financial year 2019-2020) and the base value as 100. The Composite Index does not give the absolute price but a trend of the market. The Indian steel industry is broadly classified into the BF-BOF and the electric/induction furnace routes. Keeping this broad classification in view, BigMint proposes to release the Composite Index by considering both production routes by manufacturing capacity and the production weighted method to compute the index for India.