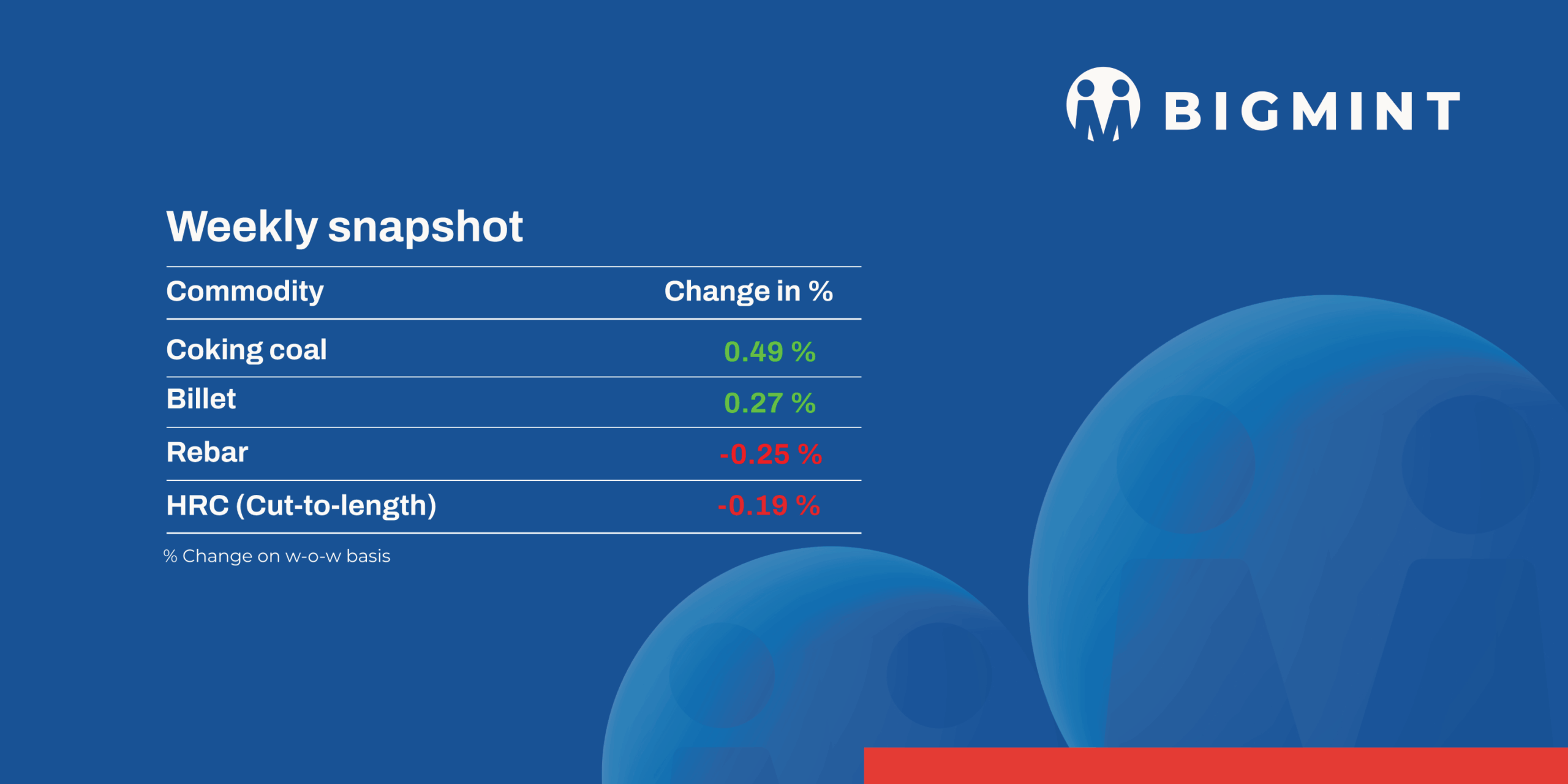

The domestic steel market saw seesaw price trends during week 38 ( 15-19 September, 2025). Semi-finished steel prices varied in the range of INR 50-500/tonne (t).

Iron ore and pellet

- In OMC’s iron ore fines auction of 1.92 mnt (Fe 51-65%) on 19 September 2025, around 1.674 mnt (87%) of fines were booked at INR 2,550-5,450/t. Bids (weighted average) declined by INR 350/t m-o-m; however, against base prices bids rose by INR 50-750/t . The drop in prices was due to weak steel market sentiment and lack of clarity regarding export duty imposition and lowering of iron ore prices.

NMDC Chhattisgarh auctioned 70,200-t iron ore from Bacheli on 18 September. The entire 17,200-t DR CLO (Fe 67%) fetched 13% premium (base INR 6,910/t), while 4,000-t sized lumps (10-20 mm, Fe 65.5%) securing 20% premium (base INR 6,300/t). Meanwhile, 8,000-t fines (Fe 64%) were sold at the base price of INR 5,290/t, and 6,000-t ROM remained unsold (base INR 6,050/t). Prices were on FOR basis, inclusive of royalty, DMF, and NMEDT. - An eastern Indian manufacturer concluded an export deal for 75,000 t of pellets (Fe 62+%, 3% Al2O3). The deal was heard concluded at $118-120/t CFR China, as per sources. Few more deals were heard from central India and west India suppliers concluded in the sea market at $125-130/t CFR China.

- BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export remained stable w-o-w at $67.5/tonne (t) FOB east coast on 18 September. BigMint recorded export deals for nearly 325,000 t (fines + lumps) during the recent trading sessions. Cargoes of Fe 57% fines were finalised in the range of $78-80/t CFR China. Alongside fines, a few lump cargoes floated by miners also found successful bookings, reflecting steady buying interest.

Coal

- The Indian met coke market stayed unchanged this week, with BF-grade assessed at INR 29,500/t ex-Jajpur and INR 30,000/t ex-Gandhidham, while foundry-grade held INR 35,600/t ex-Rajkot. Trading stayed limited around 20,000 t, as buyers preferred local supply. Imports were weighed down by muted buying, though Chinese restocking ahead of holidays lent regional cost support.

- South African coal prices at Vizag and Gangavaram remained mostly unchanged this week, with RB2 steady at INR 7,750–7,900/t and RB3 around INR 6,800/t. Activity stayed muted as both buyers and sellers waited for clarity post-22 Sep cess removal. No major trades surfaced, though some forward RB2 offers were heard near INR 8,200–8,400/t. Export offers held stable at $71/t for RB2 and $60/t for RB3, reflecting weak Indian demand.

- Domestic coal prices stayed flat this week, with 5,000 GCV at INR 5,750/t ex-Bilaspur and 4,500 GCV at INR 4,900/t. Buyers continued to adopt a cautious stance ahead of 22 September, when cess removal is expected to ease FSA-linked prices. For now, offers remain unchanged, with market direction likely to emerge only after GST adjustments take effect.

Ferrous Scrap

- India’s imported scrap market remained largely quiet through the week, with shredded holding at $360-365/t CFR Nhava Sheva, though workable levels were closer to $360/t, while busheling at $375-378/t met bids closer to $365-366/t and HMS at $330-335/t CFR. Currency volatility and weak buying appetite kept activity muted.

- Mills showed little interest in higher shredded offers, along with cheaper domestic substitutes, kept mills reluctant to accept higher prices. Participants felt prices were already near the bottom, making sharp corrections unlikely, while a $5-10/t bid-offer mismatch further restricted trades.

Ferro alloys

- Silico manganese: Indian silico manganese prices (60-14) dipped by INR 200/t ($2/t) w-o-w to INR 69,000-69,200/t ($783-786/t) in the key regions of Durgapur, Raipur, and Vizag. Prices dropped as buyers resisted elevated offers amid stable demand and sufficient market availability. Meanwhile, export prices of the 65-16 grade edged down by $2/t w-o-w to $910/t FOB Vizag/Haldia, India.

- Ferro manganese: Indian ferro manganese (HC 70%) prices remained largely stable, rising by INR 100/t ($1/t) w-o-w to INR 70,400/t ($799/t) exw in Durgapur. Meanwhile, prices, exw-Raipur, also edged up by INR 100/t($1/t) to INR 70,500/t ($800/t) w-o-w. Stable demand and limited supply fluctuations kept ferro manganese prices largely unchanged with minor adjustments.

- Ferro silicon: Indian ferro silicon prices were largely steady, dipping slightly by INR 200/t ($2/t) w-o-w to INR 88,700/t ($1,007/t) exw-Guwahati. However, Bhutanese offers went up by INR 900/t ($10/t) to INR 88,400 ($1,004/t). Prices rose on tight supply, with limited sellers and Bhutanese exports driven by strong overseas demand.

- Ferro chrome: Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices dipped by INR 300/t ($3/t) w-o-w to INR 117,800/t ($1,337/t) exw-Jajpur. Prices fell as previously elevated offers failed to hold amid subdued buying interest.

- Additionally, at OMC’s chrome ore auction on 19 September, nearly all material (79,600 t) was sold, with bids rising 6–45% (INR 550–8,809/t) m-o-m. Moreover, ferro chrome auction is scheduled for September.

Semi Finished

- Indian semi-finished steel prices showed fluctuating trends. Domestic billet prices in all key locations showed mixed movement as small price corrections encouraged a few spot purchases, but overall demand remained nominal because of moderate activity and cautious buying. Prices in some locations increased by INR 50-500/t ($1-$6) but in other regions fell in the range of INR 50-500/t ($1-$6). Driven by moderate bookings in the semi-finished steel segment and supported by gradually recovering finished steel demand, sponge iron prices in all regions moved up by INR 100-700/t ($1-$8). However, prices fell in Hyderabad and Bellary by INR 200-300/t ($2-$3).

- Indian DRI (Direct Reduced Iron) export offers decreased marginally by $1 stood at CPT Raxaul, at $329/t while, CPT Benapole offers seen decreased by $1/t and stands at $337/t.

- NMDC’s Nagarnar steel plant held a steel-grade pig iron auction for 32,000 t on 16 September. The entire quantity (8 lots) were booked at an average price of INR 30,350/t (by rake), pending management approval. Bids fell by INR 450/t from the previous approved auction, on 13 August for 32,000 t, in which the entire quantity was booked at an average price of INR 30,800/t (by rake).

- NMDC’s steel plant in Nagarnar, Chhattisgarh, auctioned 10,000 t of steel-grade pig iron on 18 September, with the entire quantity booked at an average price of INR 31,700/t (by road). However, management approval is still pending. Bids fell by INR 300/t from the previous auction on 22 August for 10,000 t, in which the entire quantity was booked at an average of INR 32,000/t (by road).

Long Steel

- IF-rebar: India’s induction furnace (IF) route rebar prices showed mixed trends w-o-w, with buying activity largely confined to immediate requirements—varying by region. In the latter half of the week, manufacturers raised prices and secured moderate bookings. Sellers continued to adjust trade discounts based on prior bookings and payment terms. Given the current market conditions, prices are expected to remain rangebound in the near term.

- On a weekly basis, in rebar steel prices witnessed variation in the range of INR 100-600/t across the regions, as per BigMint assessment.

- The trade reference price of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size was assessed at INR 39,400-39,800/t exw Raipur, INR 43,700-44,300/t exw Jalna.

- Trade reference price of heavy structural steel for base size 150mm channel stands at INR 42,000-42,500/t exw Raipur.

- Trade reference prices of wire rod hovering at INR 40,400-40,900/t ex Raipur.

- BF-rebar: India’s trade-level blast furnace (BF) rebar prices declined w-o-w, weighed down by subdued domestic demand and sluggish market activity due to monsoon rains in several regions. Liquidity constraints in the market also impacted trade activity.

- Trade-level BF rebar prices edged down by INR 200/tonne (t) ($2/t) w-o-w to INR 47,000/t ($533/t) exy-Mumbai, as per BigMint’s assessment on 19 September. Prices are exclusive of GST at 18%.

- In the projects segment, prices hovered between INR 45,500-46,500/t ($516-528/t) FOR Mumbai.

Flat Steel

- Trade-level prices of hot-rolled coils (HRCs) in India fell w-o-w to INR 48,100-50,300/t ($546-571/t). Moreover, cold-rolled coil (CRC) prices showed a downtrend w-o-w, with prices ranging between INR 54,800-59,000/t ($622-670/t).

- BigMint’s benchmark assessment (bi-weekly) for HRCs (IS2062, Gr E250, 2.5-8 mm/CTL) decreased by INR 300/t ($3/t) w-o-w to INR 49,200/t ($559/t) on 16 September against INR 49,500/t ($562/t) on 9 September. Similarly, CRC (IS513, Gr O, 0.9 mm/CTL) prices declined by INR 400/t ($5/t) w-o-w to INR 56,100/t ($637/t) on Tuesday against INR 56,500/t ($642/t) a week ago. These prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST. Indian HRC market sentiment stayed muted as sluggish demand, oversupply and ample inventories pressured prices.

- India’s bulk imports of HRCs touched 209,072 t as of 13 September, based on vessel line-up data. Around 166,872 t of additional cargoes are expected by the end-August.

- India’s bulk exports of HRCs touched 100,523 t as of 13 September and around 19,513 t of additional cargo are being shipped.

Leave a Reply