- Downside pressure persisted across most LME metals despite isolated gains

- Domestic markets saw limited activity with buying largely need-based

LME base metals showed a mixed trend on a w-o-w basis as of the latest update, with gains concentrated in nickel, while the rest of the complex largely declined. Nickel was the sole gainer, rising 3.11% to $19,385/t, reflecting relatively stronger market sentiment. In contrast, aluminium fell 2.14% to $3,523/t, copper declined 3.01% to $12,895/t, and zinc dropped 3.77% to $3,343/t, marking the steepest fall among the base metals. Lead remained broadly stable, inching up 0.10% to $1,956/t.

On the inventory front, trends were also mixed. Copper stocks increased by 1.55% to 398,675 t, indicating some easing in supply tightness. Meanwhile, inventories declined across other metals, suggesting continued offtake. Zinc stocks recorded the sharpest drop, down 6.39% to 96,250 t, followed by aluminium, which fell 3.07% to 364,725 t. Lead inventories slipped 0.56% to 268,500 t, while nickel stocks edged lower by 0.42% to 276,396 t, pointing to relatively balanced near-term availability.

Aluminium

India’s imported aluminium scrap market displayed a mixed-to-soft trend w-o-w as of the latest assessment, amid cautious buying interest despite continued support from relatively firm global benchmarks and LME-linked cues.

As per the latest assessment, UK-origin Zorba 95-5 scrap, CFR Nhava Sheva, declined to $2,875/t from $2,940/t, marking a drop of $65/t w-o-w, indicating some easing after earlier firmness. Meanwhile, US-origin tense scrap (attachments 6-7%), CFR Nhava Sheva, fell to $2,730/t from $2,745/t, registering a decline of $15/t w-o-w, reflecting mild pressure from buyer resistance and slightly improved availability.

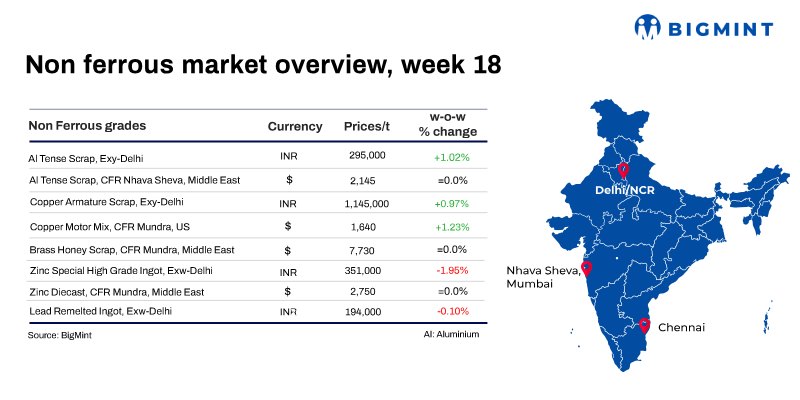

On the domestic front, sentiment remained stable to slightly soft. P1020 aluminium ingot, ex-Delhi NCR, was assessed at INR 370,500/t, down by INR 7,000/t w-o-w from INR 377,500/t tracking the weakness in LME and MCX trends. However, tight inventory levels limited the downside, keeping spot prices relatively supported despite subdued buying activity.

Overall, the imported aluminium scrap market remained range-bound with a mild corrective bias, while the domestic ingot segment held broadly steady, supported by firm global cues and constrained supply conditions.

Copper

India’s copper scrap market displayed a rangebound trend w-o-w as of the latest assessment, amid weak buying interest and persistent margin pressure despite relatively stable LME copper prices. Demand from the key consuming hub of Jamnagar remained largely need-based, with brass processors continuing to operate cautiously due to tight margins and subdued finished goods demand, limiting fresh procurement activity.

The market remained supported by tight domestic scrap availability and controlled inflows; however, weak downstream consumption and thin spot liquidity capped any upward movement. Buyers largely preferred immediate requirement-based purchases, while resistance at higher price levels and ongoing margin pressure restricted aggressive restocking, with minimal interest in bulk bookings.

As per the latest assessment, brass honey scrap, exw-Jamnagar, was assessed at INR 760,000/t, broadly unchanged w-o-w, reflecting muted trade flows and cautious procurement behaviour during the period.

Overall, weak domestic demand and sustained margin pressure remained the key market drivers, while stable global copper cues offered limited support, keeping sentiment cautious with prices moving within a narrow range.

Zinc

India’s zinc ingot (Zn 99.995%) prices inched up w-o-w as of the latest assessment, supported by a recent producer price hike, although muted downstream demand continued to weigh on sentiment. SHG zinc ingot (ex-Delhi) was assessed at INR 353,000/t, up by INR 3,000/t w-o-w from INR 350,000/t, reflecting limited but steady procurement activity from galvanizing units, with buying largely restricted to immediate requirements.

The domestic uptick came despite softer LME zinc trends, where prices declined 3.77% w-o-w to $3,343/t, indicating weak global momentum. On the domestic front, Hindustan Zinc Limited (HZL) initially supported prices through hikes but later cut zinc ingot prices by INR 7,200/t to INR 359,100/t, highlighting volatile producer pricing amid subdued demand conditions.

In the secondary segment, prices showed marginal improvement. Zinc oxide (99% Zn, ex-Delhi) increased by INR 700/t w-o-w to INR 275,700/t, supported by steady demand from downstream sectors such as rubber and chemicals. Meanwhile, zinc dross prices remained largely stable, reflecting weak buying interest and margin pressure.

Overall, producer-led price support helped primary zinc prices edge higher, but subdued demand, HZL’s subsequent price cut, and softer LME trends capped further gains, keeping the market rangebound with limited upside.

Lead

India’s domestic lead market remained largely stable with a marginal upward bias w-o-w as of the latest assessment. Lead primary ingot (ex-Delhi) was assessed at INR 203,000/t, up by INR 1,200/t w-o-w from INR 201,800/t, while lead remelted ingot (ex-Delhi) was assessed at INR 194,000/t, broadly stable w-o-w with a marginal dip of INR 200/t from INR 194,200/t, reflecting steady-to-cautious spot demand conditions.

The marginal firmness in primary prices came despite mixed producer signals. Hindustan Zinc Limited (HZL), in its latest revision, increased lead ingot prices by INR 400/t to INR 219,200/t (ex-works), indicating limited but continued producer support, even as broader base metal sentiment remained mixed.

On the global front, LME lead prices edged up marginally by 0.10% w-o-w to $1,956/t, while stocks declined by 0.56%, suggesting tightening exchange inventories and offering mild support to prices.

Overall sentiment remained stable, with modest gains in primary lead offset by largely flat secondary prices, as balanced demand-supply dynamics and cautious buying activity continued to limit any sharp directional movement.

Leave a Reply