- Global aluminium output up 1.1% y-o-y

- Refined copper production rises 4.4% y-o-y

London Metal Exchange (LME) base metal prices mostly traded higher on a week-on-week basis in the week ended 27 December. Aluminium prices inched up by 0.53% w-o-w to $2,961/t, while LME stocks rose slightly by 0.28% to 521,050 t. Nickel recorded the strongest price gain, climbing 6.64% w-o-w to $15,786/t, alongside a modest 0.45% increase in inventories to 255,696 t.

Copper prices advanced 2.37% w-o-w to $12,163/t, supported by a 2.10% decline in LME stocks to 157,025 t, indicating tighter supply conditions. Zinc prices rose 0.59% w-o-w to $3,091/t; however, inventories increased sharply by 6.98% to 106,875 t, reflecting stock build-up. Lead prices also gained 0.50% w-o-w to $1,995/t, while LME stocks declined by 3.76% to 248,900 t.

Meanwhile, LME copper prices crossed the $12,000/t mark on Tuesday, touching a fresh record in the final trading days of 2025. The three-month LME copper contract rose 1% to trade at $12,055/t, compared with $11,925/t in the previous session. Prices are now up around 36% so far this year, extending a strong upward trend.

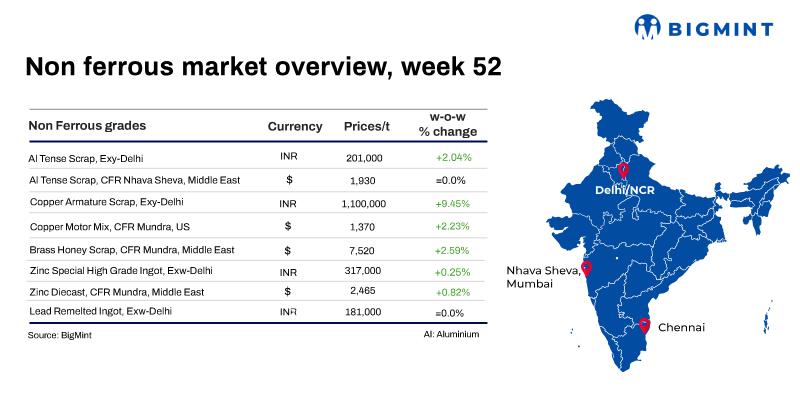

India’s imported aluminium scrap prices recorded slightly positive trends in the week ended 27 December, following positive momentum in LME prices, with mixed movements observed across key grades.

BigMint assessed Middle East-origin Tense (8-9%) at $1,930/t, unchanged w-o-w and US-origin Tense (6-7%) at $2,025/t, up by $25/t w-o-w. UK-origin Zorba 95/5 inched up $30/t to $2,320/t, and UK-origin Wheel prices gained $20/t to $2,675/t.

India’s domestic aluminium prices recorded notable week-on-week gains, supported by upward price revisions from primary producers following a rise in LME and MCX aluminium prices and renewed global supply concerns. BigMint’s assessment showed India’s domestic P1020 ingot (99.7%) prices rising by INR 5,000/t w-o-w to INR 292,000/t ex-Delhi NCR.

Additionally, NALCO raised its primary aluminium ingot (P1020, 99.7%) prices by INR 5,600/t ($62/t) on 24 Dec’25.

Imported copper scrap prices in India moved higher w-o-w on 27 December, supported by a strong rise in benchmark copper prices on the London Metal Exchange (LME) futures.

Domestic copper scrap prices firmed in line with the strong LME uptrend, but restocking appetite stayed muted, with buyers limiting purchases to immediate requirements during the year-end holiday period.

According to BigMint’s assessment, Birch/Cliff was assessed at $11,260/tonne (t), up by $470/t w-o-w, while US motors mix stood at $1,370/t, up by $30/t w-o-w (both CFR Mundra).

India’s domestic brass honey prices remain rangebound w-o-w with 1% upside on subdued market activity and multiple demand-side pressures. According to BigMint’s assessment, brass honey exw Jamnagar was assessed at INR 620,000/t, 1% up w-o-w.

Zinc

The Indian zinc scrap market recorded mixed trends during the week ending 27 December. Tight spot supply led to a slight uptick in prices of imported diecast scrap, though gains in other grades were limited by softer global zinc prices and subdued domestic demand.

BigMint assessed zinc diecast scrap (Middle East origin) at $2,450/t CFR west coast India, up $30/t w-o-w, supported by limited spot availability despite a correction in London Metal Exchange (LME) futures.

Domestic zinc spot prices stood at INR 317,000/t exw-Delhi, up by 0.63% w-o-w. HZL zinc prices were down by 1.24% w-o-w at INR 310,600/t ex-Chanderiya.

Lead

Domestic primary lead ingot prices stood at INR 191,000/t, down by 0.26% w-o-w, while re-melted ingots stood at INR 181,000/t, unchnaged w-o-w.

Meanwhile, HZL lead prices stood at INR 207,900/t ex-Chanderiya, up by 0.34% w-o-w.

Other updates

Global aluminium scrap trade rises 3% in Jan-Oct’25

Global aluminium scrap trade volumes, including intra-European trade, increased by 3% y-o-y in the first ten months of 2025 (10MCY’25). India remained the key demand driver, increasing its imports by 15% to 1.65 mnt, especially from the EU, UK, and Middle East.Total exports in 10MCY’25 stood at 9.95 million tonnes (mnt) compared to almost 9.68 mnt in 10MCY’24, as per provisional data available with BigMint. Notably, the global aluminium scrap trade volume stood at 11.69 mnt in 2024 and is expected to increase to nearly 11.9 mnt in 2025.

Global aluminium output rises y-o-y in Jan-Nov’25

Global primary aluminium production reached 67.49 million tonnes (mnt) in 11MCY’25, registering a 1.1% y-o-y increase from 66.74 mnt in 11MCY’24. The modest growth underscores broadly stable output levels across key producing regions, with consistent smelter operations offsetting intermittent demand fluctuations and regional supply adjustments.However, global primary aluminium production in November 2025 fell 3.3% m-o-m to 6.09 mnt from 6.29 mnt in October.

Global refined copper production up over 4% y-o-y in Jan-Oct’25: ICSG

The International Copper Study Group (ICSG) has reported preliminary data for January-October 2025, showing that global refined copper production grew by around 4.4% y-o-y, supported by a 4% rise in primary production (from ores via electrolytic and electrowinning processes) and a 5.6% increase in secondary production (from scrap). Growth in global refined copper production during the period under review continued to be underpinned by China and the Democratic Republic of Congo (DRC). Together, these two producers accounting for around 57% of global output, are estimated to have recorded a combined production increase of about 9% (China +9.3%, DRC +7.8%). Excluding China and the DRC, global refined copper output declined by approximately 1.6%.

Leave a Reply