- Japanese aluminium premium jumps on supply tightness

- Kipushi zinc mine meets CY’25 targets, CY’26 outlook raised

London Metal Exchange (LME) base metals prices showed mixed trends on a w-o-w basis as of 17 January 2026, with selective gains across the complex amid divergent inventory trends. Aluminium prices inched up 0.10% w-o-w to $3,139/t, while LME stocks declined 1.97% to 488,000 t, indicating slightly tighter availability. Nickel prices rose 0.69% w-o-w to $17,825/t, even as inventories edged up 0.33% to 285,732 t.

Copper prices eased 0.52% w-o-w to $12,930/t, pressured by a 3.43% increase in LME stocks to 143,735 t, suggesting easing supply tightness. Zinc outperformed, gaining 2.81% w-o-w to $3,242/t, supported by a 0.86% drawdown in inventories to 106,525 t. Lead prices also firmed, rising 0.61% w-o-w to $2,062/t, while LME stocks fell sharply by 7.35% to 206,350 t, reflecting an improving market balance.

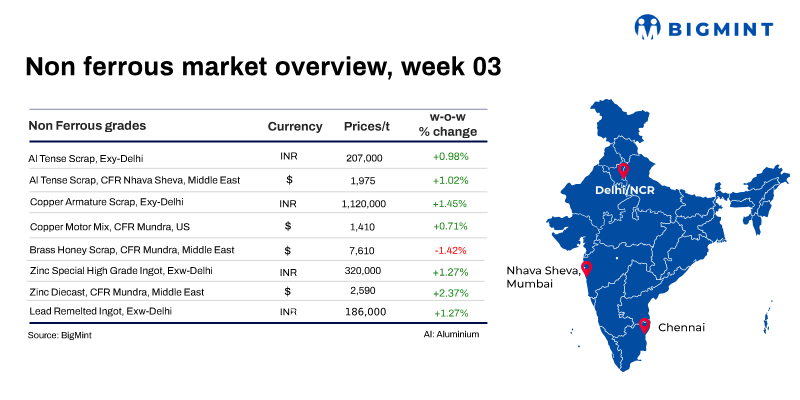

India’s imported aluminium scrap prices strengthened in the week ended 17 January, supported by a rise in prices on the LME, steady buying interest, and firm global aluminium sentiment.

BigMint assessed Middle East-origin Tense (8-9%) at $1,975/t, up $20/t w-o-w, while Middle East-origin Extrusion 6063 rose $100/t to $2,900/t, driven by improved demand for higher-grade material.

Domestic aluminium prices in India continued to strengthen w-o-w. According to BigMint’s assessment, domestic aluminium ingot prices in Delhi rose by INR 7,000/t, or 2%, w-o-w to INR 322,000/t as of 15 January.

India’s aluminium scrap imports have more than doubled over the past decade, reaching a record level of around 2 million tonnes (mnt) in 2025, highlighting the country’s increasing reliance on scrap to support secondary aluminium and alloy production.

India’s ADC12 aluminium alloy ingot prices strengthened y-o-y in CY’25, supported by firmer domestic market fundamentals. Average OEM ADC12 prices in Delhi increased 5.4% from INR 213,875/t in CY’24 to INR 225,375/t in CY’25.

Imported copper scrap prices in India fell w-o-w in the week ended 17 January, tracking a mild correction in LME copper futures. Meanwhile, domestic copper scrap prices showed mixed trends w-o-w.

According to BigMint’s assessment, Birch Cliff scrap was assessed at $11,870/t, down by 3.5% w-o-w, while US motors mix stood at $1,410/t (both CFR Mundra), slightly up by 1% w-o-w.

India’s copper scrap imports surged 38% y-o-y in CY’25 to 440,668 t from 319,415 t in CY’24, reflecting a sharp rise in reliance on secondary raw materials.

The Indian zinc scrap market witnessed mixed price movements during the week ending 17 January, tracking a combination of firmer global cues and stable domestic demand. While imported scrap prices remained unchanged, select domestic by-products moved in opposite directions, reflecting supply-side dynamics rather than demand erosion.

BigMint assessed zinc diecast scrap (Middle East origin) at $2,530/t CFR west coast India, unchanged w-o-w.

Domestic zinc spot prices stood at INR 320,000/t exw-Delhi, up by 1.27% w-o-w. HZL zinc prices were up by 1.56% w-o-w at INR 327,400/t ex-Chanderiya.

Lead

Domestic primary lead ingot prices stood at INR 196,000/t, up by 1.08% w-o-w, while re-melted ingots stood at INR 186,000/t, up by 1.08% w-o-w.

Meanwhile, HZL lead prices stood at INR 217,200/t ex-Chanderiya, up by 1.3% w-o-w.

Other updates

Japanese aluminium premium jumps on tightening global supply

The Japanese aluminium premium for Q1CY’26 was settled at $195/t, up sharply by 127% q-o-q, marking the first quarterly increase in a year as global supply tightened amid smelter outages and power-related disruptions. Negotiations were prolonged due to a wide buyer-seller gap, with the final level reflecting a compromise as buyers resisted prices above $200/t. Despite muted domestic demand, elevated overseas premiums and declining global inventories supported the surge, reinforcing Japan’s role as a key benchmark market. Premiums are expected to remain firm in Q2CY’26, supported by ongoing supply constraints and strength in LME aluminium prices.

Kipushi zinc mine meets CY’25 target; Ivanhoe raises CY’26 outlook

Ivanhoe Mines announced that the Kipushi zinc mine in the Democratic Republic of Congo has met its CY’25 target, delivering a record 203,168 t of concentrate. Output remained within the guided range of 180,000-240,000 t, supported by stable mining and processing operations. Additionally, on the back of strong performance, Ivanhoe lifted its 2026 production guidance to 240,000-290,000 t. December 2025 data suggest an annualised production rate exceeding 270,000 t.

China announces measures to boost battery recycling from EVs

China has announced new interim measures to strengthen the recycling and comprehensive utilisation of used power batteries from new energy vehicles (NEVs), effective 1 April 2026. The rules mandate battery coding, digital identity cards, and full life-cycle traceability, while extending recycling responsibility to battery and EV manufacturers. Non-compliance may attract fines of up to RMB 50,000. Notably, China’s rapidly expanding NEV fleet exceeded 20 million by 2024.

Leave a Reply