- HRC prices stable, rebar prices rise w-o-w

- Raw material prices remain mixed

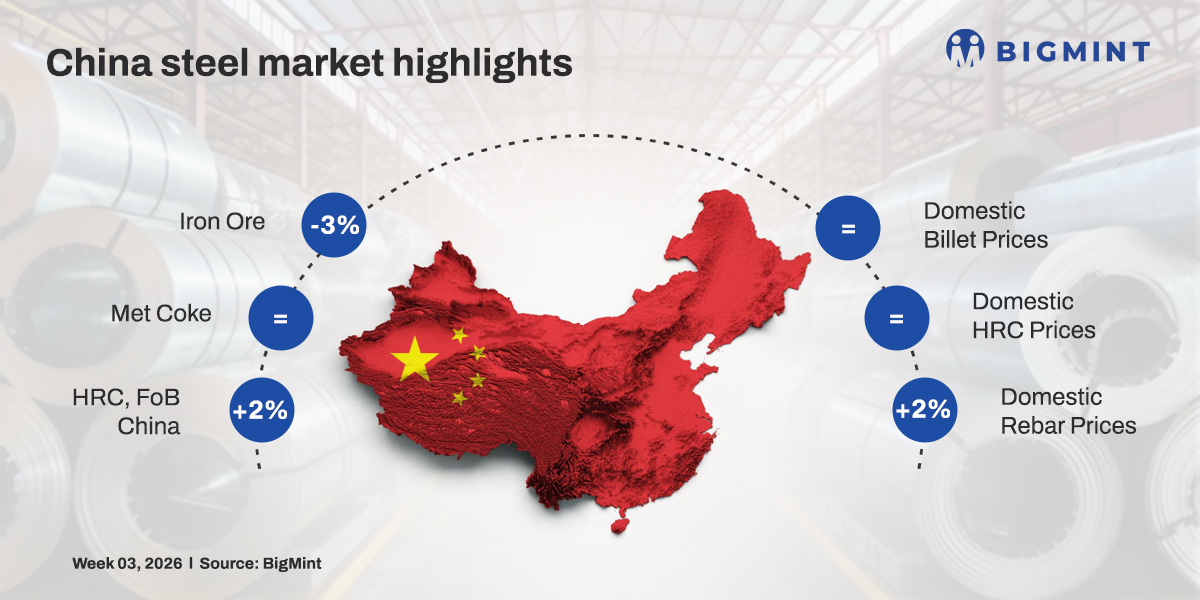

China’s steel prices remained mixed in the week ended 16 January, with domestic hot-rolled coil (HRC) prices remaining unchanged w-o-w, while rebar prices rose marginally. Raw materials, including iron ore prices declined slightly, while billet prices remained stable and coking coal prices increased w-o-w.

The China Iron and Steel Association (CISA) reported that total steel inventory at key Chinese enterprises reached 15.04 million tonnes (mnt) in early-January 2026 (1-10 January), an increase of 900,000 tonnes (t) or 6.4% against 14.14 mnt in late-December 2025.

Furthermore, China’s steel exports reached an all-time high of 119.01 million tonnes (mnt) in 2025, up by 7.5% y-o-y from 111.01 mnt in the same period last year, according to the General Administration of Customs.

Moreover, in December 2025, steel exports stood at 11.30 mnt, marking the highest monthly volume of the year and an increase of 16.2% y-o-y from 9.72 mnt in December 2024. On a m-o-m basis as well, steel exports rose by 13.2% from 9.98 mnt in November 2025.

1.Iron ore spot prices edge down w-o-w: Iron ore fines benchmark prices for Fe 61% dipped by $3/t w-o-w to $106/dmt CFR China on 16 Jan. Prices declined despite ongoing restocking activity for the Lunar New Year, with recent trades indicating widening discounts or weakening premiums for some medium-grade fine cargoes. With short-term demand met, fewer mills are expected to make purchases to complete restocking ahead of the holiday.

a) Spot pellet premium stable w-o-w: Spot pellet premium for Fe 65% grade pellet remained firm at $17.8/t CFR China on 14 January.

b) Spot lump premium dip w-o-w: Spot lump premium edge down w-o-w to $0.045/dmtu on 16 January.

2. China met coke producers signal price hike amid rising coking coal costs: Chinese met coke producers are expected to raise their offers by approximately RMB 50-55/t ($ 7-8/t), following a series of four price reductions earlier this year. The anticipated increase is primarily driven by the recent surge in raw material costs, particularly coking coal.

On the cost front, Australian Premium Hard Coking Coal (PHCC) prices rose sharply by $ 14/t, reaching $ 232/t FOB, while the BigMint’s PHCC index climbed $ 9/t week-on-week to $ 247/t CNF Paradip as of 16 January 2026. The rising coal prices have significantly increased production costs for met coke manufacturers, necessitating upward price adjustments to maintain margins.

3. China’s billet prices remain stable w-o-w: Chinese billet prices were unchanged w-o-w at RMB 2,970/t (~$426/t) during 9–16 January, as weak winter demand and rising inventories continued to cap upside. Mills largely controlled supply, preventing further downside, while spot trading remained slow due to muted buying interest ahead of the Chinese New Year. Overall, the physical billet market stayed stable but subdued, with participants adopting a cautious, wait-and-watch approach.

SHFE rebar futures rose w-o-w by RMB 33/t (~$5/t) to RMB 3,141/t (~$451/t), recovering from early-week pressure. Initial weakness from soft demand, logistics issues, and easing raw material prices gave way to improved sentiment toward the end of the week, supported by policy expectations, firmer export sentiment, and higher offers from northern mills. Futures outperformed the spot market, signaling selective optimism, even as underlying demand conditions remained fragile.

4. Domestic HRC prices remain stable w-o-w: Domestic HRC prices in China remained unchanged w-o-w at RMB 3,100/t ($445/t) on 16 January 2026, in line with largely steady SHFE HRC futures (May 2026 contract), which stood at RMB 3,324/t ($477/t) on 16 January, unchanged from the previous week. Meanwhile, China’s HRC export offers rose by $8/t w-o-w to $473/t FOB on 13 January, from $465/t FOB a week earlier.

Overall, China’s domestic steel market remains mixed. Inventories have increased slightly, with rises in pig iron and crude steel output. However, demand remained weak due to the subdued consumption, though supportive monetary policies and targeted economic measures are providing modest support to prices.

5. Rebar prices rise w-o-w: China’s rebar prices edged up by RMB 50/t ($7/t) w-o-w to RMB 3,190/t ($/458t) on 16 January from RMB 3,140 ($451/t) a week earlier, tracking gains in SHFE futures. The SHFE futures (May 2026 contract) rose by RMB 27/t ($4/t) w-o-w to RMB 3,173/t ($455/t) on 16 January from RMB 3,146/t ($451/t) on 9 January 2026.

China’s Shagang Steel has continued to keep its long steel prices flat for mid-Jan’26 sales, with no price revisions announced since 11 Sept’25. Prices of rebars, coiled rebars, and wire rods are as follows:

- Rebars (16-25 mm): RMB 3,450/t ($495/t)

- Coiled rebars (8-10 mm): RMB 3,560 ($511/t)

- Wire rods (6-10 mm): RMB 3,470/t ($498/t)

Outlook

China’s steel market is expected to remain volatile in the coming week, with policy-driven optimism providing some support while demand fundamentals remain weak. Prices remain mixed, and a clearer market direction is likely to emerge only as demand trends become more visible.

Leave a Reply