- GST reforms boost IF-rebar tags, cause caution in coal markets

- Trade-level HRC market remains subdued amid weak demand

The domestic steel market reflected cautious sentiment in week 36 (1-6 September 2025). Pellet prices softened; ferro alloys, except for ferro chrome, witnessed corrections; coal and ferrous scrap stayed stable; semi-finished and long steel showed mixed movements; and flat steel remained range-bound amid weak demand.

Iron ore, pellet

PELLEX, BigMint’s bi-weekly domestic pellet (Fe63%) index for Raipur, decreased by INR 200/tonne (t) w-o-w to INR 10,150/t ($115/t) DAP on 5 September. Deals for around 47,000 t were recorded in the Raipur market at revised offers from local suppliers. Raipur-based pellet producers reduced their offers for Fe 63/63.5% (+/-0.5%) material by INR 200/t ($2/t) to INR 10,000-10,300/t ($113-117/t) exw a couple of days back.

BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index remained largely stable w-o-w at $65.5/t FOB east coast on 4 September, with 220,000 t booked. The hike in vessel freights kept FOB prices stable, while CNF tags rose w-o-w. Discounts for Indian-origin 57% Fe fines were at around 17-18% in the overseas market, though negotiations remain ongoing.

AM/NS sold 300,000 t of iron ore of the 352,000 t offered from Odisha on 3 Sep’25. Premiums of up to INR 400/t were recorded. From Thakurani mines, 120,000-t fines (Fe 57-59%) were booked at INR 3,600-4,600/t (INR 100/t premium), and 48,000-t lumps (5-18 mm, Fe 56.5-59%) remained unsold. From Sagasahi mines, 52,000-t lumps (5-18mm, Fe 58.5-62.5%) were booked at INR 5,925-7,250/t and 132,000-t fines (Fe 53.5-56.5%) at INR 2,775-3,600/t against base prices INR 5,800-7,000/t and INR 2,350-3,400/t, respectively (including royalty).

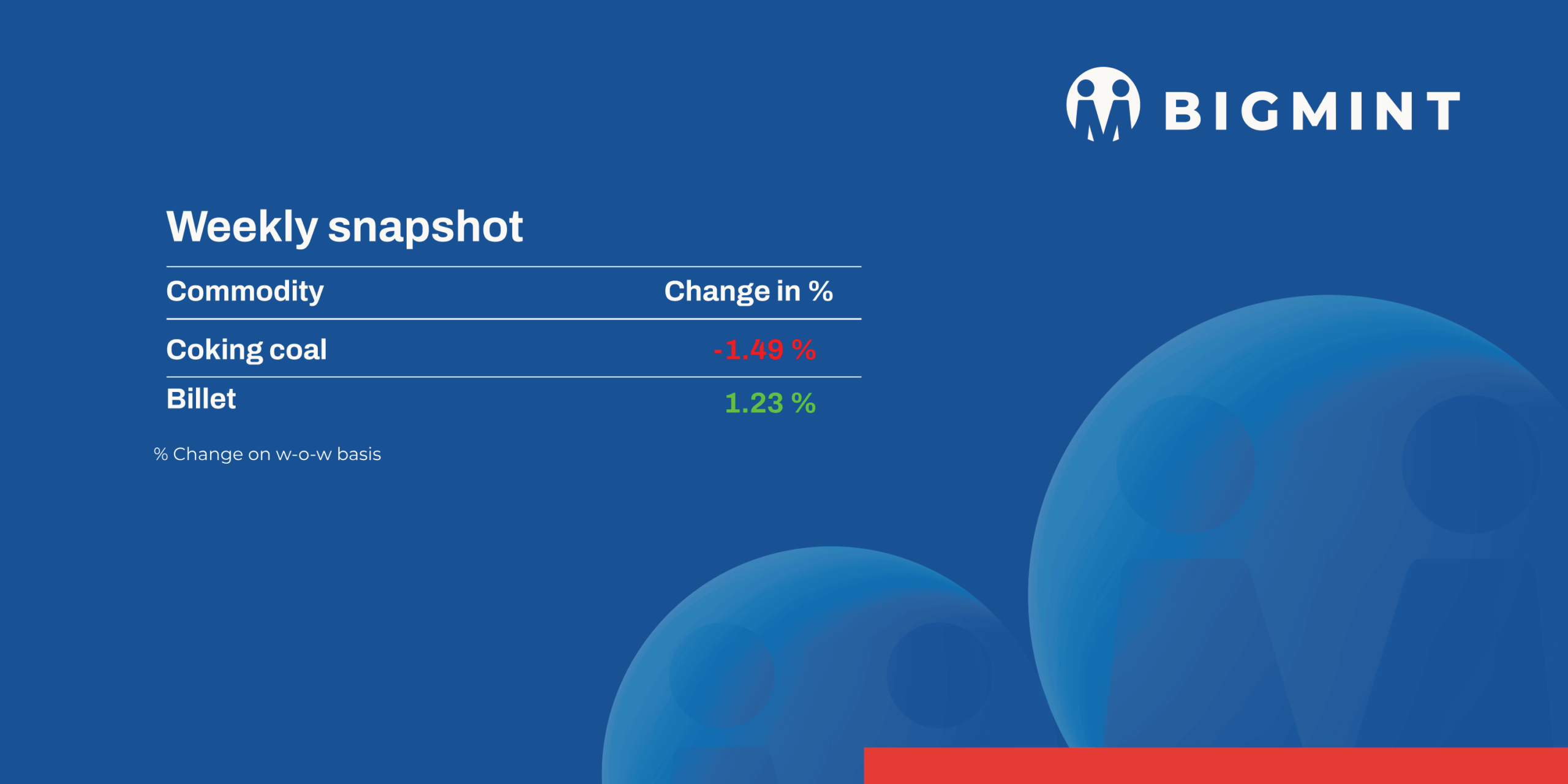

Coal

South African RB2 and RB3 prices at Gangavaram stayed flat w-o-w at INR 8,300/t and INR 7,200/t. Sellers rushed to liquidate limited port stocks before the 22 September GST deadline, while buyers held back, awaiting fresh offers. The GST hike to 18% and cess removal kept the market in wait-and-watch mode, as participants awaited clarity on its impact on steelmaking.

Domestic coal prices in India held steady w-o-w this week, with 5,000 GCV assessed at INR 5,750/t ex-Bilaspur and 4,500 GCV at INR 4,900/t. Market focus remained on GST changes, with rates raised to 18% and the INR 400/t cess removed. The effect stayed mixed — lower grades showed slight relief, while mid- to higher-grade coal turned relatively costlier, keeping overall market sentiment cautious.

The Indian met coke market held steady this week, with BF-grade prices at INR 29,000/t in Jajpur and INR 30,000/t in Gandhidham, while foundry-grade stood at INR 35,600/t in Rajkot. Offers remained firm as coking coal costs provided little relief, but buyers showed resistance amid weak steel demand. Pig iron auctions saw some improvement, yet overall demand was muted. Chinese market sentiment softened on a weak steel outlook. In the near term, India’s met coke market is expected to track global coking coal trends with a cautious tone.

Ferrous scrap

India’s imported ferrous scrap market stayed subdued through the week as a strong dollar, weak sentiment, and heavy monsoon rains weighed on activity. Shredded offers held near $365/t CFR, while HMS 80:20 ranged within $325-345/t CFR, though bids stayed lower. Busheling above $375/t met resistance, and turnings hovered at $300-315/t CFR.

Floods in Ludhiana and festive slowdowns in Maharashtra further curbed demand, leaving both imported and domestic scrap trades muted. Buyers remained cautious amid weak finished steel offtake, with restocking expected to stay limited in the near term.

Approximately 3,000 t of imported scrap were booked in the last seven days, including 2,000-2,500 t of HMS 80:20 priced between $328-340/t.

Ferro alloys

Silico manganese: Indian silico manganese prices (60-14) decreased by INR 500/t ($6/t) w-o-w to INR 69,500-69,600/t ($789-790/t) in the key regions of Durgapur, Raipur, and Vizag. Silico manganese prices stayed under pressure due to weak demand and rising inventories, but high input costs limited further decline.

Ferro manganese: Indian ferro manganese (HC 70%) prices dipped by INR 100/t ($1/t) w-o-w to INR 70,300/t ($800/t) exw in Durgapur. However, prices, exw-Raipur, remained unchanged at INR 70,600/t ($802/t) w-o-w. A slight decline was observed due to moderate demand weakness and increased supply from select regional producers in the Durgapur market.

Ferro silicon: Indian ferro silicon prices dropped by INR 400/t ($5/t) w-o-w to INR 91,200/t ($1,035/t) exw-Guwahati. Meanwhile, Bhutan’s offers dipped by INR 900/t ($11/t) to INR 92,100/t ($1,046/t) exw. Muted demand, sufficient inventories, and cautious buying led to reduced trade and a slight price correction this week.

Ferro chrome: Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices increased by INR 4,200/t ($48/t) w-o-w to INR 113,700/t ($1,291/t) exw-Jajpur. The price rise was driven by limited market participation, as most major sellers withheld offers, leading to tighter supply and upward pressure on prices.

Semi-finished steel

Indian semi-finished steel prices showed a fluctuating trend as per BigMint’s assessment.

Billets: Domestic billet prices in all key locations showed mixed sentiments. Prices in some regions moved up, as in the middle of the week, trade was boosted by the GST 2.0 reform. Prices increased by INR 200-350/t ($2-4/t) in most regions; others witnessed a drop of INR 200-500/t ($2-6/t).

Sponge iron

Sponge iron prices also witnessed a mixed trend, as purchasing interest was largely confined to immediate needs, reflecting the prevailing cautious mood. Almost all key locations were up INR 150-550/t ($2-6/t), while Durgapur, Ramgarh and Jharsugda witnessed a drop of INR 50-400/t ($1-5/t).

India’s sponge iron export market remained under slight pressure this week amid a persistent domestic downtrend. Export offers to Nepal slipped by $1/t w-o-w to $329/t CPT Raxaul, while those to Bangladesh declined by $3/t, settling at $339/t CPT Benapole. Buying activity was limited, with deals for about 4,500 t concluded for Nepal and Bangladesh.

Pig iron

SAIL’s Bokaro Steel Plant (BSL) held an auction for 3,000 t of steel-grade pig iron on 3 September. The total volume was booked at an average price of INR 32,300/t exw ($366). Bids increased by around INR 600/t ($7) from the previous auction held on 30 August, in which 3,000 t were booked, out of the 6,000 t offered, at an average price of INR 31,730/t ($360) exw.

SAILs Rourkela Steel Plant (RSP) conducted an auction on 5 September for 5,000 t of steel-grade pig iron, in which 3,500 t were booked at an average price of INR 32,800/t ($372)exw. This marked a decrease of INR 650/t ($7) compared to the previous auction on 13 August, in which the entire volume of 1,200 t was sold at INR 33,450/t ($379) exw.

Finished long steel

IF-rebar: In the initial days of the week, India’s IF-route finished long steel market experienced a slowdown due to weak market sentiment and a lack of fresh inquiries. Manufacturers were forced to reduce their prices to liquidate inventories. However, prices increased in the latter half due to positive sentiments from the GST Council meeting. Additionally, prices had been supported by shortages of raw material (sponge iron) in a few markets. As per the current scenario, the inventory pressure in the market remains considerable, and prices are expected to move within a narrow range.

On a w-o-w basis, rebar prices fluctuated by INR 100-800/t across regions, as per BigMint’s assessment.

Trade reference prices of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size were assessed at INR 39,300-39,700/t exw-Raipur and INR 43,600-44,200/t exw-Jalna. Trade reference prices of heavy structural steel for base size 150-mm channel stood at INR 41,800-42,200/t exw-Raipur.

Trade reference prices of wire rod hovered at INR 40,300-40,800/t ex-Raipur.

BF-rebar: Some leading primary mills increased rebar prices by INR 1,000/t ($11/t) for early-September 2025 deliveries as against prices prevailing in end-August, sources informed BigMint. Meanwhile, some mills rolled over their prices. Post-revision, list prices stood at INR 47,500-48,500/t ($538-549/t) on landed basis.

Trade-level BF rebar prices remained stable w-o-w at INR 47,300/t ($536/t) exy-Mumbai, as per BigMint’s assessment on 5 September 2025. Demand remained sluggish in the trade channel last month, as heavy monsoons and waterlogging disrupted logistics and hampered market activity. In the projects segment, prices opened at INR 46,000-47,000/t ($521-532/t) FOR Mumbai basis.

Flat steel

Trade-level prices of hot-rolled coils (HRCs) in India remained range-bound w-o-w at INR 49,000-51,000/t ($556-579/t). Similarly, cold-rolled coil (CRC) prices held steady w-o-w, ranging within INR 55,300-59,000/t ($627-669/t).

The trade-level HRC market remained subdued amid weak demand. Prices were range-bound w-o-w, reflecting the lack of momentum in the market.

India’s bulk imports of HRCs touched 381,189 t as of 30 August, based on vessel line-up data. Around 248,786 t of additional cargoes are expected by the end of September.

India’s bulk exports of HRCs touched 226,837 t as of 30 August, based on vessel line-up data with BigMint. Moreover, around 12,700 t of additional cargo are being shipped.

Leave a Reply