- CIS export prices slip amid muted trade

- UAE billet demand rises on stronger rebar momentum

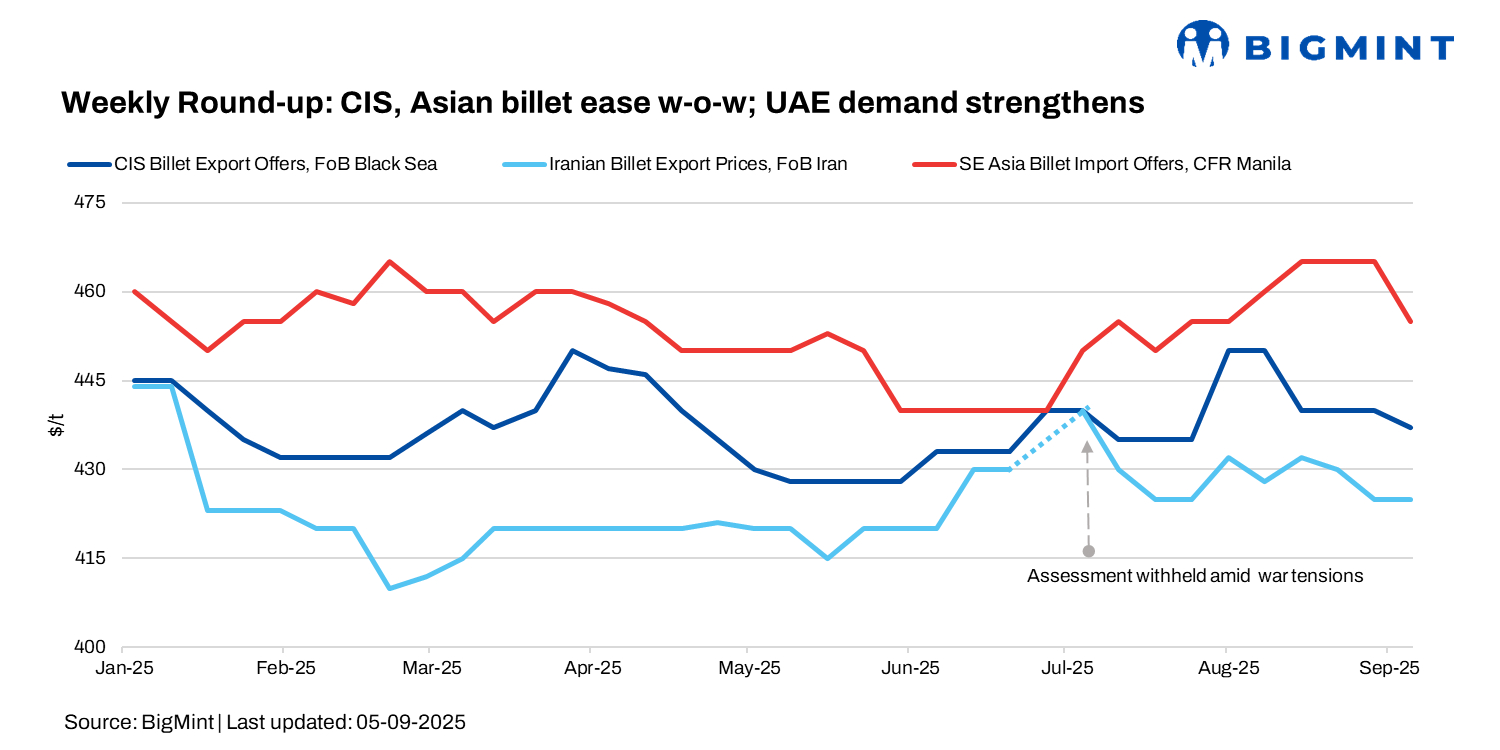

In the 36th week of 2025, global billet prices continued to ease. Major Russian mills held back October offers, keeping availability thin, while Turkish buyers stayed cautious with price ideas at $425-430/t FOB ($450-455/t CFR).

In Asia, increased competition from Chinese suppliers kept sentiment weak, with the latest confirmed deal at $455/t CFR Philippines for 30,000-40,000 t of 5sp 150 mm billets dragging the new workable levels to $455/t from last week’s $460-465/t.

Meanwhile, Turkiye’s imported scrap market remained largely steady. US/Baltic-origin HMS 80:20 traded at $340-345/t CFR, while EU cargoes were assessed at $334-338/t CFR. Rising freight costs from the US to Turkiye and softening rebar prices added further pressure, prompting some sellers to divert cargoes to Europe.

Market highlights

CIS regions: CIS billet export prices slipped $3/t w-o-w to $437/t FOB Black Sea amid muted activity, while major Russian mills held back fresh offers pending October price decisions.

Turkish buyers stayed on the sidelines, targeting $425-430/t FOB ($450-460/t CFR) as weaker Kardemir sales and Chinese competition weighed on sentiment.

In contrast, the Far East saw firmer activity with a 26,000 t sale at $430-435/t FOB for October shipment, up from $410-415/t FOB two weeks earlier. Overall, cautious sentiment prevails as buyers expect further price pressure across key regions.

Iran: Iran’s billet prices climbed 10,000 rial/kg w-o-w to 343,500 rial/kg, while rebar slipped 2,000 rial/kg to 383,000 rial/kg. Billet gains were supported by limited supply and high production costs despite weak demand and political uncertainty. Rebar eased slightly as sentiment stayed cautious amid sanctions risks, exchange rate volatility, and concerns over power and gas shortages ahead of winter.

On the export side, activity remained muted with offers from major suppliers at $420-430/t FOB and one IF-based mill targeting $410/t FOB for September shipment. Some traders quoted as low as $390-395/t FOB, though such levels are seen as unworkable.

Key producers, including KSC and SISCO, are expected to return with tenders in the coming weeks. Early September indications placed billet at $425-430/t FOB and slabs at $405-410/t FOB.

UAE: Stronger rebar demand lifted billet procurement in the UAE, with GCC suppliers meeting most requirements. A local producer sold about 20,000 t at around $500/t exw, while mills from Oman and Qatar supplied bulk volumes, including extra intake by an integrated mill ahead of maintenance.

Imports also saw activity, with Chinese 3sp billet booked at $460-465/t CFR for October shipment and Indonesian offers heard at $480/t CFR, though certification remains a hurdle. Reports of Iranian billets reclassified as Omani are unconfirmed.

Buyers are targeting $460/t CFR, but suppliers are pushing prices towards $500-510/t delivered amid expectations of stronger Q4 construction demand.

China: Tangshan billet prices slipped RMB 20/t ($3/t) w-o-w to RMB 2,990/t. Early in the week, prices dropped RMB 60/t ($8/t) to RMB 2,950/t amid weaker raw materials, falling rebar futures, and fragile demand despite the peak season. Inventories climbed to a 3-month high as steel output rose, while rebar demand stayed sluggish and exports to Southeast Asia and Africa slowed.

Mid-week stability was followed by a weekend rebound of RMB 30-50/t, supported by post-holiday restocking, firmer coking coal, and policy rumours. Still, flat steel buying outperformed longs, and uncertainty over September demand lingers with high stocks and muted construction activity.

Leave a Reply