- Mills hike BF rebar prices by $6-11/t w-o-w

- Billet prices tick up on positive trade momentum

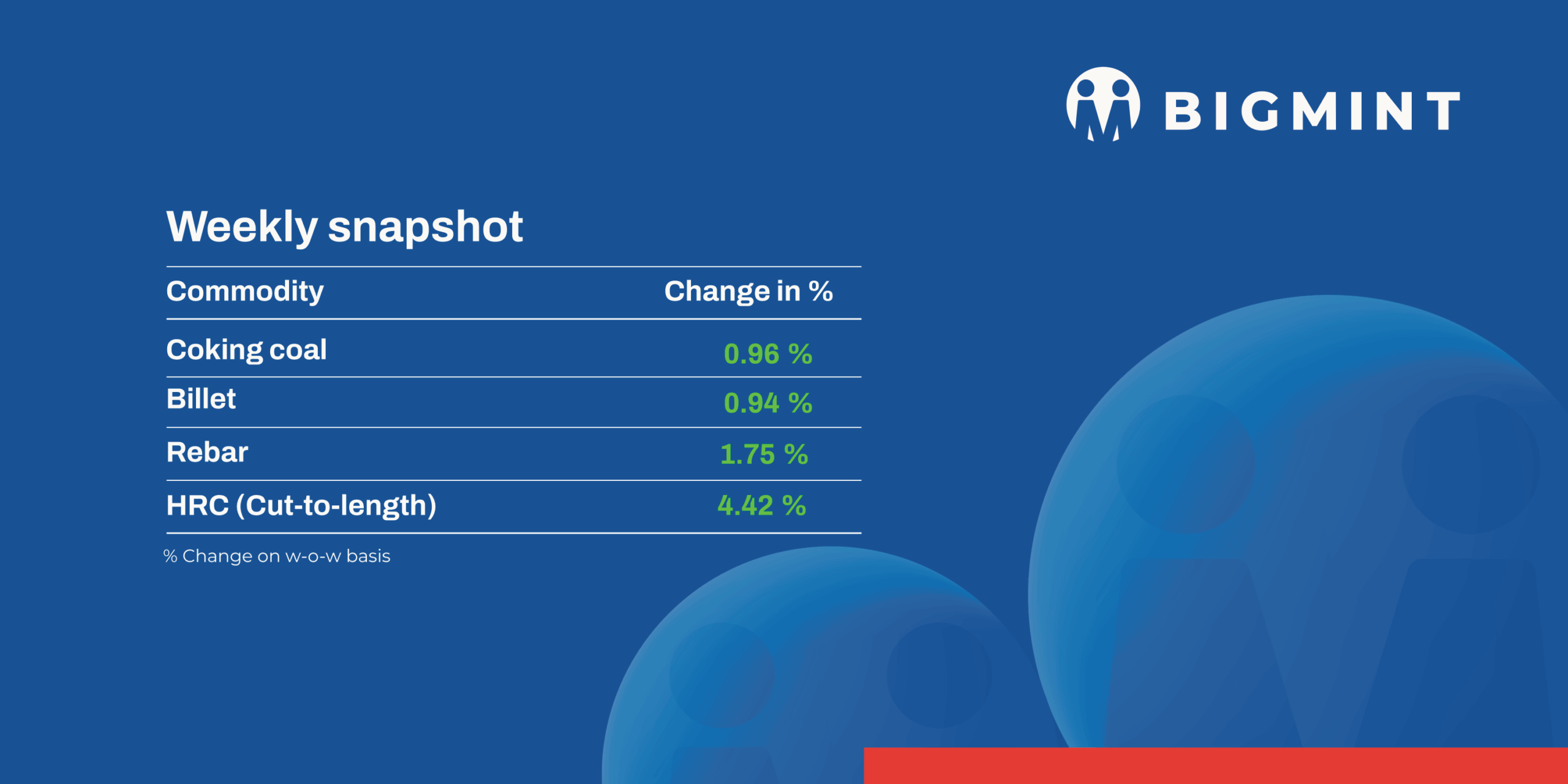

The domestic steel market witnessed a positive price trend during week 52 (22–26 December 2025), with semi-finished steel prices increasing by INR 100-700/t.

Iron ore and pellet

- PELLEX, BigMint’s bi-weekly domestic pellet (Fe63%) index for Raipur, increased by INR 100/t ($1/t) to INR 9,500/t ($106/t) DAP on Friday compared to the previous assessment on 19 December. Raipur-based pellet producers have increased offers for Fe 62.5% (+/-0.5) pellets by INR 100/t ($1/t) to INR 9,300-9,400/t ($104-105/t) exw. Meanwhile, producers such as Godawari have recently raised prices by INR 100/t ($1/t) to INR 9,500/t ($104/t) and 10,700/t ($119/t) exw for Fe 62.5% and Fe 64.5%, respectively. The sudden spike in sponge iron and finished steel offers led to the hike in pellet prices.

- NMDC conducted an auction for 83,000 t of run of mine (ROM) iron ore from its Bacheli mines in Chhattisgarh on 23 December. Around 45,000 t of ROM (10-150 mm, Fe 65.5%) was booked against the base price of INR 5,500/t. Prices were FOR/FOT basis, inclusive of royalty, DMF, and NMEDT charges.

- BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export prices increased by $0.5/tonne (t) w-o-w to $67.5/t FOB east coast on Wednesday. BigMint heard approximately 370,000 t of export deals during this assessment period, which were primarily concluded for below-Fe 55% fines at 25-26% discounts. Discounts now being offered are around 20-21% for Fe 57% fines cargo, while exporters are still targeting 19%, which is not attracting buyers toward fresh deals. While Fe56% cargoes were reported to fetch discounts in the range of 22-23%.

Coal

- South African thermal coal prices softened amid weak year-end buying. RB2 (5,500 NAR) ex-Paradip, Vizag, and Gangavaram declined to INR 8,850–8,900/t, while RB3 (4,800 NAR) eased to INR 7,500/t ex-Vizag and held at INR 7,550/t at Paradip and Gangavaram. The downward correction followed a drop in freight rates to around $12 from $14. International trading activity remained limited due to Christmas and New Year holidays.

- Domestic coal prices remained stable during the week. 5,000 GCV material was assessed at INR 5,750/t, while 4,500 GCV stayed unchanged at INR 4,800/t w-o-w. Coal availability was adequate across key consuming regions, reducing procurement urgency. Buying remained largely need-based, even as downstream sentiment showed slight improvement. A balance between steady supply and cautious demand kept prices rangebound.

- India’s metallurgical coke market stayed largely steady in the week ended 24 December, with cost pressures offset by subdued demand. BF-grade met coke prices remained unchanged at INR 32,000/t ex-Jajpur in the east and INR 29,800/t ex-Gandhidham in the west. Foundry-grade prices softened by INR 600/t w-o-w to INR 35,200/t ex-Rajkot due to weak offtake. Producers continued to face margin pressure as Australian premium hard coking coal prices increased to $218/t FOB, up $1/t w-o-w.

- Premium hard coking coal prices into India were unchanged during the week, with the PHCC index assessed at $238/t CNF Paradip on 26 December. Market activity remained muted during the Christmas holiday period, with no fresh trades reported. Participants noted that global inactivity kept prices stable, while supply-side risks lent support as heavy weather in Australia’s Moranbah region disrupted mining operations and logistics.

Ferrous scrap

- India’s imported scrap market remained subdued throughout the week. Buying interest stayed selective. UK-origin shredded scrap was heard around $345-350/t CFR, while HMS 80:20 levels hovered near $318/t CFR Nhava Sheva/Chennai, largely stable.

- Supplier activity remained thin due to Christmas and year-end holidays, limiting trade momentum. Although a few spot transactions were concluded, bid-offer gaps persisted, especially for HMS grades, preventing any meaningful pickup in volumes despite steady price indications.

- Approximately 3,000-4,000 t of imported scrap were reported to have arrived in India during the week, including around 1,500-2,000 t of HMS 80:20, while the balance comprised shredded, PNS, HMS bales, LMS bales, and HMS 90:10.

Ferro alloys

- Silico manganese: Indian silico manganese (60-14) prices edged up by INR 150/t ($2/t) w-o-w to INR 68,600- 69,700/t ($764-776/t) across Durgapur, Raipur, Vizag and Raigarh, supported by need-based buying. However, subdued steel demand and cautious market sentiment prompted mills to adopt a strategic, wait-and-watch procurement approach amid short-term price uncertainty.

- Ferro manganese: Indian ferro manganese (HC 70%) prices dropped w-o-w by INR 100/t ($1/t) to INR 70,800/t ($788/t) in Durgapur and decreased by INR 300/t ($3/t) to INR 71,300/t ($794/t) in Raipur. Prices declined due to need-based buying from consumers, with limited spot demand and cautious procurement amid sufficient inventories.

- Ferro silicon: Indian ferro silicon (Si 70%) prices edged down by INR 300/t ($3/t) w-o-w to INR 96,700/t ($1,077/t) ex-works Guwahati, while prices in Bhutan fell by INR 1,500/t ($17/t) to INR 95,500/t ($1,063/t). Prices softened across both regions, weighed down by lower-priced transactions amid cautious buying and weak demand.

- Ferro chrome: Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices edged down by INR 900/t ($10/t) to INR 106,500/t ex-works Jajpur, as year-end slowdown limited market activity and participants were also re-evaluating offers and bids post OMCs chrome ore auction. Meanwhile, SAIL’s Salem Steel Plant issued a tender to procure 1,200 t of high-carbon ferro chrome (Cr 57-63%, C 5-8%, 10-70 mm), with the submission deadline set for 5 January.

Semi-finished

- India’s semi-finished steel segment recorded a notable recovery during the week, with billet prices increasing by INR 300-1,100/t across major markets. The uptrend was primarily driven by improved buying interest and a sharp rise in enquiries from neighbouring regions. Ahmedabad emerged as the key gainer, with prices rising by around INR 1,100/t, supported by stronger billet bookings and improved finished steel demand. Trade activity remained moderate to high, indicating improved market liquidity. Sellers maintained a firm stance, while buyers stepped up procurement amid positive demand expectations.

- The sponge iron market also reflected strengthening sentiment, as prices rose by INR 100–700/t w-o-w. Higher enquiry levels and improved trade activity underpinned the price gains. Sellers remained optimistic, while buyers actively procured material in response to better finished steel sales. Overall, improved demand visibility and steady procurement supported a positive market outlook during the week.

Finished long steel

- IF-rebar: India’s Induction Furnace (IF) route rebar prices moved up w-o-w. Trading activity remained moderate, as manufacturers continued to quote higher offers. Buyers stayed active backed by steady demand from the project segment and retail markets. Dispatches of previously booked material were smooth, restricting the scope for further discounts from manufacturers. Mill inventories remained comfortable at around 8-12 days across regions. Given the current scenario, market participants expect the market to remain supportive in the near term.

- On a weekly basis, rebar prices increased in the range of INR 300-1,300/t across the regions, as per BigMint assessment.

- The trade reference price of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size was assessed at INR 40,500-40,900/t exw Raipur, INR 45,400-46,000/t exw Jalna.

- Trade reference price of heavy structural steel for base size 150mm channel stands at INR 42,500-43,000/t exw Raipur.

- Trade reference prices of wire rod are hovering at INR 41,200-41,800/t ex Raipur.

- BF-rebar: Indian Tier-I mills have increased rebar prices by INR 500-1,000/t ($6-11/t) for end-December deliveries, sources informed BigMint. Post-revision, list prices stood at INR 48,000-49,500/t ($536-553/t) on a landed basis.

- Trade-level BF rebar prices rise w-o-w by INR 1,500/t to INR 49,000/t exy-Mumbai, as per BigMint’s assessment on 26 December. Prices exclude GST at 18%.

- In the projects segment, prices hovered at around INR 47,000-48,000/t ($525-536/t) FOR Mumbai basis.

Flat steel

- Trade-level prices of hot-rolled coils (HRCs) in India surged w-o-w on 23 December to INR 47,500-49,900/t ($530-557/t). Additionally, cold-rolled coil (CRC) prices rose sharply w-o-w to INR 55,100-57,000/t ($578-636/t).

- Indian HRC prices surged this week in a sharp departure from the downward trajectory observed over the past few months. The steep rise was precipitated by list price hikes by major mills in mid-December. However, market activity was largely need-based, with buyers procuring cautiously as prices firmed up.

- India’s bulk imports of HRCs touched 211,350 t as of 19 December, based on vessel line-up data. Around 112,899 t of additional cargoes are expected by early-January.

- India’s bulk exports of HRCs touched 219,573 t as of 19 December, and around 87,906 t of additional cargo are in transit.

- BigMint’s India HRC (S275) export index for the European Union (EU) remained stable w-o-w at $520/t FOB main port, as market activity remained stable with participants entering holiday mode ahead of the Christmas celebrations. Moreover, India HRC (SAE 1006) export index for the Middle East remained unchanged w-o-w at around $465/t. A source told BigMint: “Demand in the region remained slow ahead of the upcoming Christmas holidays.

Leave a Reply