- Smelter disruptions underpin market sentiment globally

- Inventories decline across key regions globally

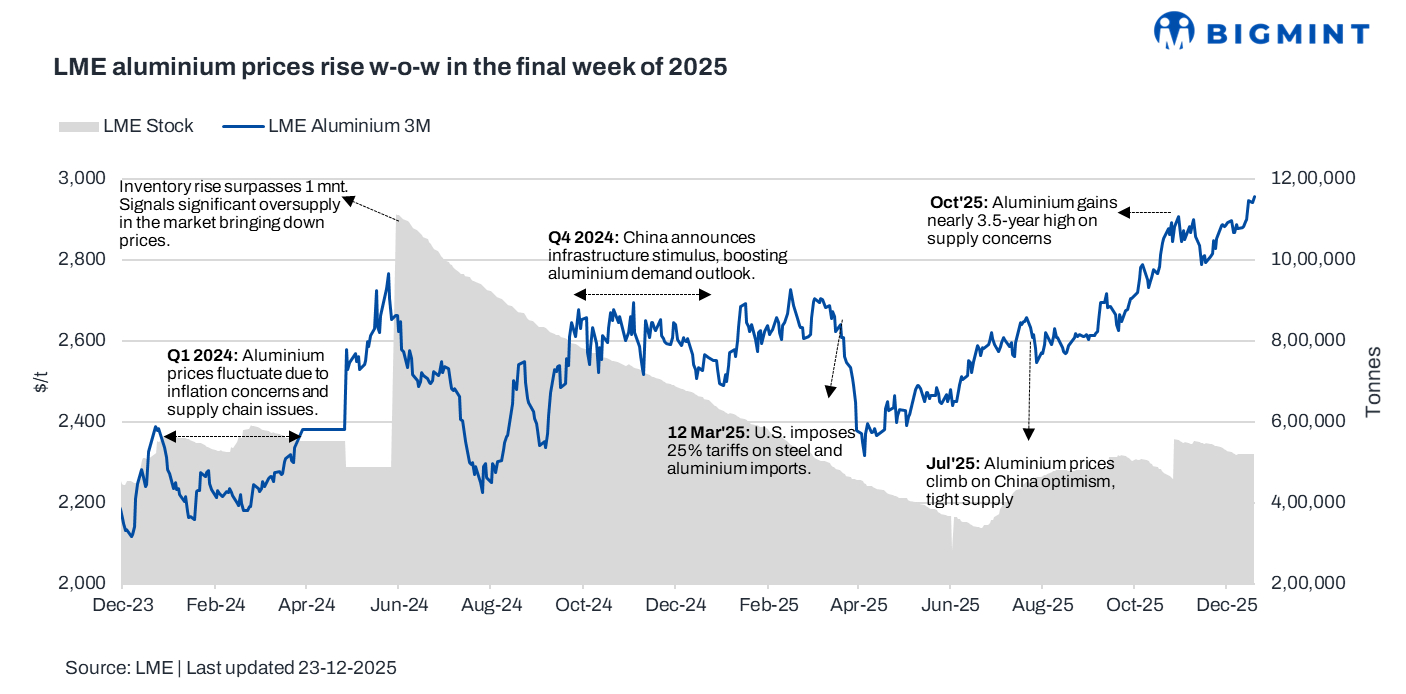

Aluminium prices on the London Metal Exchange (LME) edged higher during the week ended 26 December, supported by tightening global supply expectations. Prices were underpinned by confirmed smelter disruptions, declining inventories across key regions, falling Japanese port stocks, and firmer physical premiums, which outweighed lingering demand concerns. However, trading activity was limited as the LME remained closed on 25 and 26 December for the Christmas holidays. Prices rose in the early part of the week before stabilising toward the end amid thin liquidity.

Pricing, inventory trends

LME aluminium prices averaged $2,950/t in the week ended 26 December, up $50/t or 1.7% w-o-w. Prices opened the week at around $2,942/t and strengthened to close at $2,955/t on 23 December. Trading activity was limited in the latter part of the week, as the LME remained closed on 25 and 26 December for the Christmas holidays.

Meanwhile, LME aluminium inventories witnessed stood stable at 519,600 t w-o-w.

Factors impacting prices

LME aluminium prices were mainly supported by tightening global supply prospects after confirmation that Mozambique’s Mozal smelter will be placed under care and maintenance by March, a move expected to dent global output next year. Supply concerns were further amplified by disruptions elsewhere, including the suspension of a potline at Iceland’s Grundartangi smelter due to equipment failure.

Inventories at major Japanese ports fell 5.2% m-o-m to 312,100 t, while premiums sought by global producers for January-March shipments to Japan surged, underscoring a tight physical market. However, upside remained capped by renewed demand concerns from China. Although China’s aluminium production rose 2.5% y-o-y to 3.79 mnt in November, ongoing property-sector weakness weighed on sentiment. SHFE-monitored inventories declined 2.5%, providing limited near-term support.

Additionally, global primary aluminium production reached 67.49 mnt in 11MCY’25, up 1.1% y-o-y, although November output declined 3.3% m-o-m to 6.09 mnt.

Outlook

LME aluminium prices are expected to remain firm in the near term, supported by supply-side disruptions, declining inventories, and elevated physical premiums. However, upside may be capped by demand uncertainties in China and seasonally low trading activity. Prices are likely to stay range-bound with a positive bias as markets assess early-2026 supply developments.

Leave a Reply