- Domestic coal demand strengthened amid import rally

- Freight surge pushed global petcoke and coal prices

Coal market sentiment in the week ended 20 February remained firm but cautious. Imported coal prices stayed elevated due to supply disruptions in South Africa and regulatory uncertainty in Indonesia, while freight strength supported overall cost structures. However, buyers largely adopted a wait-and-watch approach as high raw material costs pressured margins. Domestic coal gained attention as a viable alternative, with selective procurement and limited fresh deals dominating market activity.

Indonesian coal prices climb on RKAB delays

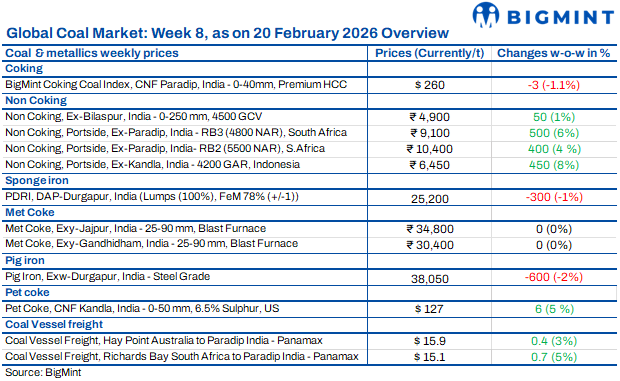

Indian portside prices of Indonesian thermal coal rose w-o-w for the week ended 20 Feb’26 amid continued uncertainty over RKAB (Indonesia’s annual operational and financial plan that mining companies must submit to the government for approval) which constrained export flows. As per BigMint’s assessment, 5,000 GAR increased INR 600/t to INR 8,300/t at Kandla and INR 8,200/t at Vizag. 4,200 GAR rose INR 450/t to INR 6,450/t at Kandla and INR 6,350/t at Vizag, while 3,400 GAR gained INR 250/t to INR 4,850/t at Navlakhi.

Indonesian benchmarks also edged higher, with 5,800 GAR up $1.05/t, 4,200 GAR up $0.54/t and 3,400 GAR up $0.23/t. Coal stocks at Indian power plants stood at 58.8 mnt, around 19 days’ cover, though 23 plants remained under critical levels. Overall sentiment stayed firm on restricted supply.

South African thermal coal prices extend gains

South African thermal coal prices at Indian ports increased further w-o-w amid firm export offers and tight grade-wise availability. As per BigMint’s assessment, exw-Paradip 5,500 NAR rose by INR 350/t to INR 10,350/t, while 4,800 NAR increased by INR 400/t to INR 9,000/t. At Vizag, 5,500 NAR gained INR 200/t to INR 10,100/t and 4,800 NAR rose INR 350/t to INR 8,850/t. Export offers for 5,500 NAR climbed $4-6 w-o-w to around $91/t FOB RBCT amid mine maintenance and operational disruptions in South Africa. No South African stock was reported at Haldia.

Total portside thermal coal inventories across India rose 5.3% w-o-w to 14.06 mnt, the highest since week 31 of CY25. Sponge iron prices in eastern India declined INR 500/t w-o-w to INR 25,000/t, while buyers largely remained cautious despite firm portside sentiment.

Domestic coal prices edge higher in recent SECL auction

Domestic non-coking coal prices increased w-o-w following firmer SECL auction bids and strong imported coal trends. As per BigMint’s assessment, 4,500 GCV rose to INR 4,900/t and 5,000 GCV to INR 5,950/t exw Bilaspur. At the 19 Feb’26 SECL auction, high-grade bids increased INR 150-200/t compared with the previous event. SECL also announced auction of 1,768,000 t of non-coking coal on 26 Feb’26, indicating continued supply in the domestic market.

BigMint coking coal index dips on lower bids

BigMint’s PHCC index was assessed at $260/t CNF Paradip on 21 Feb’26, down $3/t w-o-w amid muted trading during Chinese Lunar holidays. Market sources indicated limited fresh deals, with buyers awaiting clearer direction and FOB expectations from large Indian mills below $220/t. Australian PHCC fell $6/t to $243/t FOB, reflecting subdued global interest.

Indian met coke prices hold steady

Indian BF-grade metallurgical coke prices remained stable w-o-w on 18 Feb’26 despite softer coking coal costs. In eastern India, BF coke stood at INR 34,800/t ex-Jajpur, while western India held at INR 30,400/t ex-Gandhidham. Foundry-grade coke was unchanged at INR 36,100/t ex-Rajkot, reflecting steady demand from steelmakers and foundries. Firm import parity supported prices. Indonesian BF coke offers were heard at $270-275/t CFR India, equivalent to INR 34,000-34,500/t landed.

Global petcoke prices firm up, trades remain limited

Global petcoke prices increased across major origins on rising freight and tight supply, though higher CFR levels triggered buyer resistance in India and Turkiye. FOB USGC 6.5% sulphur rose to $81/t, 5.5% to $84/t and 4.5% to $87/t, while USWC 2% surged to $150/t. Freight to India climbed to $46/t and to Iskenderun to $31/t.

In India, offers were heard at $130-132/t CFR, with buyers targeting $125/t. Venezuelan cargoes were offered at $117/t CFR, while South African coal was booked at $112/t CFR. Turkish offers stood at $115-122/t CIF. Outlook remained firm, though demand resistance may limit further gains.

Coal freight rates stay firm

Dry bulk coal freight rates to India remained firm w-o-w on tight tonnage, higher bunker prices and stronger FFA sentiment, though overall fixture activity stayed limited. Brent crude rose $4.04/bbl to $70.95/bbl, supporting bunker costs. The Baltic Dry Index fell 76 points to 2,019, while the Panamax index increased 50 points to 1,160 and Supramax edged down 5 points to 1,160. DCE coking coal futures held steady at RMB 1,682/t or $243.46/t. Market participants expected freight rates to stay supported as Chinese buyers returned, with momentum likely to build in the coming week.

Leave a Reply