- Landslide disrupts operations at major Indonesian nickel processing hub

- Profit-booking, stable LME stocks, China holiday slowdown cap upside

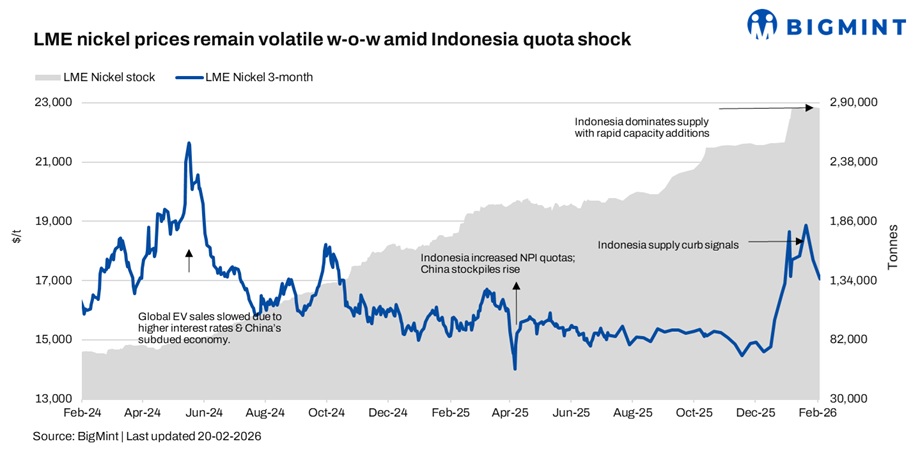

Nickel prices continued to climb up w-o-w, triggered by Indonesia’s aggressive ore quota cuts, though macro pressure and seasonal demand weakness offset supply concerns. LME three-month nickel averaged $17,350/t in the week ended 20 February, up 2% w-o-w from $17,010/t. This was despite a sharp decline of 1.8% d-o-d on 17 February, when prices fell 1.8% d-o-d to $16,830-16,900/t, marking a one-month low.

LME warehouse inventories edged higher to 287,706 t from 287,088 t, remaining broadly stable.

Indonesia tightens ore quotas, reshaping supply outlook

Indonesia’s sharp reduction in nickel ore production quotas (RKAB) has significantly altered short-term nickel sentiment, continuing to drive up prices. Authorities slashed PT Weda Bay Nickel’s 2026 mining allocation to 12 million tonnes (mnt) from 42 mnt previously, while the national ore quota was reduced to 260-270 mnt from 379 mnt in 2025. The move directly challenged the prolonged oversupply narrative that had weighed on prices. Market participants interpreted the cuts as a clear signal of tighter upstream availability for nickel pig iron (NPI) producers and stainless steel mills, prompting a reassessment of forward supply balances and triggering renewed buying interest across the value chain.

Fatal accident halts operations at Morowali nickel hub

Operational risk at Indonesia’s Morowali Industrial Park (IMIP) added to the week’s bullish undertone. A fatal landslide at a PT QMB facility temporarily halted operations, tightening near-term processing availability at one of the world’s key nickel hubs supplying stainless steel and EV battery raw materials. While the disruption is currently localised, market participants viewed it as reinforcing Indonesia’s supply vulnerability, particularly amid already reduced ore quotas.

Traders noted that any prolonged interruption at Morowali could tighten NPI feed flows and strengthen nickel’s underlying support structure in the short term. IMIP, a major global nickel-processing hub supplying stainless steel and EV battery materials, had witnessed a similar accident in March 2025, raising renewed safety concerns.

Macro headwinds trigger correction on 17 Feb’26

Nickel’s decline on 17 February was mainly macro-driven. Strong US non-farm payroll data reduced expectations of an early Federal Reserve rate cut, lifting Treasury yields and strengthening the dollar, which pressured base metals. Profit-booking after the Indonesian supply cut-led rally added downside momentum. Meanwhile, the Lunar New Year-related slowdown in China curtailed stainless steel transactions and NPI procurement. Stable LME inventories further signalled no immediate supply tightness, reinforcing the technical pullback.

Outlook

Macro headwinds and seasonal demand weakness may weigh on nickel prices in the near term, but Indonesia’s ore supply curbs and potential smelter feed constraints should limit downside, keeping the broader market bias cautiously firm.

Leave a Reply