- Vietnam sees weak demand, price resistance

- Pak witnesses limited buying in subdued market

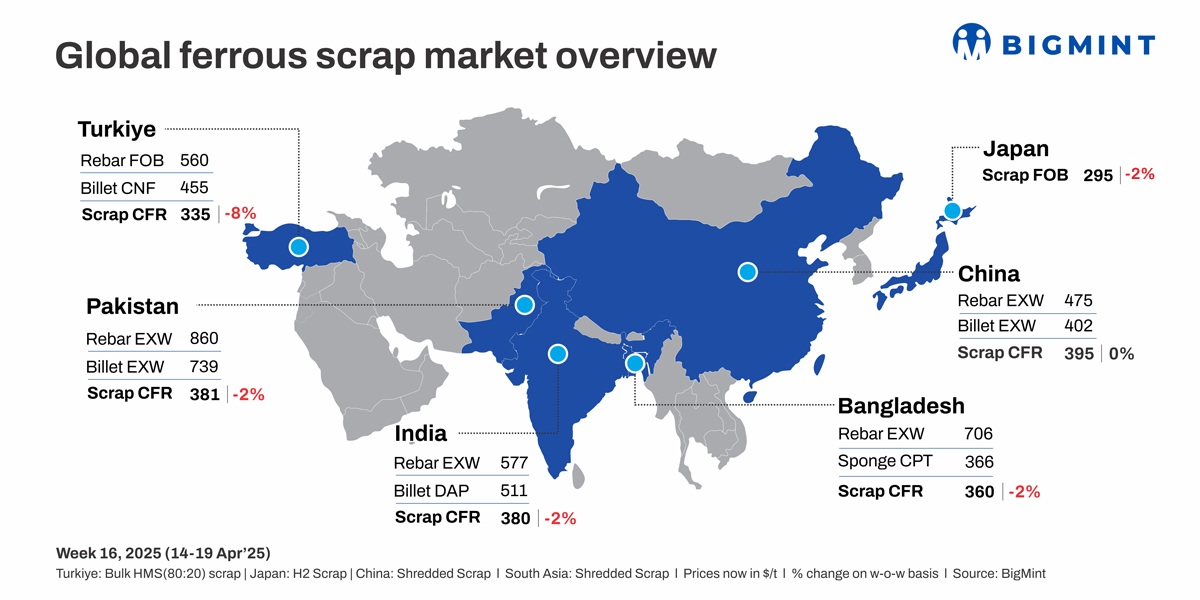

Global ferrous scrap prices fell this week, influenced by weak steel demand, growing competition from cheaper steel alternatives, and concerns over overall economic conditions. Key markets like Turkiye, India, and Bangladesh witnessed reduced buying interest, with mills cautious amid ongoing currency fluctuations, political instability, and uncertainty in steel pricing.

Turkiye: The imported scrap market here remained under pressure due to weak steel demand, political uncertainty, and low-priced Chinese billet offers. HMS 80:20 fell sharply by 5% w-o-w to $345/t CFR, with limited fresh bookings. Mills pushed for lower prices amid sluggish rebar sales, while discounted UK/EU-origin cargoes at $335-348/t CFR dragged the market further down.

US offers at $345-355/t CFR saw little traction, with buyers anticipating further corrections. Domestic scrap prices were also revised down. A late-week Baltic deal at $348/t hinted at a possible floor, but sentiment stayed mixed as high collection costs and a strong euro limited exporter flexibility. Buyers remained cautious, awaiting policy clarity.

Recent deep-sea deals into Turkiye showed an abnormal price drop. HMS 80:20 from the EU sold at $330/t to the Mediterranean region, while US cargo cleared at around $332/t to West Marmara. A German HMS 75:25 cargo was booked at $333/t for the Aegean, reflecting sharply weakened buying sentiment.

India: India’s imported scrap market remained bearish this week, weighed down by weak global cues and volatile domestic steel sentiments. Shredded offers from UK/Europe initially hovered at $390/t CFR Nhava Sheva but saw little interest, with buyers aiming below $380/t. Limited trades and a wide bid-offer gap signalled caution.

Falling domestic rebar prices, rising sponge iron usage, and sufficient inventories kept mills from booking. Australian and UK HMS saw deals in the $350-365/t CFR range, but overall demand stayed sluggish.

Towards the weekend, shredded UK scrap prices fell by 2% w-o-w to $380/t CFR India. The outlook remains cautious amid currency volatility and fears of rising Chinese billet imports.

Around 17,500-18,000 t of imported scrap arrived in India, including a bulk shredded cargo of 10,500 t priced between $380-385/t, a partial bulk HMS 80:20 lot of 2,000 t at $380/t, and a partial bulk bonus-grade cargo of 3,000 t at $395/t. Additionally, 1,500-2,000 t of mixed HMS-LMS bundles, MS turnings, and HMS 80:20 also arrived.

Pakistan: Pakistan’s imported scrap market stayed weak with low steel demand, sluggish rebar sales, and global price drops. Mills ran at 30-40% capacity, avoiding bookings amid tight cash flow and uncertain demand. Sentiment remained weak, with shredded scrap prices falling 2% from $390/t to $381/t.

UK/Europe-origin shredded scrap offers dropped from around $390/t to $380-382/t CFR Qasim, but actual interest remained lower at $375-378/t. Domestic scrap supply remained tight at PKR 138,000-148,000/t ($492-527/t) delivered, while rebar traded at PKR 230,000-250,000/t ($820-890/t) .

Bangladesh: The imported scrap market was subdued as buyers remained largely inactive due to ongoing LC issues and tight forex liquidity, despite stronger remittance inflows and robust March exports.

Bulk offers from the US were absent due to a volatile Turkish market. Offers from Australia and Japan ranged at $360-380/t CFR but drew little interest. Mills preferred domestic scrap, supported by stable rebar prices at BDT 82,000-86,000/t, and avoided imports amid financial uncertainty and political instability.

Japan: The H2 scrap export market remained under pressure this week, with BigMint’s weekly assessment of H2 scrap prices decreasing by JPY 800/t ($6/t) to JPY 42,000/t ($295/t) FOB Tokyo Bay in comparison to JPY 42,800/t ($301/t) last week.

Export activity continued, but at a slower pace, with buyers negotiating for better prices. While Japan found export opportunities, mainly to Southeast Asia and China, market resistance remained high. Buyers focused on securing lower-priced scrap and were holding off on new bookings, waiting for clearer signals in the coming weeks.

Vietnam: Vietnam’s imported scrap market stayed quiet, with limited interest due to competitive domestic scrap rates and weak steel demand. Japanese H2 offers held at $335-340/t CFR, but bids were lower at $322-325/t. US and Australian cargoes saw minimal interest. Domestic H2-equivalent scrap was preferred due to better cost efficiency.

South Korea: The imported scrap market stayed weak as major mills cut purchase prices by KRW 10,000/t ($7/t) amid sluggish rebar demand and rising inventories, which are now touching above 900,000 t. Despite low demand, over 30,000 t of imported scrap, mainly H2 and Shindachi, arrived at ports like Gunsan and Dangjin, adding pressure on domestic suppliers.

The US: Ferrous scrap export indices fell abruptly this week, with HMS 80:20 at $327/t and shredded at $347/t FOB East Coast. Global demand slowed due to cheaper Chinese billet inflows, especially in Turkiye, Bangladesh, and Vietnam. Domestic scrap prices also weakened, led by shredded which dropped by $40/t in some regions, pressured by bearish flat steel trends.

Key buyers saw minimal interest in US cargoes amid currency concerns and weak steel demand. Exporters face margin pressure and limited buying appetite, keeping US obsolete scrap prices under continued downside risk.

Leave a Reply