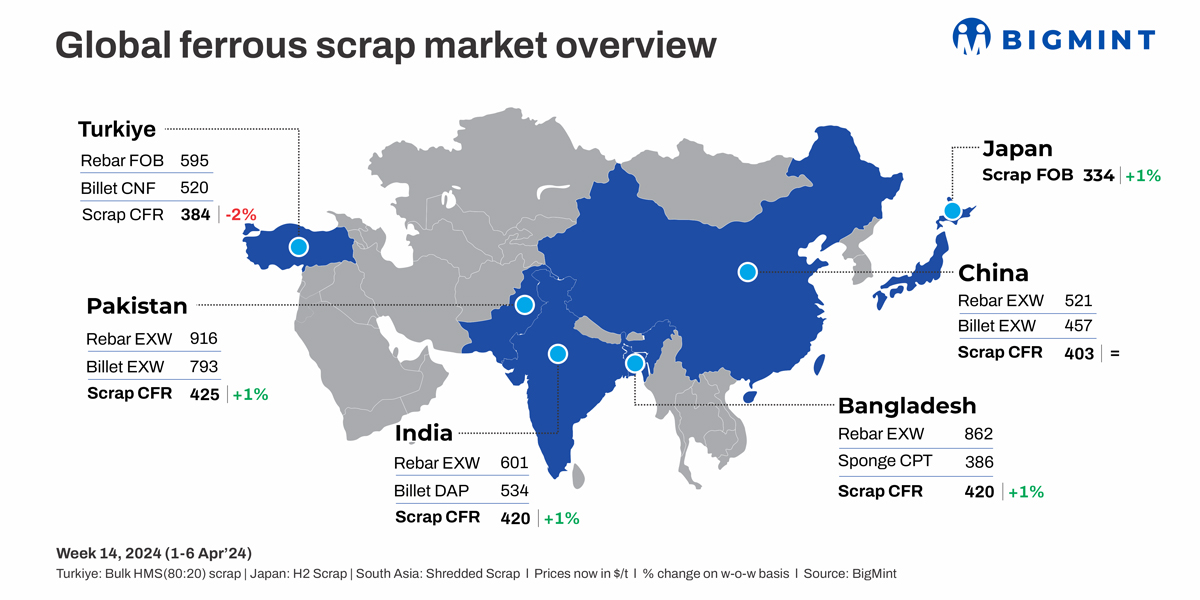

This week, the global ferrous scrap market displayed a mixed trend. In terms of South Asian imported scrap, there was a modest 1% increase, attributed to sellers maintaining a firm stance due to rising collection costs and heightened inquiries from India. However, purchases in the Pakistani and Bangladeshi markets slowed down due to Ramadan festivities and the upcoming Eid holidays.

Japanese H2 scrap export offers saw a $4/t rise compared to the previous week, driven by a positive market outlook and stronger domestic realisation. However, demand from key importers such as Vietnam, Taiwan, and South Korea remained lacklustre, creating downward pressure on the market.

Turkiye: Turkish imported ferrous scrap prices saw a slight decline of $6/t w-o-w due to mills’ efforts to negotiate lower prices. Around 25-27 deep-sea bulk vessels were booked for shipments from Europe, the US, and the Baltic regions, potentially impacting prices if demand surges unexpectedly.

Sellers maintained firm positions despite attempts by Turkish mills to negotiate softer prices. Offers for HMS (80:20) from Europe were at $385-386/t CFR, while those from the US stood at $388-390/t CFR.

BigMint’s assessment for US-origin HMS (80:20) bulk scrap dropped to $384/t CFR. BigMint’s assessment for bulk HMS (80:20) from the US East Coast stood at $361/t FOB, down $5/t w-o-w. BigMint’s weekly rebar assessment stood at $595/t FOB Iskenderun. The scrap-to-rebar spread has increased to $205-206/t as of now.

In the US domestic steel market, a sideways to slightly positive trend is expected in early April, with a resumption of production after maintenance shutdowns potentially stimulating buying activity. European collection costs ranged from Euro 310-320/t delivered to the docks in the Benelux region and Euro 315/t in the Baltic region.

India: In India, demand for imported scrap experienced a modest uptick this week as buyers sought alternatives amidst rising domestic scrap prices and supply shortages. While a few deals were finalised, market observers consider the recent surge in domestic prices to be temporary. Consequently, buyers seeking materials have begun turning to imported scrap.

A Gujarat-based mill reportedly secured a bulk cargo deal comprising 30,000 t this week at approximately $415/t CFR, although specific details are not yet available.

On a weekly basis, shredded scrap offers from Europe increased marginally by $2/t to $418/t CFR, up from $416/t w-o-w. Similarly, HMS (80:20) offers saw a slight uptick to $392/t, a $4/t rise compared to $388/t the week before.

Pakistan: This week, Pakistani buyers displayed little enthusiasm for imported scrap, largely due to the final days of Ramadan festivities and the imminent Eid holidays. Market activity is anticipated to be subdued as participants are expected to be on holiday from 6-12 April. Moreover, some steel mills have chosen to undergo maintenance shutdowns due to the off-season, alongside escalating costs of fuel and electricity, leading to decreased scrap consumption.

On average for the week, shredded scrap offers from Europe were priced at $424/t CFR, marking a $5/t increase compared to the previous week’s $419/t CFR.

Bangladesh: In Bangladesh, the imported ferrous scrap market slowed ahead of the Eid holidays and amid sluggish local steel demand. Containerised shredded scrap from the UK and Europe increased to $420-422/t, while HMS (80:20) offers rose to $403-405/t CFR Chattogram. Approximately 6,500-7,000 t of containerised deals were closed last week.

Bulk inquiries are being floated by the Chattogram mills, particularly for Australian and US suppliers. BigMint’s weekly assessment for US-origin HMS (80:20) bulk scrap increased to $397/t CFR Chattogram. Japanese H2 scrap offers were around $392-394/t, while US-origin HMS (80:20) bulk indicatives ranged from $398-400/t.

Smaller mills in Dhaka face LC clearance issues, impacting liquidity during Ramadan and slowing infrastructure projects.

Japan: This week, export offers for Japan’s H2 scrap increased, propelled by optimistic forecasts for late April and May shipments. Increased interest from Vietnam and Taiwan, expecting further price hikes in line with global trends, also played a role. Additionally, improved realisations in the domestic market contributed to the price hike, prompting some Japanese suppliers to redirect their focus towards domestic sales.

According to the latest assessment by BigMint, export offers for Japanese H2 scrap stood at JPY 50,800/t ($336/t) FOB Tokyo Bay, showing a rise of JPY 600/t ($4/t) compared to JPY 50,200/t ($332/t) FOB reported a week earlier.

South Korea: South Korean steel mills have opted to prioritise domestic market purchases over seaborne options due to the availability of cost-effective scrap in the domestic market. Additionally, scrap inventories were reported to be higher this week.

Vietnam: Vietnamese mills have shifted their focus towards domestic scrap procurement over seaborne scraps due to bid-offer disparities, alongside higher inventories held by major steel mills, which were booked before the Lunar New Year holidays. Meanwhile, downstream steel demand remained soft, resulting in sluggish scrap consumption.

Prices for domestic type 1 (3-6mm) scrap were reported to be around VND 9,000-9,200/t in the northern region and VND 8,700-8,800/t in the southern region.