- Iranian billet exports gradually recover despite challenges

- Chinese exports face limited demand amid weak steel market

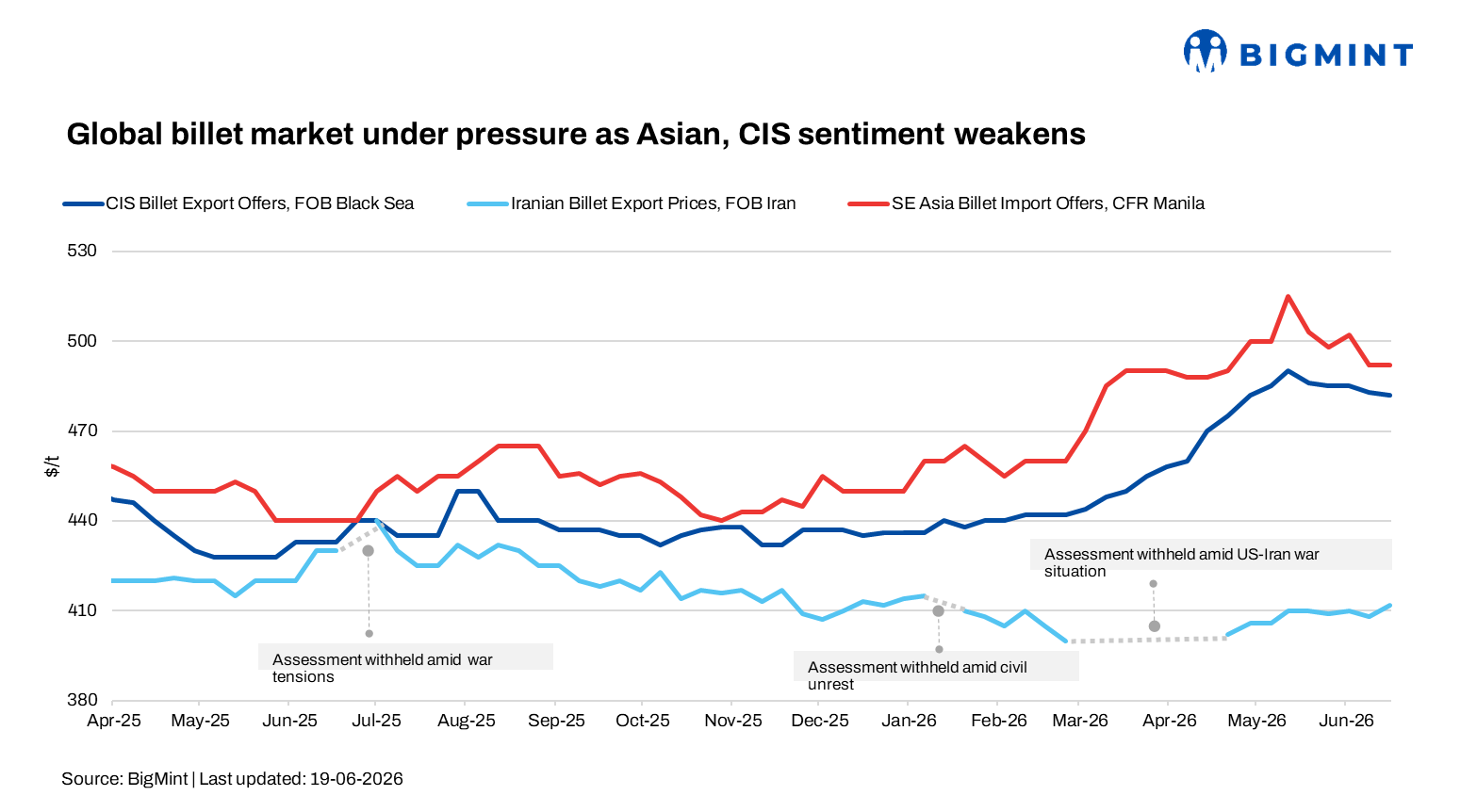

The global billet market remained under pressure during the week ended 19 June as weak finished steel demand and cautious buying sentiment continued to limit trading activity across Asia and the CIS. Chinese and Russian suppliers adjusted export offers to stimulate demand, while buyers largely remained on the sidelines amid falling scrap prices, uncertain steel market fundamentals, and geopolitical concerns.

In contrast, billet demand in the GCC remained relatively firm as buyers diversified supply sources to mitigate logistical risks, supporting import activity from China, Algeria, and Iran despite ongoing uncertainty surrounding regional shipping routes and freight conditions.

Turkish deep-sea scrap sentiment weakened further as CFR Turkiye prices dropped to $385-390/t during the week as sluggish finished steel demand, falling rebar prices, and limited booking activity kept mills largely out of the market. Buyers focused on protecting margins and managing finished steel sales rather than replenishing scrap inventories.

With Turkish rebar export offers slipping below $585/t FOB and domestic rebar trading at $580-600/t exw, the scrap-to-rebar spread remained under pressure, reinforcing bearish sentiment in the imported scrap market.

Asian billet market

Asian billet export activity remained sluggish during the week as buyers delayed purchases amid weak finished steel demand and uncertain market direction. Chinese 3sp billet offers for August shipment were heard at $465-470/t FOB, largely unchanged w-o-w, while trading activity remained limited.

Market participants said traders had secured sufficient volumes in earlier transactions, prompting most buyers to adopt a wait-and-see approach. In Southeast Asia, 5sp billet was offered at $495-500/t CFR, while buyers targeted $485-490/t CFR, resulting in a wide bid-offer gap.

In Indonesia, a major steel mill maintained billet offers at $480-484/t FOB for late-September shipment.

The Philippine market remained weak due to the rainy season and subdued construction activity. Chinese 5sp billet offers were reported at $490-495/t CFR, while Indian billets remained absent from the market. Traders also reported increased short-selling activity amid poor long steel demand.

In Taiwan, Chinese 3sp billet offers were heard at $495-500/t CFR, while recent Russian billet transactions were reported at $490-492/t CFR for volumes of 30,000-60,000 t.

CIS billet market

CIS billet export sentiment softened during the week as Russian suppliers reduced billet offers to $480-485/t FOB Black Sea from $490-495/t FOB a week earlier, pressured by falling Turkish scrap prices and weak buying interest. However, the stronger rouble and firm domestic scrap prices limited the scope for deeper discounts.

Turkish buyers maintained workable billet indications at around $505-510/t CFR, while the gap between buyer expectations and seller targets continued to restrict trading activity. Recent billet price cuts by Kardemir further weakened import demand and reinforced cautious sentiment.

Meanwhile, suppliers from the Donbas region remained largely absent after reportedly selling out of July production. New August offers are expected shortly, with nominal indications heard at $495-500/t FOB.

Black Sea billet sentiment remained weak during the week, with market participants expecting further pressure if Turkish scrap prices continue to soften. Separately, Ukraine’s Kamet Steel is expected to ship around 115,000-120,000 t of billet in June, including more than 110,000 t for export markets.

GCC billet market

Billet demand across the GCC remained firm during the week as buyers continued to diversify supply sources amid ongoing logistical uncertainty in the region.

The UAE remained active in the import market, with a 50,000-52,000 t Chinese billet cargo reportedly booked for August shipment at $535-540/t CFR. Market participants also highlighted persistent port congestion, with a previously booked billet vessel still awaiting discharge at Sohar.

Algerian billet attracted growing interest as an alternative supply source, although transaction-related challenges limited direct trade with UAE buyers. Some cargoes were reportedly redirected to other GCC destinations.

Qatar remained one of the most active markets, with buyers evaluating billet from Oman, Saudi Arabia, China, and Algeria. Import billet prices were assessed at $550-560/t CFR Qatar.

In Saudi Arabia, billet transactions involving Algerian material were reported, while a 50,000-t Chinese slab cargo was reportedly booked at around $560/t CFR.

Despite active buying interest, market participants remained cautious amid uncertainty surrounding the Strait of Hormuz, with many delaying major purchasing decisions until freight and logistics conditions become clearer.

The failure to fully reopen the Strait of Hormuz has continued to disrupt regional steel supply chains, forcing GCC mills to maintain contingency plans for raw material procurement. Market participants noted that billet, slab, scrap, iron ore, and pellet supplies remain key concerns, while port congestion and freight uncertainties continue to affect purchasing decisions.

Meanwhile, Iranian billet export sentiment improved slightly as mills gradually resumed export activity and adopted more flexible pricing. Billet offers were heard at $410-415/t FOB, while producers, including Khouzestan Steel Company (KSC), IASCO, and SJSCO, returned to the market with fresh tenders. Billet shipments to Oman and the UAE were also reported.

Improved port operations and better freight availability supported export enquiries and allowed mills to gradually resume overseas sales. However, renewed regional tensions and uncertainty surrounding US-Iran negotiations later weakened sentiment, prompting buyers to remain cautious.

However, buyers continued to monitor regional tensions and freight conditions closely, while electricity restrictions and summer power shortages continued to weigh on Iranian steel production. Domestic billet and rebar prices remained largely stable amid weak demand and liquidity constraints.

Leave a Reply