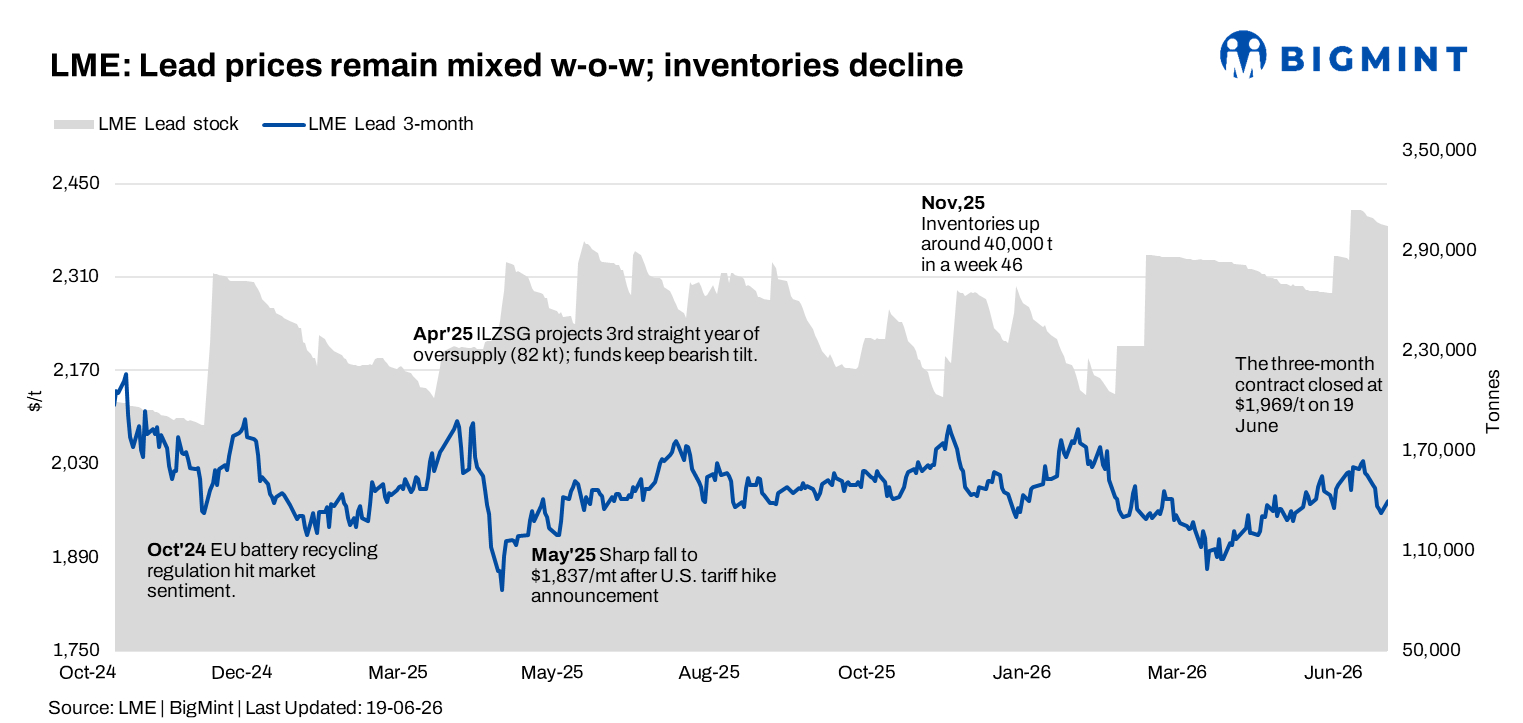

- Prices remain below key $2,000/t level

- Chinese market shows signs of resilience

Lead prices on the London Metal Exchange (LME) remained under pressure during the week ended 19 June 2026, extending losses for a second consecutive week as bearish sentiment across the base metals complex continued to weigh on market activity. Despite ongoing declines in exchange inventories, prices struggled to gain traction and remained below the psychological $2,000/t threshold.

On a w-o-w basis, LME cash lead prices declined by $22/t, or 1.1%, to $1,935/t on 19 June from $1,957/t recorded on 12 June. The persistent weakness reflects cautious industrial demand and continued risk aversion among market participants, although tightening inventories helped limit sharper downside moves.

Price trends

LME cash lead prices opened the week at $1,964/t on 15 June before gradually weakening through the reporting period. Prices slipped to $1,956/t on 16 June and further to $1,945/t on both 17 and 18 June before touching a weekly low of $1,935/t on 19 June.

The three-month contract followed a slightly different trajectory. Prices strengthened from $1,974/t on 15 June to a weekly high of $1,980.5/t on 17 June before easing to $1,969/t by the close of the week. The divergence between cash and forward prices suggests near-term spot market weakness, while forward sentiment remained relatively more stable.

The continued inability to reclaim the $2,000/t level indicates weak near-term momentum, with sellers maintaining control despite tightening inventory conditions.

Inventory analysis

LME lead inventories continued their downward trend during the reporting week, providing some underlying support to the market.

Stocks declined from 305,875 t on 12 June to 304,850 t on 15 June and continued to fall steadily throughout the week, reaching 301,950 t on 19 June.

Overall, exchange inventories declined by 3,925 t w-o-w, extending the inventory drawdown observed in recent weeks. The sustained reduction suggests ongoing warehouse outflows and relatively balanced physical supply conditions. However, inventory declines alone have not been sufficient to reverse prevailing bearish market sentiment.

SHFE lead trends

On the Shanghai Futures Exchange (SHFE), lead prices displayed a firmer tone during the week.

SHFE lead remained stable at $2,246/t on both 15 and 16 June before advancing to $2,263/t on 17 June, $2,281/t on 18 June and $2,300/t on 19 June.

The steady rise suggests improving sentiment in the Chinese market, supported by relatively stable domestic demand conditions. Trading activity, however, was expected to remain subdued towards the week-end as market participants prepared for the Dragon Boat Festival holiday period from 19-21 June.

MCX lead trends (15-19 June)

On the Multi Commodity Exchange (MCX), lead futures traded within a narrow range and broadly mirrored weakness in overseas markets.

The June contract settled at INR 204.8/kg on 15 June and remained largely rangebound during the week. Prices edged lower to INR 204.7/kg on 16 June, recovered marginally to INR 205.1/kg on 17 June, and subsequently declined to INR 203.9/kg on 18 June before closing at INR 203.8/kg on 19 June.

Open interest declined from 435 lots on 15 June to 395 lots on 19 June after touching 451 lots during the middle of the week. The simultaneous decline in prices and open interest indicates long liquidation, reflecting cautious participation and a lack of fresh bullish positions.

Trading volumes remained moderate as domestic consumers largely continued need-based procurement amid stable availability of refined lead material.

Market updates

Market sentiment remained cautious throughout the week as lead prices continued to trade below the key $2,000/t mark despite persistent inventory drawdowns. The decline in LME stocks provided some support to market fundamentals; however, weak spot market performance and limited speculative interest kept overall sentiment subdued.

In India, buyers largely maintained need-based purchases, with adequate material availability limiting aggressive restocking activity. Market participants reported stable demand from battery manufacturers, though elevated uncertainty regarding near-term price direction encouraged consumers to remain cautious. Meanwhile, firmer SHFE lead prices offered some positive signals from China, although trading activity was expected to slow ahead of the Dragon Boat Festival holiday period.

Outlook

BigMint expects LME lead prices to remain under pressure in the near term as weak spot market sentiment continues to outweigh support from declining exchange inventories.

The market is likely to find immediate support in the $1,920-1,940/t range, while resistance is seen around $1,980-2,000/t. Inventory movements and post-holiday demand trends in China will remain key indicators for future price direction, while domestic buyers are expected to continue adopting a cautious, need-based procurement strategy.

Leave a Reply