- Weak global scrap, finished markets weigh on billet prices

- Iraq import duty to curb Iraq’s billet export prospects

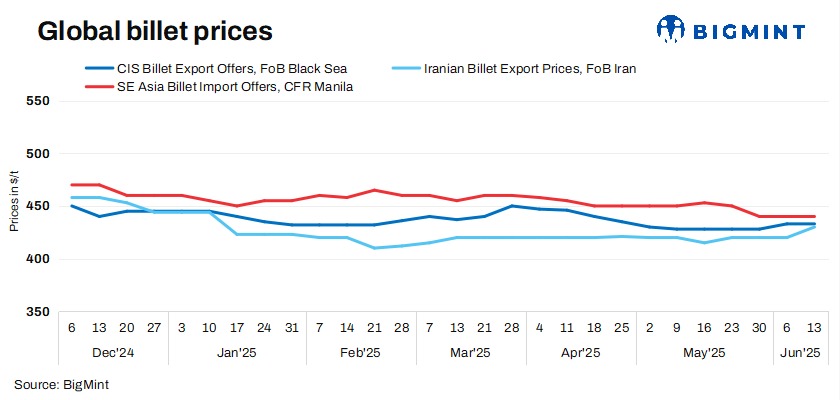

In the 24th week of CY2025, the global billets market displayed diverging regional dynamics, reflecting a complex interplay of supply, demand, and sentiment shifts, according to BigMint. From the absence of export offers in Vietnam to stable billet import prices in Southeast Asia despite limited trading activity, and from weak market sentiment in China driven by falling domestic raw material prices to Iranian steelmakers securing billet export deals at higher levels amid supply concerns – the global billet market captured it all.

Meanwhile, weakness in the global ferrous scrap and finished long steel markets also exerted some downward pressure on the billets market. According to BigMint, imported deep-sea ferrous scrap (HMS 80:20) prices in Türkiye fell by approximately $4/t w-o-w, as Turkish mills remained cautious and refrained from significant bookings amid sluggish demand for finished steel products.

Similarly, the finished steel market in the region has experienced sluggish activity in recent weeks, influenced by the Eid holidays, the typical seasonal summer slowdown, and domestic economic challenges such as high inflation and rising interest rates. Reflecting this, Turkiye’s rebar export prices also declined by around $5/t w-o-w, according to data from BigMint.

Market highlights

- SE Asia’s imported billet prices stable amid holiday lull: Imported billet prices in Southeast Asia remained steady despite limited spot market activity during the holiday period. Buyers and sellers largely took a cautious, wait-and-see stance amid uncertainty over price sustainability and future demand. According to BigMint, weekly billet import prices held firm at $440 per tonne CFR Manila, w-o-w, on 13 June 2025.

- Vietnam billet export offers remain on hold: In Vietnam, the persistent lack of new export offers highlights a cautious market atmosphere, as sellers hold back from aggressive pricing amid regional material shortages. Market participants are prioritizing their domestic demand and increasingly turning to imports to meet requirements. Additionally, subdued buying interest and cautious sentiment in the scrap market have further weighed on the billet market.

- Iran billet export tenders attract higher bids amid supply concerns: Iranian billet producers are pushing for higher deal prices amid limited availability caused by power supply challenges. Khouzestan Steel Complex (KSC), a leading Iranian steelmaker, recently secured an export contract for 30,000 t of billets. The deal was finalized at $430/t FOB, with shipments scheduled for late September 2025, according to sources cited by BigMint.

In a recent announcement, the Iraqi government has raised the import duty on Iranian rebar from 20% to 30% across all sources. This move aims to support domestic steel producers and curb the competitive advantage of Iranian steelmakers in the Iraqi market.

- Chinese billet prices inch down by RMB 10/t ($1/t) w-o-w: Steel billet prices in Tangshan, China, edged down by RMB 10/t ($1/t) w-o-w to RMB 2,900/t ($404/t), including 13% VAT, on 13 June 2025. Billet prices recorded a dip due to reduced production in the downstream sector , weakening domestic raw material tags and fall in rebar futures. Meanwhile, SHFE rebar futures (October 2025 delivery) dipped w-o-w by RMB 6/t ($1/t) to RMB 2,969/t ($414/t) on 13 June 2025.

Leave a Reply