- Chinese billet rebounds post-CNY holiday

- Turkiye billet trade weak amid Ramadan, liquidity crunch

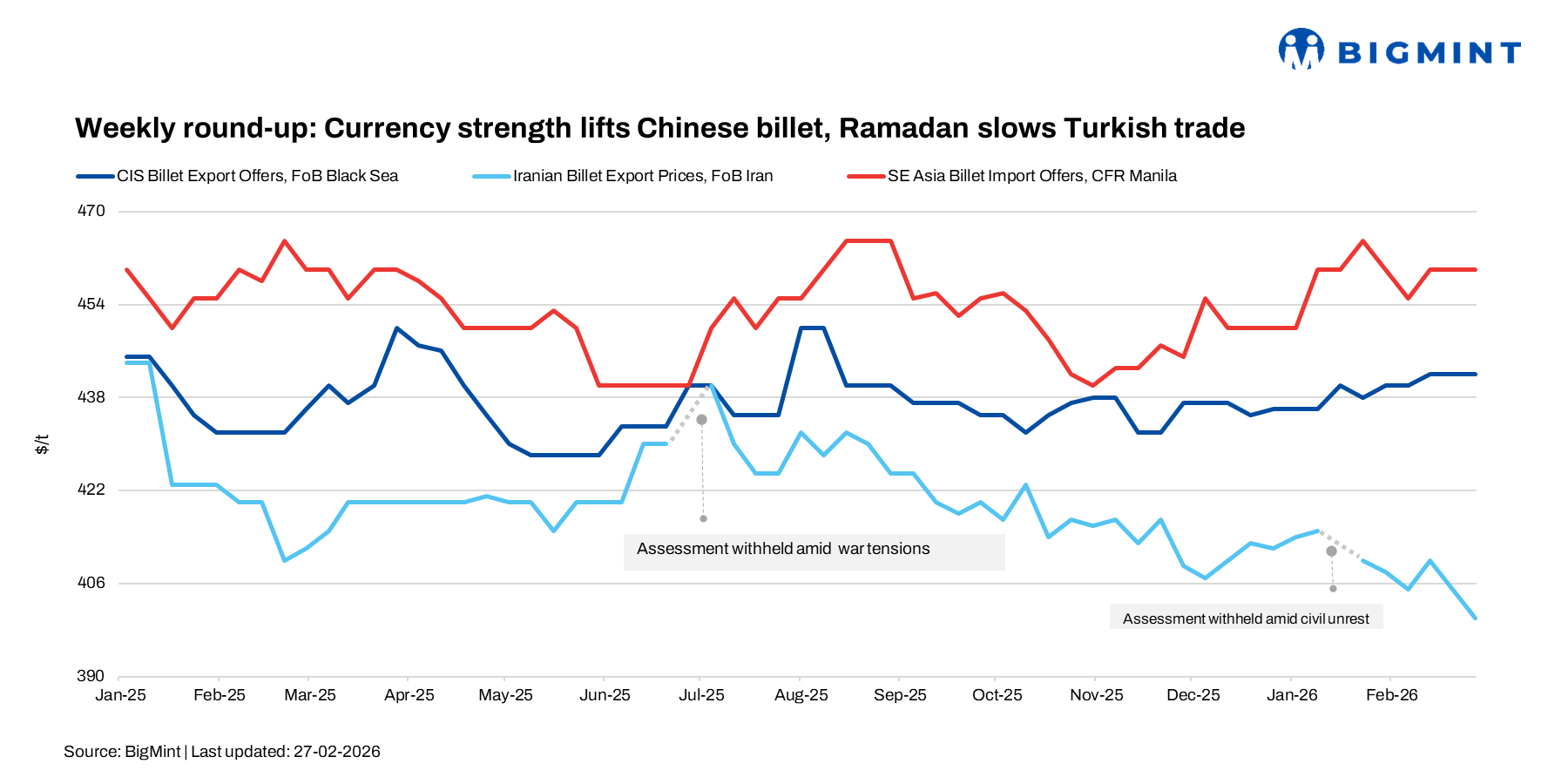

Global billet prices were largely stable to slightly firmer w-o-w. Chinese export offers rebounded after the CNY lull, supported by a stronger RMB and improved post-holiday sentiment, while Southeast Asian import levels held steady. CIS-origin billet into Turkiye remained broadly unchanged, and Iranian billet stayed stable sub-$400/t FOB. However, tight liquidity and cautious downstream demand continued to limit aggressive buying across key import markets.

In Turkiye, deep-sea scrap prices were steady, with US-origin HMS 80:20 at $374-376/t CFR and EU/Baltic at $369-373/t CFR. Weak rebar demand and narrow scrap-to-rebar spreads of $180/t kept mills cautious, with rebar export offers around $555/t FOB. Ramadan, US winter collection constraints, and firm freight rates underpinned scrap offers, but resistance to US levels near $380/t CFR restricted fresh deal activity.

China/Southeast Asia

Chinese export billet prices, which had eased by $4-5/t over the past month to an average of $438-440/t FOB, rebounded mid-week as Asian buyers returned from holidays and sentiment improved. New Offers for 3sp billet were heard at $443-446/t FOB for April shipment, up from $438-440/t two weeks earlier, while bids remained lower at $430-435/t FOB.

“Last two days, traders booked good volumes with mills and took positions. Now mills are not in a hurry as they have sufficient May order books,” a major Southeast Asian trader said.

The rebound was supported by a stronger RMB, which appreciated to 6.85 against the US dollar from 6.91 before the holidays.

“Export prices are not competitive with the current exchange rate, because the RMB appreciated too much,” a Singapore-based trader commented.

Sentiment was further supported by expectations of fresh government stimulus ahead of upcoming parliamentary meetings and anticipated output curbs in North China during 4-11 March. Tangshan billet prices rose RMB 30/t ($4.3/t) mid-week on urban renewal stimulus hopes. Chinese rebar futures dipped early in the week but stabilised later.

In Southeast Asia, imported billet prices remained broadly stable at $460-465/t CFR over the past month. Buying improved slightly mid-week, but overall demand stayed selective. Seasonal construction recovery in March-April may lend support; however, tight financing conditions and cautious long steel consumption continue to cap procurement.

Indonesian Dexin Steel maintained base-grade billet offers at $450-455/t FOB, while open-origin 5sp billet was indicated at around $4650470/t CFR Southeast Asia, up from $460-465/t earlier. “There are no firm offers in the market. Everyone is waiting for the exchange rate to stabilise,” an exporter noted.

CIS/Turkiye

In the import segment, CIS-origin billet was offered at $465-470/t CFR, with workable levels seen near $460/t CFR as buyers resisted higher prices. Chinese billet was indicated at around $475/t CFR. Over the past month, imported billet prices remained broadly stable at $460-465/t CFR, while domestic prices softened marginally.

Business activity in Turkiye’s billet market remained weak during the week, constrained by Ramadan and tight liquidity. Domestic square billet offers were heard at $490-500/t exw, slightly down from $495-500/t previously, while bids for smaller lots were around $490-495/t exw. Mills facing slow finished steel sales and cash flow shortages are increasingly open to selective price adjustments to secure bookings.

While some seasonal improvement in rebar demand is expected after Ramadan, high borrowing costs and weak export outlets are likely to keep billet trading cautious. In the near term, price direction will depend largely on import competitiveness and mills’ urgency to generate cash flow rather than on any meaningful recovery in underlying steel demand.

Iran

Iran’s semis export trade remains under pressure amid Ramadan-related slowdown and heightened political uncertainty. Export activity has largely paused, with billet prices holding stable at $390-400/t FOB. While most quoted levels are from traders, mills are reportedly targeting higher offers.

“We prefer to buy from trading companies because customers are looking for smaller cargoes,” a Middle East steel market participant noted.

Market sentiment remains cautious as geopolitical developments continue to influence business decisions. Participants are closely monitoring the outcome of negotiations in Geneva between Iran and the US, as progress could support trade flows, while adverse developments may further disrupt activity. Some market players anticipate a gradual pickup in transactions as Chinese buyers re-enter the market, particularly in the raw materials segment.

Despite firmer domestic semis prices on higher DRI costs and gas constraints, export offers remained broadly stable as currency gains offset the rise in local prices.

Outlook

BigMint believes global billet prices are expected to remain largely rangebound, with mild upward support from a stronger RMB, a seasonal construction recovery in Asia, and stable scrap costs. However, tight liquidity, cautious procurement, and weak finished steel demand in Turkiye and parts of Asia will limit significant price gains.

Leave a Reply