- Year-end restocking lifts billet enquiries in Saudi Arabia

- Higher futures push up China’s export offers, demand lags

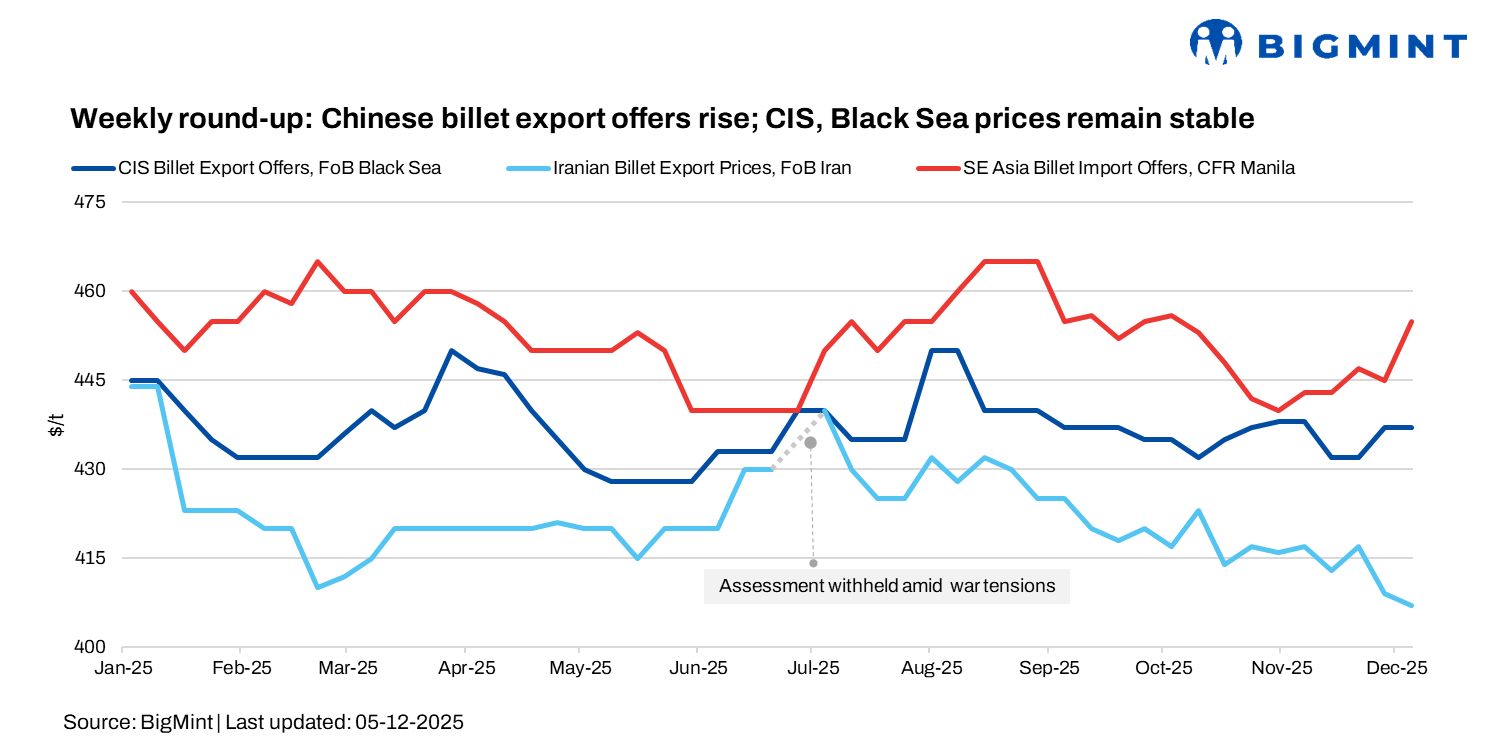

Global billet and scrap markets strengthened in the week ended 5 December, supported by firmer rebar sentiment in Turkiye, tightening supply, and steady buying interest across Asia and the GCC. While Chinese billet export offers climbed up, CIS and Black Sea prices remained stable.

Billet prices from Chinese and Indonesian exporters held at $440/t FOB minimum, translating to $450-455/t CFR for buyers in the Philippines and Thailand. Chinese traders who built positions around $430/t FOB (Dexin) are now holding stocks, awaiting further upside with SHFE support.

In Turkiye, deep-sea scrap prices rose on higher collection costs and limited availability. EU HMS 80:20 was assessed at $356-365/t CFR, while US-origin material traded at $368-372/t CFR. Around 6-7 deals were concluded at $352-368/t CFR, with the scrap-to-rebar spread steady at $200-205/t. Sentiment remained firm but cautious.

Asian billet market

Chinese billet export offers edged up in early December on firmer local sentiment and supportive futures, but higher prices failed to spur buying interest. Mills raised January-February offers to $440-445/t FOB (from $435-438/t), while Dexin held at $440/t FOB for March after selling around 100,000 t at $432/t FOB last week. The uptick was seen as being futures-driven, with traders stating that current levels are too high to follow.

Domestic billet prices in China edged up by RMB 20/t ($3/t) w-o-w to RMB 3,000/t ($424/t) in the week ended 5 December. The uptick was supported by steel output hitting an eight-month low and falling mill inventories, though gains were capped by soft raw material prices, high port stocks, and muted restocking interest.

SHFE rebar futures dipped by RMB 3/t ($1/t) w-o-w to RMB 3,107/t ($439/t). Demand remained subdued, and export activity was quiet but firm, keeping sentiment cautious as the market moved deeper into the seasonally weak December period.

In Southeast Asia, Chinese 3sp was available at $460-464/t CFR Thailand, against bids at $442-445/t, prompting many exporters to withdraw offers. Taiwan buyers capped bids near $430/t CFR, Indonesian import activity stayed muted, and the Philippines saw no fresh deals after a recent 20,000-t booking at $454-458/t CFR. Despite Indonesia’s tighter scrap supply (licence suspensions lifting scrap costs), billet market sentiment remained cautious, with seasonal demand weakness and long lead times keeping buyers sidelined.

Latest offers for Asian billets

- China (3sp): $440-445/t FOB

- Indonesia (3sp): $440/t FOB

- China to Indonesia (3sp): $450-455/t CFR

- China to Philippines (5sp, 150 mm): $450-455/t CFR

CIS market

CIS billet offers remained unchanged this week amid quiet trade, with Russian suppliers quoting $440-450/t FOB Black Sea for January-February shipments, depending on payment terms. Semis from unrecognised Donbas republics were heard at $440/t FOB Novorossiysk, up from $430/t FOB a couple of weeks ago. In Turkiye, CIS billets stayed at $455-460/t CFR (equivalent to $438-442/t FOB), levels viewed as workable, especially for Black Sea and Marmara buyers.

Turkish market

CIS-origin billets remained stable at $455-460/t CFR, with unconfirmed chatter of two to three cargoes sold at these levels. Chinese billets held steady at $470/t CFR Turkiye, and Indonesian and Malaysian material were available at $475-480/t CFR and $490/t CFR, respectively, though long delivery timelines (February-March arrival) reduced buying interest.

Turkish local billet offers inched up to $530-540/t exw by the week’s end (vs $520-530/t exw at the start), driven by higher scrap costs and firmer rebar prices. Price strength was mainly supply-led, as mills operated at around 50% of their capacity, keeping tonnage tight. Demand remained weak, and no major deals were heard.

Marmara-based producers quoted higher than Iskenderun, supported by rebar at $590/t exw in Marmara versus $570-575/t exw in Iskenderun.

Saudi Arabian market

Saudi mills stepped up enquiries to replenish stocks ahead of year-end, lending firmer support to billet prices and intensifying negotiations. A regular consumer was in the market for around 50,000 t of billet. Chinese offers at $470/t CFR Saudi Arabia were slightly above buyers’ expectations, as recent bookings were done at $450-460/t CFR.

Locally, billet prices stood at SAR 1,800-1,820/t exw ($480-485/t), up SAR 10-15/t ($3-4/t). Improved finished steel sentiment also lifted scrap prices by SAR 15-20/t ($4-5/t), with material from Jeddah and Riyadh assessed at SAR 1,400-1,410/t ($373-376/t).

Scrap stood at SAR 1,400/t ($373/t) in Jeddah and Riyadh, SAR 1,370/t ($365/t) in Dammam, and SAR 1,250/t ($333/t) in Jizan.

Sentiment remained firm — restocking activity and higher input costs underpinned prices, though buyers remained selective due to pricing.

Leave a Reply