- Freight costs and logistics disruptions support prices

- Weak rebar demand limits billet buying interest

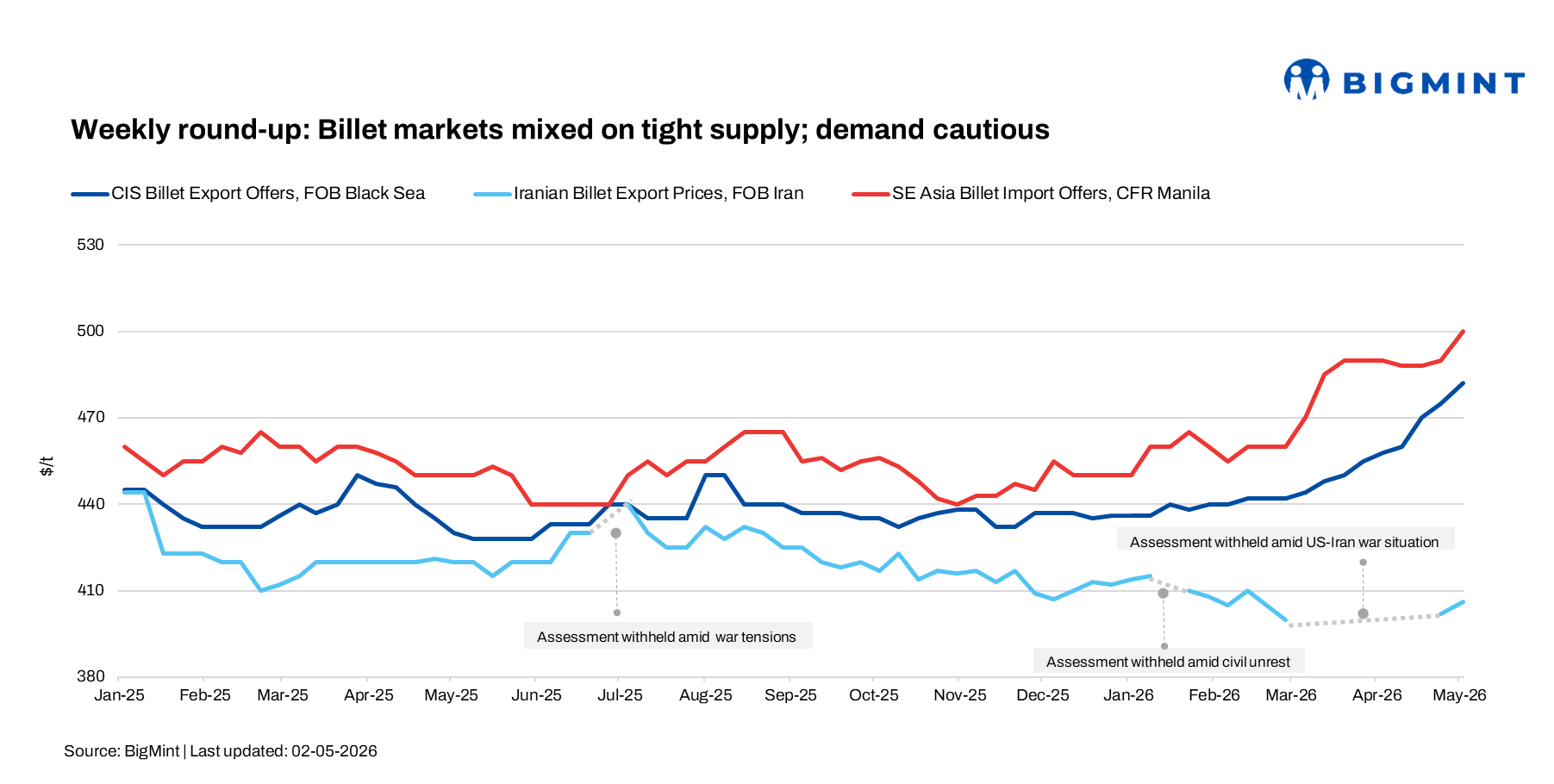

Global billet markets witnessed mixed movements during the week, with gains led by the CIS/Black Sea region on the back of firmer currencies and stronger seller control.

China provided additional support through higher domestic billet prices and marginal gains in rebar futures towards the later part Chinese market remain absent due to holidays.

In contrast, Southeast Asia remained subdued as buyers largely stayed covered and resisted elevated offers. Reduced exports from Iran and ongoing logistical disruptions tightened supply, supporting prices but limiting aggressive trade activity.

In Turkiye, scrap prices remained largely stable, supported by tight supply from the US and Europe along with firm freight rates. However, billet sentiment stayed cautious, with weak downstream demand—particularly in rebar—continuing to weigh on buying interest. Mills showed limited urgency for fresh bookings, focusing on existing coverage and monitoring market direction.

CIS/Black Sea billet market

Billet prices in the CIS/Black Sea region strengthened w-o-w, supported by improved deal activity and firmer seller sentiment. Export billet was assessed around $480-485/t FOB, with tradable levels at $478-480/t, while offers ranged from $480-500/t FOB and up to $500-530/t CFR Turkiye.

However, higher offers remained largely unworkable amid buyer resistance. Turkish import billet prices were heard at $505-510/t CFR, reflecting increased replacement costs, though limited deal closures indicated cautious buying.

In Turkiye’s domestic market, billet and rebar segments remained under pressure due to weak downstream demand. Mills reduced rebar prices to $600-615/t exw to stimulate sales, with some volumes concluded at discounted levels. Softer finished steel prices, despite relatively firm scrap costs, continued to compress margins and limit billet procurement. Export rebar offers also eased to similar levels, reflecting subdued global demand.

Meanwhile, Russia’s scrap market stabilised following earlier corrections. A3-grade scrap was heard at RUB 15,300-18,500/t ($204-247/t) in the Central Federal District and RUB 14,300-18,200/t ($191-243/t) in the northwest, while the Urals region ranged at RUB 17,800-19,100/t ($238-255/t). Mills paused price revisions ahead of holidays, focusing on stable inflows and inventory rebuilding.

Asian billet market

Asian billet markets showed divergent trends, with Chinese suppliers raising export offers. 3SP billet prices increased to $475-480/t FOB for July shipment, supported by firm domestic demand, improved bookings, and the absence of Iranian material. Strong local steel prices and seasonal demand kept sentiment supported.

In contrast, Indonesian steel major maintained offers at around $485/t FOB, unchanged w-o-w after concluding similar deals. Volumes of 40,000-50,000 t were largely for stock-building, with cargoes moving toward the Middle East.

However, fresh buying interest slowed as earlier requirements were largely covered, with the producer shifting partial focus toward slab sales.

Across Southeast Asia, activity remained limited. A China-origin billet deal was heard slightly above $490/t CFR Thailand, while offers to the Philippines crossed $500/t CFR. However, demand remained weak due to high prices, rising construction costs, and seasonal factors, keeping overall sentiment cautious.

GCC market

Billet supply in the GCC remained tight during the week, as disruptions in the Strait of Hormuz continued to impact regional trade.

Limited vessel availability, longer transit times, and elevated freight costs increased procurement expenses, though buyers adapted by exploring alternative logistics routes.

Oman emerged as a key transshipment hub, with cargoes redirected to the UAE and other GCC markets to maintain supply flow.

Deals were heard at around $485/t FOB for 30,000-50,000 t cargoes for July shipment, translating to $525-535/t CPT UAE, up $5-10/t from mid-April due to higher logistics costs.

In Saudi Arabia, mills sourced material from Russia and China at $520-522/t CFR, prioritising supply security despite rising costs.

Iran market

Iran’s semis market remained under pressure amid ongoing geopolitical and logistical disruptions. Billet export activity showed gradual recovery, with offers at $400-410/t FOB for May shipment. Several producers floated tenders of around 20,000 t, indicating attempts to re-enter export markets. However, trade activity remained limited due to sanctions, shipping constraints, and restricted access to key routes.

Smaller transactions included Iranian-origin billet at around $405/t FOB Bandar Abbas.

It is critical to note that Iran has suspended exports of steel billets and other semi-finished products until May 30, 2026, following recent regional conflicts and damage to infrastructure.

At the same time, slab exports remained constrained following disruptions at major steel plants, increasing reliance on imports. This led to higher inquiries for flat products, with Chinese semis offers around $500/t FOB, while buyers targeted similar levels on a CFR basis. Discussions with CIS suppliers, including Russia and Kazakhstan, were also noted, though trade mechanisms remained unclear.

Outlook

Global billet markets are expected to remain supported in the upcoming days, driven by firm input costs, currency strength, and constrained supply, particularly from the Black Sea and Iran.

However, weak downstream demand–especially in rebar–is likely to limit further upside. Buyers are expected to remain cautious, focusing on short-term requirements.

At the same time, shifting trade flows across Asia and the Middle East, along with ongoing logistical challenges, will continue to shape market dynamics. Price movements are likely to remain gradual, with regional variations driven by supply constraints, freight conditions, and evolving demand trends.

Leave a Reply