- Higher mill consumption led by Asia narrows global stock outlook

- India’s stable output contrasts with rising demand from spinning millers

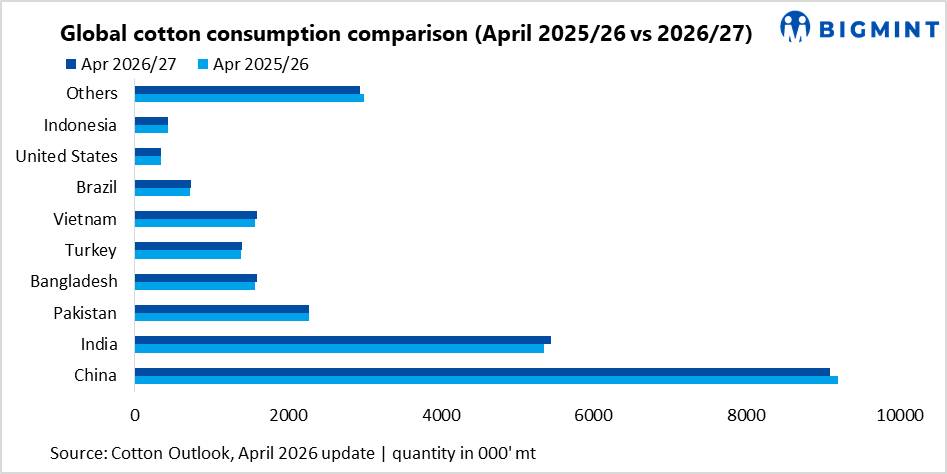

Global cotton balance shifts towards deficit

Global cotton fundamentals for the 2026-27 season indicate a tightening balance sheet, with consumption expected to outpace production, leading to a drawdown in ending stocks. According to the Cotton Outlook April update, world cotton production is projected at 25.37 million tonnes (mnt), revised upward by 264,000 t primarily due to higher crop estimates in China and Pakistan. However, global consumption has been raised more sharply by 487,000 t to 25.89 mnt, reflecting improved demand from key textile manufacturing hubs including China, Pakistan, and Turkiye.

As a result, global stocks are forecast to decline by 518,000 t by the end of the 2026-27 marketing year, indicating a shift from surplus conditions towards a tighter supply-demand scenario.

India’s position remains steady amid global adjustments

India’s cotton production estimate for 2026-27 remains unchanged at 5.31 mnt, signalling stable crop prospects despite global revisions. On the consumption side, domestic demand is also steady at 5.44 mnt, suggesting that India’s spinning millers continue to operate at consistent capacity levels without significant expansion or contraction.

For the ongoing 2025-26 season, India’s production estimate has been marginally revised upward by 85,000 t to 5.355 mnt, contributing to a modest increase in global supply. This reinforces India’s role as a stable producer in the global cotton balance, even as other origins witness more volatility.

Current season shows narrowing surplus

In the 2025-26 season, global cotton supply has been revised upward by 110,000 t due to higher production in India and Brazil. At the same time, consumption has increased significantly by 532,000 t, driven by improved mill demand across major consuming countries.

This has reduced the expected global stock build-up to 578,000 t, down from an earlier estimate of 1 mnt. The narrowing surplus indicates that demand recovery is absorbing additional supply more efficiently than previously anticipated.

Demand recovery led by Asian spinning hubs

The upward revision in global consumption is largely driven by Asia’s textile sector. China’s consumption has been increased by 250,000 t for 2026-27, while Pakistan and Turkiye have also seen upward revisions of 107,000 t and 100,000 t respectively. These changes reflect improving yarn demand, better export orders, and stabilising textile margins.

For India, while consumption remains unchanged, steady demand from spinning millers indicates resilience in domestic yarn markets despite global uncertainties.

Implications for trade and prices

The projected stock drawdown in 2026-27 is likely to provide underlying support to global cotton prices, particularly if demand momentum sustains. For Indian stakeholders, including ginners, spinning millers, and exporters, the stable domestic balance combined with tightening global stocks may improve export competitiveness, especially if international prices firm up.

However, the absence of strong growth in India’s consumption suggests that any significant upside in prices will depend more on global demand trends than domestic fundamentals. Going forward, trade flows, currency movements, and China’s procurement strategy will remain critical factors shaping price direction and export opportunities.

Leave a Reply