- Middle East supply tightness drives sharp price gains

- Asia shifts sourcing amid limited Russian supply

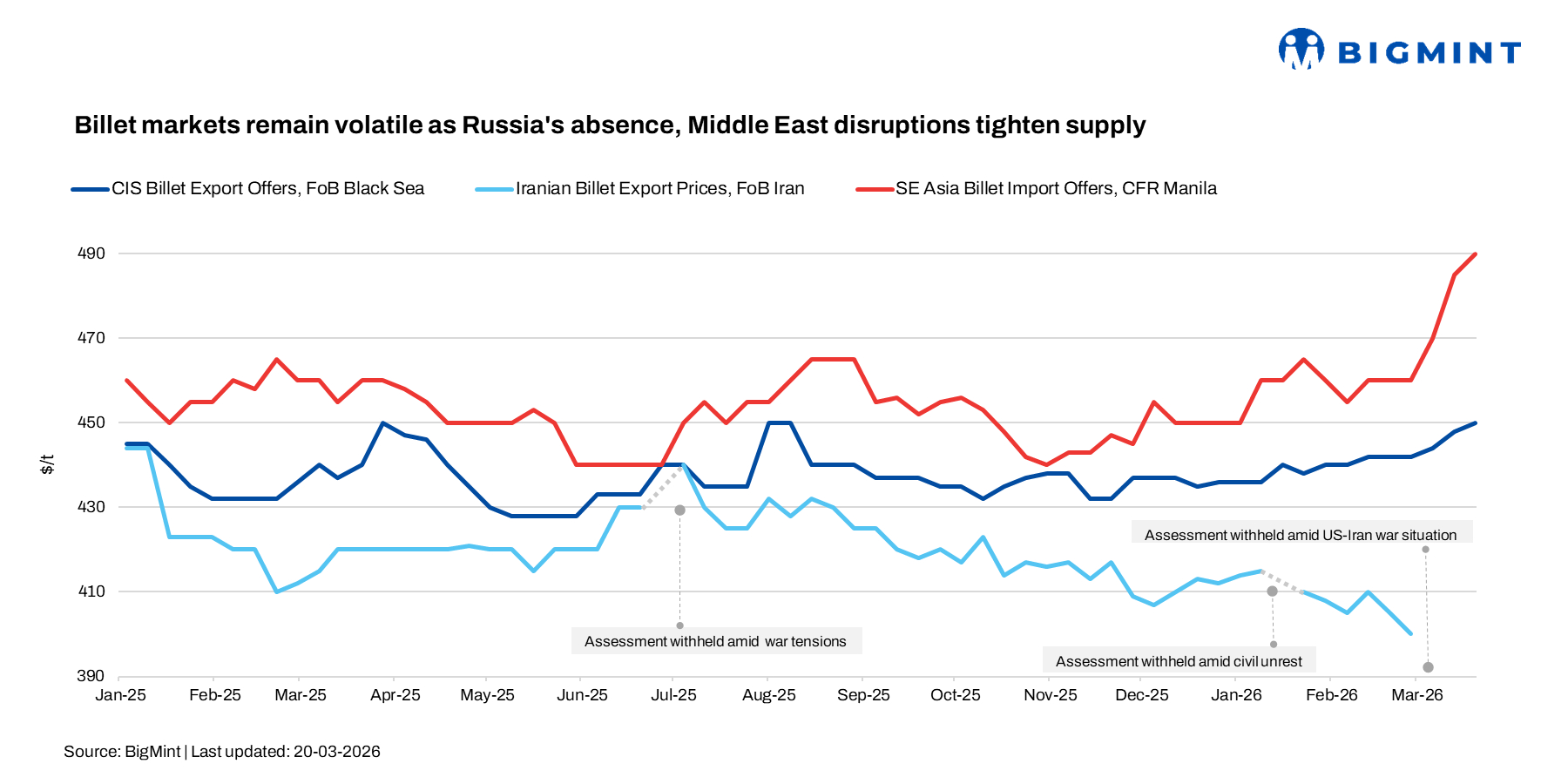

The global billet market remained volatile in the week ending 20 March, with prices largely supported by supply-side disruptions, geopolitical tensions, and shifting trade flows.

In the Black Sea, CIS-origin billet prices increased w-o-w, with some suppliers quoting even higher levels amid firm cost pressures. However, a sharp depreciation of the rouble against the US dollar triggered a slowdown in trading activity, as both buyers and sellers adopted a cautious, wait-and-see approach.

Despite currency weakness, mills showed limited willingness to reduce offers, citing rising raw material costs and increased tax burdens.

At the same time, Turkish deep-sea scrap import prices strengthened to around $388/t CFR, supported by rising freight and energy costs amid ongoing Middle East tensions. Higher scrap costs are adding further pressure on billet production costs, reinforcing firm price expectations despite weak downstream demand.

Asia turns to China as CIS billet market faces uncertainty

In Asia, the continued absence of Russian billet since early January has reshaped trade flows, with buyers, particularly in Taiwan, shifting towards Chinese material, where export prices were heard at $455-460/t FOB. Tight availability of both domestic and imported scrap in Taiwan supported local steel prices, prompting mills to raise scrap and rebar prices, although downstream demand remained subdued due to elevated input costs.

Meanwhile, the CIS billet market showed firm pricing but rising uncertainty. Russian-origin billet offers increased to $455-460/t FOB Black Sea from $450-452/t w-o-w, with some suppliers indicating levels up to $470/t FOB amid limited selling pressure. However, a sharp depreciation of the rouble–from around RUB 80/$ to above RUB 84/$–slowed trading activity, as market participants adopted a wait-and-watch approach.

Despite currency weakness, mills remained reluctant to lower offers, citing higher raw material costs and increased tax burdens, with some preferring to defer exports rather than reduce prices.

In Turkiye, Russian billet deals were reported at $480-485/t CFR, with offers rising by around $8-10/t w-o-w, although activity remained partly subdued due to Ramadan holidays and regional instability.

In the Far East, suppliers stayed largely out of the market, with last offers around $425/t FOB amid weak export viability amid high production costs. Overall, despite firm pricing, heightened currency volatility and geopolitical risks kept CIS billet indicatives heard stable at around $448-450/t FOB.

A Southeast Asia-based trader noted that billet offers into Thailand were heard at $480-485/t CFR for 3sp, although buyers were expecting lower levels and remained on the sidelines.

Chinese billet export offers for May-June shipments were also heard around $460/t FOB, indicating limited price movement, with currency stability further keeping the market largely unchanged.

Middle East markets tighten on supply and logistics constraints

In the Middle East, billet markets saw strong upward momentum, particularly in Saudi Arabia, where domestic billet prices rose sharply to around $540/t exw from $510-525/t in earlier weeks of the month. The increase was driven by tightening raw material supply and logistical disruptions, especially affecting integrated producers.

Market participants indicated that mills are largely booked for March, with limited spot availability supporting firm prices. Import billet offers for May shipments were heard at $510-520/t CFR, though trade routes remain fragile and options restricted.

In the UAE, regulatory developments added further complexity to the billet market. Authorities intensified scrutiny on steel imports following the arrival of a vessel carrying approximately 30,000 t of billet and wire rod reportedly linked to Iran.

The cargo was denied discharge, and the vessel departed without unloading. This incident triggered inspections across steel companies to ensure compliance with ECAS norms and prevent unfair trade practices. Market participants expect tighter enforcement of import regulations and stricter origin checks, which may limit sourcing flexibility and reshape trade flows, particularly for material from high-risk regions.

Outlook: In the coming days, global billet markets are expected to remain firm but highly volatile. Supply disruptions, freight constraints, and geopolitical tensions will continue to support prices, while currency fluctuations and weak downstream steel demand in CIS regions may cap further upside. Trade flows are likely to remain fluid, with buyers adapting sourcing strategies based on availability and cost competitiveness.

Leave a Reply