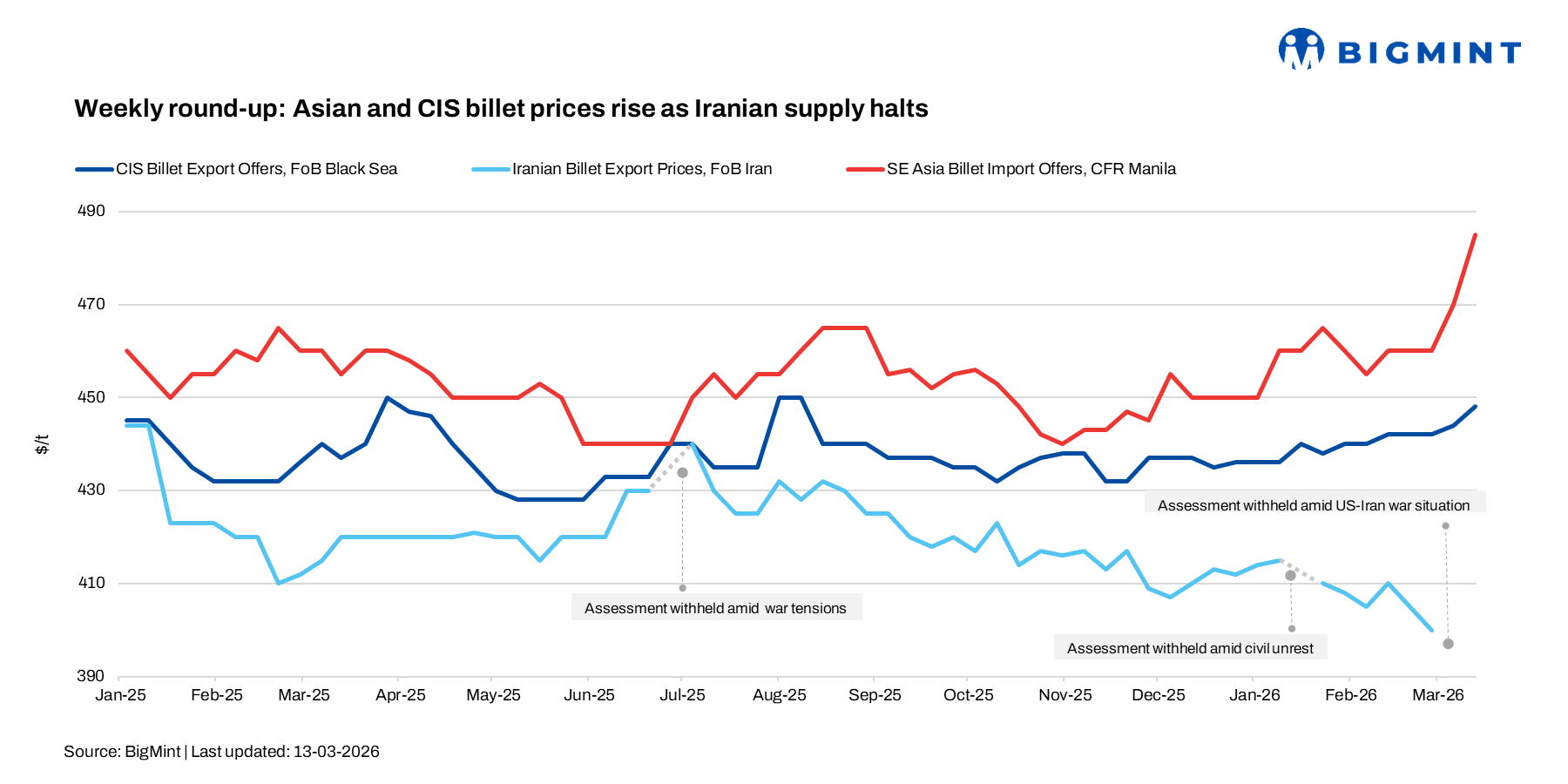

- Middle East tensions disrupt billet flows and lift freight costs

- Chinese billet offers rise as Southeast Asia turns to alternative supply

- Turkish mills postpone scrap bookings amid weak rebar demand

Rising geopolitical tensions in the Middle East are driving global steel billet trade flows, with disruptions around the Strait of Hormuz increasing freight costs and limiting supply availability.

The absence of Iranian billet in export markets has tightened supply in Southeast Asia, pushing Asian billet prices higher. At the same time, Turkish mills have largely stayed out of the deep-sea scrap market due to weak finished steel demand and reduced production.

Chinese billet gains support as Iranian supply disappears

Export prices for Chinese billets continued to strengthen during the week as Southeast Asian buyers increasingly turned to Chinese suppliers following the disruption of Iranian exports. Market sources indicated that Chinese mills raised 3sp billet export offers by about $8-10/t w-o-w, with May shipment cargoes heard at $458-460/t FOB, compared with $450-452/t FOB earlier in the week.

Workable levels for Southeast Asian buyers were heard at around $452-454/t FOB, up by approximately $5/t w-o-w.

A major trading house representative noted that Chinese billet export offers have firmed slightly, with 3SP billet heard at $455-460/t FOB for May shipment. Workable levels for Southeast Asian buyers were reported at around $450-452/t FOB a gradual uptick in market sentiment. The source added that the disruption in Iranian billet flows has redirected buying interest toward Chinese suppliers, with a few deals heard for Thailand and the Philippines at around $485-490/t CFR earlier this week.

Several transactions were reported across Southeast Asia. In Thailand, a 20,000-25,000 t cargo of Chinese high-Mn billet was booked at around $490/t CFR, while another 10,000-12,000 t contract for base-grade billet was heard near $475-480/t CFR. In the Philippines, Chinese 5sp billet was reportedly traded at $484-485/t CFR Manila, while fresh offers for Chinese and Malaysian origins were heard at around $494-496/t CFR.

Domestic sentiment in China also lent support to export offers. Chinese billet prices increased RMB 40/t ($6t) w-o-w to RMB 2,970/t ($431/t) on 13 March, supported by improving steel consumption and firm raw material costs such as iron ore and coke.

CIS billet offers edge higher on stronger market cues

Producers in the Black Sea region also revised their export prices upward, supported by rising Asian billet prices and stronger sentiment in the Turkish long steel market. Russian square billet for May shipment was heard at $450-455/t FOB Black Sea, compared with $445-448/t FOB a week earlier.

Market participants suggested that further increases remain possible. Suppliers indicated that mills may offer discounts of around $3-4/t for buyers willing to make a 20-25% prepayment, though many sellers remain confident that prices will move higher if global billet offers continue rising.

Despite firmer billet prices globally, activity in the Turkish import scrap market remained extremely limited. Steelmakers continued to delay bookings as weak rebar demand forced mills to operate at reduced capacity.

No fresh deep-sea scrap deals were reported during the week. A market participant noted that mills currently have little urgency to procure raw materials given sluggish finished steel demand.

Indicative target levels from US exporters for HMS (80:20) were heard at around $380-382/t CFR Turkiye, largely amid higher logistics costs. However, suppliers have not been actively pushing firm offers, and most negotiations remained on hold as mills monitored market developments.

Iranian export disruption reshapes regional trade

The most significant supply shock has come from Iran, where escalating security tensions have effectively halted steel exports across the value chain. Shipments of billets, slabs, pellets and iron ore concentrates have stalled, with cargoes reportedly stranded at Bandar Abbas port as shipowners hesitate to cross the Strait of Hormuz amid rising security risks.

Loading activity at Iranian ports has slowed sharply, with daily volumes estimated at 2,500-3,000 t, far below normal operating levels. Overland shipments to neighbouring markets such as Afghanistan, Iraq and Turkiye have also stopped.

Before the escalation, Iran had been expanding its steel exports. According to the Iranian Steel Producers’ Association, semi-finished steel exports rose over 30% y-o-y to 6.5-6.6 mnt during the first ten months of the Persian year, with billet and bloom shipments alone reaching nearly 4.9-5 mnt.

With exports now effectively frozen and freight risks rising in Gulf shipping routes, the absence of Iranian material is tightening billet supply across several Asian markets and supporting export prices.

Outlook

Outlook

Asian billet export prices are expected to remain firm in the short term as Iranian supply disruptions and rising freight costs support offers from Chinese and CIS suppliers. However, demand-side uncertainty persists, particularly in Turkiye where weak rebar sales continue to limit scrap procurement and production rates.

Leave a Reply