- Shipments from Indonesia, Colombia, South Africa surge w-o-w

- Volumes recover post Indian festive season despite weak demand

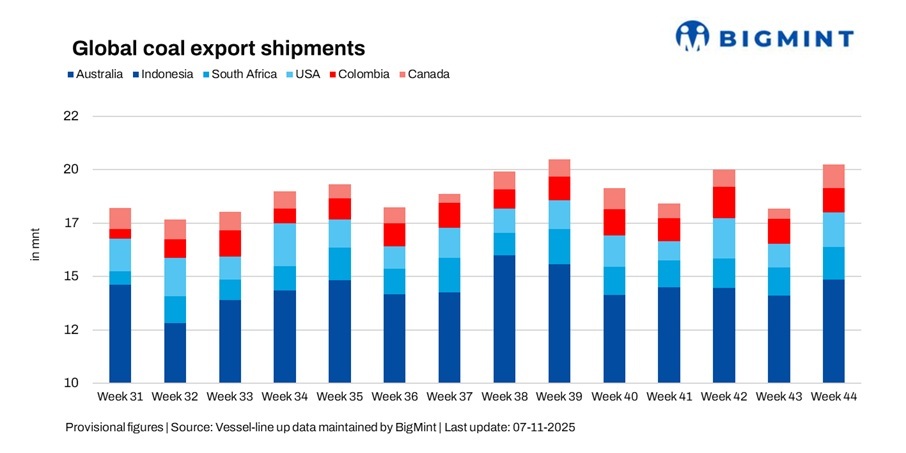

Global seaborne coal exports rose 11.1% w-o-w to 19.84 million tonnes (mnt) in week 44 (25-31 October 2025) from 17.85 mnt in week 43 (18-24 October), according to BigMint’s vessel line-up data. The rebound was led by stronger shipments from Indonesia, Colombia, Canada, and South Africa, while Australia maintained steady throughput.

Market activity improved modestly, as vessel scheduling normalised following the Indian festive season and export nominations increased from key producing regions. However, muted industrial demand, selective procurement by Asian utilities, and freight softness on certain routes kept sentiment cautious.

Country-wise trends

Australia’s coal exports increased 2.2% w-o-w to 7.21 mnt in week 44 from 7.06 mnt in week 43, supported by steady operations at key terminals — Newcastle (3.34 mnt), Gladstone (1.21 mnt), and DBCT (0.96 mnt). Consistent miner output and smooth port performance helped sustain throughput, even as buying interest from northeast Asian utilities remained selective.

Demand from Japan (2.10 mnt) and China (1.61 mnt) continued to anchor shipments, while Indian purchases stayed limited amid elevated freight costs. Major exporters, including Yancoal (0.50 mnt), BHP (0.47 mnt), and Glencore (0.44 mnt), maintained stable loading activity. Overall sentiment remained firm, supported by balanced supply conditions and steady regional demand.

Indonesia’s coal exports rose sharply by 8.1% w-o-w to 7.45 mnt in week 44 from 6.89 mnt in week 43, supported by improved vessel availability and stronger loading activity across key terminals in East and South Kalimantan. Major load ports included Taboneo (1.43 mnt), Bunati (1.16 mnt), and Samarinda (0.81 mnt).

The rebound followed a subdued post-festive week, as restocking by regional power utilities helped lift volumes. However, muted Indian demand and sluggish industrial consumption across Southeast Asia restricted further upside, with freight softness and cautious chartering weighing on overall momentum. On the demand side, China (2.11 mnt) remained the leading importer, followed by India (1.64 mnt), the Philippines (0.52 mnt), and South Korea (0.49 mnt).

South Africa’s coal exports increased 16.4% w-o-w to 1.48 mnt in week 44 from 1.27 mnt in Week 43, supported by a gradual improvement in rail logistics and vessel turnaround at Richards Bay (1.48 mnt). Although operational bottlenecks and intermittent rail delays persisted, better scheduling and improved coordination helped boost throughput.

India (0.59 mnt) remained the principal buyer, but elevated freights and cautious trading sentiment continued to limit fresh fixtures. Overall, market activity was subdued, as participants monitored cost pressures and vessel availability across the Atlantic and Indian Ocean markets.

Colombia’s coal exports surged 41% w-o-w to 1.55 mnt in week 44 from 1.10 mnt in week 43, driven by improved port operations and higher cargo nominations from key producers. Loadings from Puerto Nuevo (0.97 mnt) and Puerto Bolivar (0.44 mnt) rose notably as earlier operational disruptions eased.

Major shippers included Prodeco Group (0.98 mnt) and Cerrejon Mines (0.44 mnt), both contributing to the week’s strong rebound. The uptick was supported by a mild recovery in Atlantic basin demand, although persistently high freight costs and weak European procurement kept overall sentiment subdued. The Netherlands (0.50 mnt) emerged as the leading importer during the week.

US coal exports edged up 2.8% w-o-w to 1.09 mnt in week 44 from 1.06 mnt in week 43, supported by steady operations at key Gulf and East Coast terminals. Major loadings were recorded at Baltimore (0.41 mnt) and Norfolk (0.40 mnt), helping maintain throughput despite limited fixture activity.

Demand remained subdued, with India (0.22 mnt) serving as the leading destination, followed by Brazil (0.19 mnt) and the Netherlands (0.16 mnt). However, muted European and Asian buying interest alongside elevated voyage costs continued to weigh on sentiment, keeping overall export momentum largely flat.

Canada’s coal exports more than doubled w-o-w to 1.06 mnt in week 44 from 0.47 mnt in week 43, marking a sharp rebound after weeks of logistical disruptions. The recovery was supported by improved rail connectivity and smoother operations across major terminals — Roberts Bank (0.43 mnt), Prince Rupert (0.33 mnt), and Vancouver (0.30 mnt).

Elk Valley Resources (0.30 mnt) emerged as the major shipper during the week. The rise primarily reflected catch-up shipments from earlier delays rather than new demand, as elevated freight costs and subdued Pacific basin buying continued to limit incremental bookings. On the demand side, Japan (0.52 mnt) was the leading importer, followed by South Korea (0.38 mnt) and China (0.16 mnt).

Coal freights remain mixed across key routes

Dry bulk coal freights exhibited mixed momentum during week 44, as Indian demand remained tepid following the festive season. While rates on the Australia-India corridor held firm amid steady tonnage demand, the South Africa-India route stayed largely stable in the absence of fresh fixtures. In contrast, the Indonesia-India route softened further amid weak cargo flow and cautious market participation.

Overall, freight volatility and rising bunker costs tempered export recovery from several origins, while cyclone-related disruptions along India’s east coast added to logistical uncertainty. With limited chartering activity and muted buying interest across key Asian markets, freight-sensitive shipments — particularly from Indonesia and the Atlantic basin — faced headwinds despite improved port performance.

Outlook

Global coal exports are expected to remain broadly steady in the near term, supported by stable Australian output and recovering Indonesian loadings. However, mixed freight sentiment and soft buying from India and Southeast Asia may restrict further gains.

Atlantic suppliers such as Colombia and Canada could maintain moderate volumes provided logistical conditions remain favourable, though overall trade momentum is likely to stay range-bound through early November amid cautious procurement and cost pressures.

Leave a Reply