- Import moratorium to last until Dec’25; window open till mid-Feb

- Philippines reduces 2025 import forecast to 4.9 mnt amid freeze

The Philippines’ Department of Agriculture (DA) announced that rice imports will likely recommence in mid-January 2026, following a four-month suspension of shipments designed to bolster prices at the farm-gate and build buffer stocks ahead of the next harvest cycle.

Imports were halted beginning 1 September under an executive order yet to be formally issued that suspends the importation of regular- and well-milled rice through December, the DA said. The agency confirmed the order is expected imminently. “By January, we definitely need imports because there will be no additional harvest,” spokesman Arnel V. de Mesa told reporters, explaining the timing of the policy window.

Stabilising the domestic palay-rice chain

The decision is driven by the twin objectives of stabilising farm-gate palay (unmilled rice) prices and ensuring adequate domestic supply during the lean period before the next main crop. While the ban helped curb downward pressure on palay prices, the DA acknowledged that retail rice prices have not significantly risen to date.

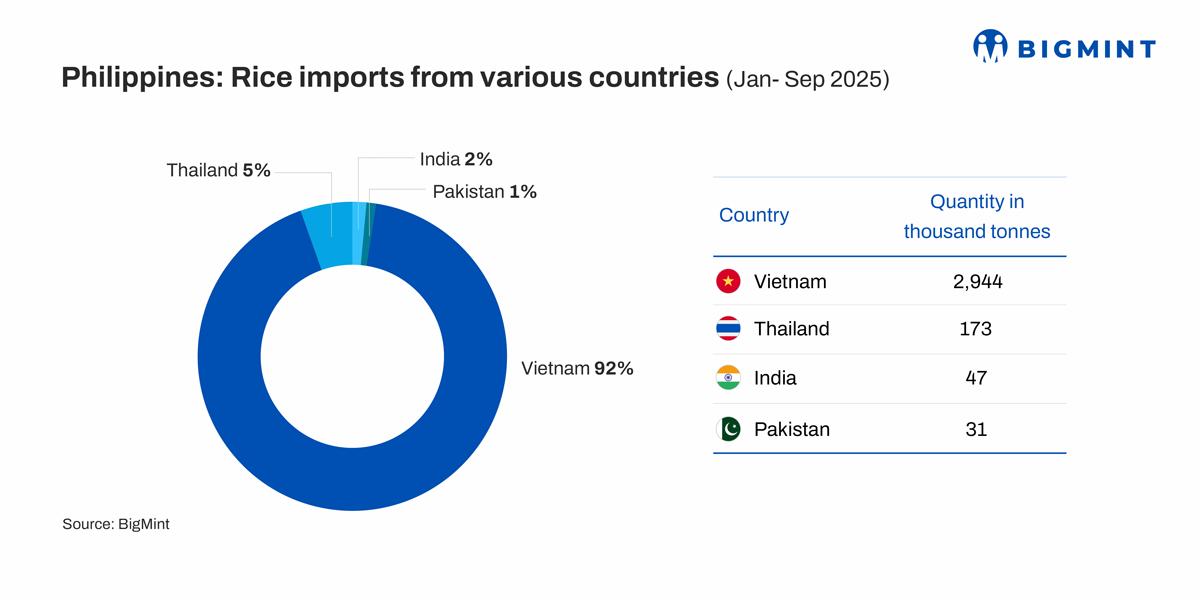

In August, the US Department of Agriculture trimmed its forecast for Philippines rice imports in 2025 to 4.9 million tonnes (mnt), down from an earlier estimate of 5.4 mnt, in light of the ban. Till August, imports had reached 2.58 mnt in CY’25, compared with 4.81 mnt in the same period of 2024. The Philippines remains the world’s largest rice importer.

Import window, inventory strategy

The import window is scheduled to run from mid-January through mid-February, allowing the government and commercial sector to build rice inventories before the March-May harvest begins. The DA flagged that another import freeze may be reimposed later in the year if local crop yields remain strong and farm-gate prices come under pressure. “It’s possible that we may reimpose a ban if harvests remain strong, to protect farm gate prices,” de Mesa said.

This approach reflects a shift towards cyclical trade controls calibrated to domestic production rhythms. De Mesa noted that the next lean period is expected in July-August ahead of the September harvest.

Vietnam continues to dominate the Philippines’ rice supply, accounting for 70-80% of total imports, mostly 5% and 25% broken white rice that fit domestic demand. Shipments move from Ho Chi Minh City and Mekong Delta ports to Subic, Manila, and Cebu. Thailand is the second-largest supplier, providing premium white and jasmine rice, while Myanmar, India, and Pakistan fill smaller market gaps.

Challenges, farm-level response

Farmer groups remain cautious about the benefits of the ban. Federation of Free Farmers national manager Raul Q. Montemayor pointed out that palay farm-gate prices dropped to PHP 15.60/kg in September from PHP 17.11/kg the previous month despite the import moratorium. Production cost is estimated at about PHP 14.50/kg, limiting effective margin for many growers. He also warned that the ban has likely benefited traders more than farmers, given that most of the wet-season harvest had already been delivered to millers.

Meanwhile, the National Food Authority and commercial stocks of rice are being monitored closely: import suspension means fewer foreign rice arrivals, requiring stronger data-based inventory management to avoid supply gaps. Montemayor estimated that foregone imports between October and December would reduce supply by about 1 mnt.

Outlook for market participants

For rice traders, millers and importers, the January-February import window presents a defined short-term opportunity to load foreign rice ahead of domestic production. For producers, the outcome of this import cycle will test the ability of trade-policy tools to sustain palay prices and shape planting incentives ahead of the next harvest.

If yields across the Philippines rise significantly and domestic production meets or exceeds expectations, the government may trigger a secondary import moratorium later in the year as a support mechanism for local farmers. Conversely, if supply shortfalls or price spikes occur in the lean months, the window may be extended or reinforced via buffer releases.

Leave a Reply