- Hoa Phat trims HRC prices for Jan-Feb’26 sales

- Weak domestic demand drives further price cuts by mills

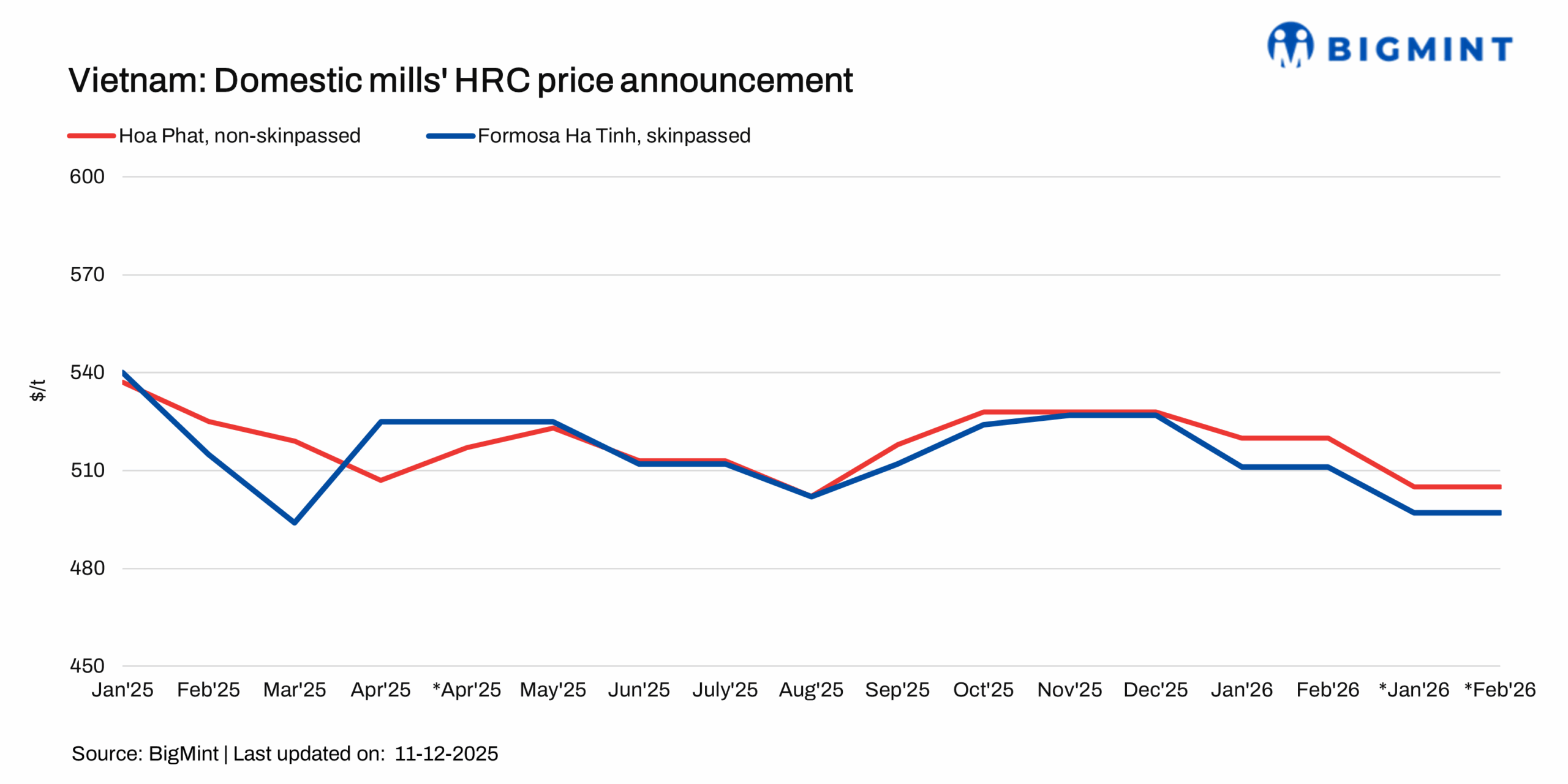

Vietnam’s leading steel manufacturer, Formosa Ha Tinh (FHS) has reduced its hot-rolled coil (HRC) prices by around $14/tonne (t) for sales in January 2026. With this adjustment, FHS’s HRC (SAE1006, skin-passed) is now priced at approximately $497/t CIF Ho Chi Minh City (HCMC).

Domestic demand in Vietnam remains sluggish following the severe damage caused by Typhoon Kalmaegi. Trading activity is largely limited to need-based buying, prompting mills to cut prices to stay competitive.

Market updates

1. Hoa Phat trims HRC offers, Baosteel raises prices: Vietnamese steel major Hoa Phat Group has further reduced its HRC (SAE1006, non–skin-passed) prices for sales in the first two months of 2026 sales by $15/t m-o-m. This revision represents a 3% decrease from the levels previously announced on 3 November. Updated prices in the southern region now stand at $505/t (VND 13,320,000/t), down from $520/t (VND 13,680,000/t), excluding VAT. The price cut reflects muted demand and cautious buying sentiment in Vietnam.

In contrast, Baosteel, the world’s leading steel manufacturer, has raised its HRC prices by RMB 100/t ($14/t) m-o-m for January 2026 sales after keeping it stable for three consecutive months. This rise in prices is attributed to an increase in SHFE HRC futures by RMB 36/t ($6/t) m-o-m to RMB 3,277/t ($464/t). Moreover, the prices of hot-dip galvanised also increased by RMB 100/t ($14/t) m-o-m.

2. Vietnam’s steel imports: Vietnam imported 1.52 million tonnes (mnt) of steel in November 25, remaining unchanged m-o-m. However, on a y-o-y basis, imports rose by 56,350 t, or 4%, compared with 1.46 mnt in November 24.

For the 11 months to November in 2025, Vietnam’s total steel imports reached 14.24 mnt, up by 1.88 mnt from 12.36 mnt in the same period last year. The majority of these imports came from China (8.38 mnt), followed by Japan (1.99 mnt), South Korea (1.50 mnt), Indonesia (1.18 mnt), and Taiwan (0.82 mnt).

Outlook

The Vietnamese steel market is expected to remain subdued in December on the back of weak domestic demand, with purchases largely limited to need-based requirements. This is likely to keep prices under pressure, and any improvement will hinge on a recovery in end-user demand across the region.

Leave a Reply