- Coking coal imports also edge higher, signaling firmer industrial activity

- Market points to restocking and supply security concerns rather than demand boom

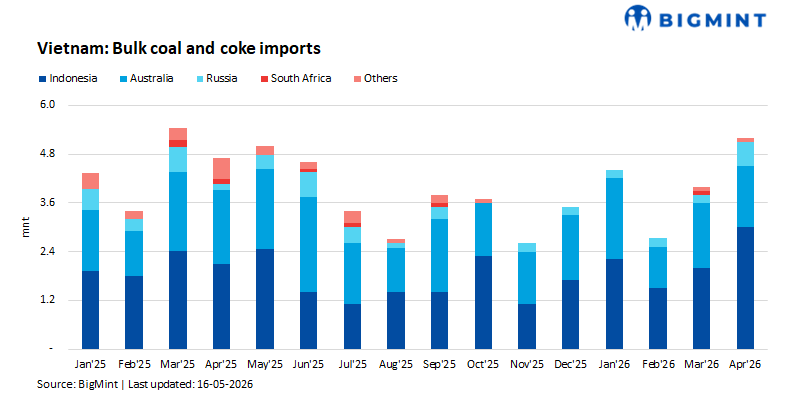

Vietnam’s coal imports recovered in April 2026, driven primarily by stronger buying of non-coking coal, after weak import activity during February and March.

Data for January-April 2026 shows Vietnam imported 16.3 million tonnes (mt) of coal, comprising 12.2 mt of non-coking coal and 4.1 mt of coking coal. While imports softened during the early part of the year, April marked a notable recovery, particularly in thermal coal procurement.

Thermal coal imports rebound in April

Vietnam’s non-coking coal imports increased to 3.9 mt in April, up from 2.9 mt in March, representing a 34% month-on-month increase.

After falling sharply to 2.1 mt in February, thermal coal imports have now recovered for two consecutive months, suggesting buyers returned to the market to rebuild inventories ahead of the summer demand period.

The April increase appears to reflect restocking activity rather than a sharp structural increase in coal demand, with utilities and industrial consumers likely securing prompt cargoes amid heightened uncertainty in global energy markets.

Coking coal imports also strengthen

Vietnam’s coking coal imports increased to 1.3 mt in April, compared with 1.1 mt in March, indicating firmer procurement by the steel sector.

After weakening to 0.6 mt in February, coking coal buying has steadily recovered, suggesting steelmakers may be preparing for stronger industrial activity or replenishing depleted inventories.

What is driving the recovery?

The rebound in Vietnam’s coal imports coincides with growing concerns over global energy security and elevated LNG prices in Asia.

Higher spot LNG prices have improved the competitiveness of coal-fired generation in several Asian markets, while ongoing geopolitical tensions have encouraged utilities to maintain higher fuel inventories.

At the same time, Vietnam’s thermal coal buying pattern suggests importers may be positioning for higher seasonal electricity demand during Q2 and Q3, rather than responding to an immediate surge in coal burn.

Outlook: Recovery visible, but not yet a structural shift

While April’s import rebound signals improving buying interest, the trend remains uneven.

Thermal coal imports remain heavily dependent on power demand, domestic coal availability and gas economics. A sustained rise in LNG prices could support further coal procurement, particularly for imported Indonesian and Australian material.

For now, the data points to Vietnam returning to the market after a weak first quarter, rather than a full-scale recovery in coal demand.

Leave a Reply