- US coal emerges as cost competitive alternative to petcoke

- Limited supply, rising freights help maintain firm prices

US-origin high-calorific value NAPP (Northern Appalachian) thermal coal moved firmly higher in the week ended 20 March 2026, with two Indian cement companies concluding deals for April loading and May arrival cargoes. The transactions, one for the east coast and another for the west coast of India, were finalised at around $145-146/tonne (t) on a CFR basis.

These deals mark a clear re-entry of Indian cement buyers into the US high-CV coal market after a period of cautious procurement. They also reflect a broader shift in pricing dynamics, with physical markets catching up to earlier strength seen in financial contracts. Global benchmarks have firmed, with FOB Newcastle 6000 moving toward $140/t, reinforcing the strength in high-CV coal demand.

At the supply end, US miners are currently offering fresh May-loading cargoes at around $115/t FOB. However, rising freights are pushing delivered prices significantly higher. Freights for Baltimore to West Coast India were recently quoted near $48/t, highlighting the growing impact of logistics on final procurement costs.

Coal regains advantage over petcoke on a calorific basis

The renewed buying interest in US NAPP coal is being driven primarily by a shift in fuel economics. High-sulphur US Gulf petcoke, at around 6.5% sulphur, was offered to Indian buyers at approximately $165/t CFR West Coast India.

When evaluated on a calorific basis, US NAPP coal at $145-146/t offers a more competitive cost per unit of energy. For cement manufacturers, this difference is significant, particularly for kiln operations where efficiency and fuel quality play a critical role.

As a result, buyers have shown a clear preference for high-CV coal over petcoke in recent transactions. This shift is not driven by a collapse in petcoke demand, but rather by a relative improvement in coal’s competitiveness, which has tilted procurement decisions in its favour.

Limited availability, rising freight tighten the market

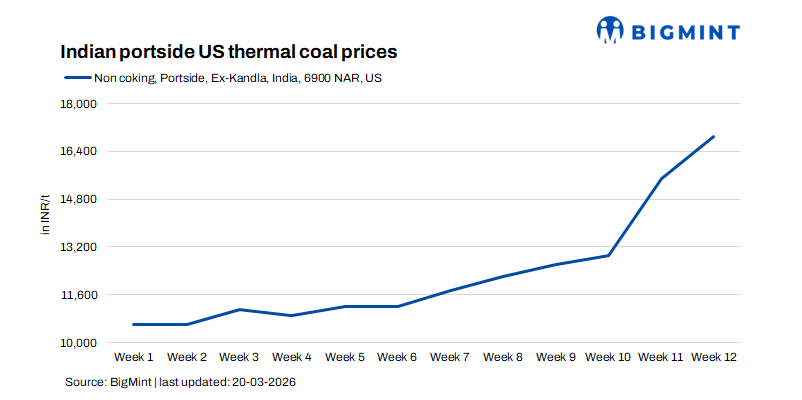

While demand has picked up, the availability of US NAPP coal in India remains tight. Market participants report that stocks at Kandla are largely exhausted, with no immediate replenishment visible. At Tuna, ex-port prices have moved above INR 17,000/t, with offers now ranging between INR 17,000/t and INR 18,000/t and expectations of further increases.

The supply pipeline appears thinner than usual. Traders indicate that, unlike last year when multiple US cargoes were arriving each week, the current flow of shipments is more limited. This has created a sense of scarcity in the spot market, particularly for high-CV material.

Freight has emerged as a key constraint. Rates on the US East Coast to India route have risen sharply, driven in part by bunker fuel shortages at Indian ports, which are delaying vessel turnaround and reducing effective fleet availability. This has increased the cost of moving cargoes and added another layer of tightness to the market.

Despite firm offers, buying activity remains selective, with some participants hesitant to chase higher prices. However, for high-quality US coal, demand has remained relatively resilient, supported by its superior calorific value and performance characteristics.

Rising prices begin to impact smaller consumers

The strength in US high-CV coal prices is now beginning to ripple through downstream markets. Brick kiln operators in northwestern India, including Punjab, Haryana, and western Uttar Pradesh, are facing increasing cost pressures due to elevated coal prices.

Industry associations are understood to be considering an early closure of operations this year, potentially before the traditional end of the production season in June. The sharp increase in fuel costs has eroded margins, raising concerns about the viability of continued production under current price conditions.

This highlights a divergence in the market. While large industrial consumers such as cement companies are able to absorb or pass through higher costs, smaller, price-sensitive sectors are more exposed and are beginning to adjust their operations accordingly.

Market direction: High-CV US coal firmly back in demand

The recent transactions underline a clear shift in favour of US high-CV coal in the Indian market. Demand from cement producers has strengthened, supply remains constrained, and freight is adding upward pressure on delivered prices.

In this environment, price discovery is increasingly being driven by the availability of prompt cargoes rather than benchmark levels. Access to physical supply, particularly high-quality material, has become a critical differentiator.

The market is therefore moving into a phase where high-CV US coal is not just competitive, but actively preferred — and where limited availability is likely to keep prices firm in the near term.

Leave a Reply