- Turkiye turns to imported billets over scrap due to cost efficiency

- Lower bulk purchases from Bangladesh, Mexico weigh on volumes

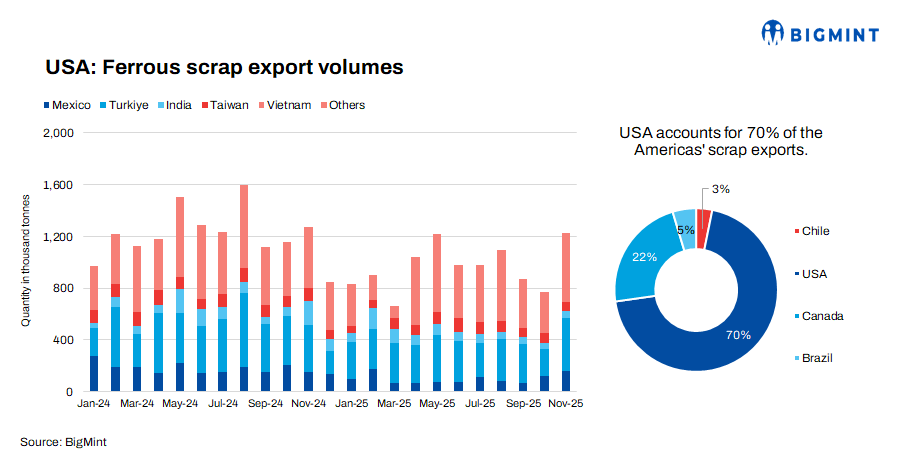

US ferrous scrap exports fell 18% y-o-y to 11.16 million tonnes (mnt) in January-November 2025 (11MCY’25) from 13.67 mnt in the same period of 11MCY’24. In November 2025, exports reached 1.23 mnt, up 60% m-o-m but down 3% y-o-y from November 2024.

The overall decline was driven by weaker demand from Turkiye, where mills increasingly opted for imported billets over scrap due to better cost efficiency, while stronger domestic US scrap prices also reduced export competitiveness. Lower bulk purchases from Bangladesh and Mexico further weighed on volumes. Although containerised shipments to parts of Asia showed some improvement, they were insufficient to offset the broader drop in bulk exports.

US scrap prices

Shredded scrap averaged $359/tonne (t) and HMS $324/t in 2025, both down $35/t y-o-y, amid weak overseas demand from Turkiye and Bangladesh, currency pressures, and ample US supply.

US ferrous scrap export prices also declined as soft Turkish steel demand prompted mills to reduce bids and defer bookings. Higher freight costs squeezed FOB margins, while competitive EU-origin cargoes and subdued buying from Bangladesh and Vietnam kept trading activity limited.

Country-wise US ferrous scrap exports

Turkiye: Turkiye remained the largest importer, even though volumes fell 21% to 3.37 mnt in 11MCY’25 from 4.24 mnt in 11MCY’24, showing slower intake.

Mexico: Scrap imports declined 45% to 1.1 mnt in 11MCY’25 from 1.99 mnt in 11MCY’24 due to weaker demand and reduced steel production.

Bangladesh: Imports fell 29% to 1.28 mnt in 11MCY’25 from 1.8 mnt in 11MCY’24, impacted by weak steel demand and currency pressures. Mill operating rates were at a low 35-40% throughout the year.

India: Imports fell 16% to 0.88 mnt in 11MCY’25 from 1.05 mnt in 11MCY’24, amid higher domestic scrap and DRI use.

Taiwan: Scrap imports dropped 22% to 0.86 mnt in 11MCY’25 from 1.1 mnt in 11MCY’24, reflecting weaker steel production and a shift to alternative raw materials.

US scrap imports rise 7%

US ferrous scrap imports increased 7% y-o-y to 4.42 mnt in 11MCY’25 from 4.15 mnt in 11MCY’24. However, imports fell 9.1% m-o-m to 0.40 mnt in November, compared with 0.44 mnt in October, reflecting softer steel demand and adequate domestic scrap availability. Earlier in the year, imports surged to a record high in March, driven by front-loaded buying amid tariff uncertainty and stronger inflows from key suppliers, before moderating in subsequent months.

US pig iron imports climb up

US pig iron imports rose 14% y-o-y to 4.95 mnt in 11MCY’25, up from 4.34 mnt in 11MCY’24, supported by steady mill demand for scrap substitutes. Volumes peaked in May and October before easing in November amid trade policy uncertainty and the higher cost of Indian-origin material, prompting cautious buying. Brazil remained the key supplier, though shipments softened in early to mid-2025 due to weaker price competitiveness and logistical constraints.

Crude steel production inches up

US crude steel production rose marginally by 1% y-o-y to 74.81 mnt in 11MCY’25, compared with 74.01 mnt in 11MCY’24, indicating largely stable output despite significant movements in raw material costs and evolving trade flows.

Scrap export dynamics in other American regions

Canada: Canada’s ferrous scrap exports declined by 7% y-o-y to 3.78 mnt in 11MCY’25, compared with 4.08 mnt in 11MCY’24. The drop reflects relatively weaker overseas demand compared to last year.

In November, exports stood at 0.40 mnt, down 13% m-o-m from 0.46 mnt in October, indicating softer shipments after stronger volumes m-o-m in October.

Canada’s ferrous scrap exports declined due to escalating trade tensions with the US, which led to the imposition of tariffs on steel in March 2025. These measures significantly reduced cross-border trade flows and weakened overall export momentum.

Slower manufacturing activity, particularly in steel-related sectors, and broader economic contraction further dampened scrap demand. Rising uncertainty, softer global steel production, and cautious buying from key Asian markets also weighed on volumes, resulting in lower ferrous scrap exports both q-o-q and y-o-y.

Brazil: Scrap exports from Brazil increased by 26% y-o-y to 0.78 mnt in 11MCY’25, compared with 0.62 mnt in 11MCY’24, reflecting stronger overseas demand, particularly from South Asia. India remained the major importer of Brazilian scrap, with volumes rising to 0.59 mnt in 2025 from 0.42 mnt in 2024.

In November 2025, exports stood at 0.07 mnt, up 17% m-o-m from 0.06 mnt in October, indicating improved late-year shipments. Shipments to Bangladesh moderated to 0.13 mnt from 0.15 mnt, while exports to the UAE and Pakistan were negligible in 2025.

However, alongside scrap, Brazil also recorded higher pig iron exports, increased crude steel production, and stronger iron ore export volumes in 2025, underscoring firm upstream output and resilient raw material demand across global markets.

Leave a Reply