- Only South Africa’s exports rise; rail flows to ports stay smooth

- Freight sentiment remains subdued amid ample vessel supply

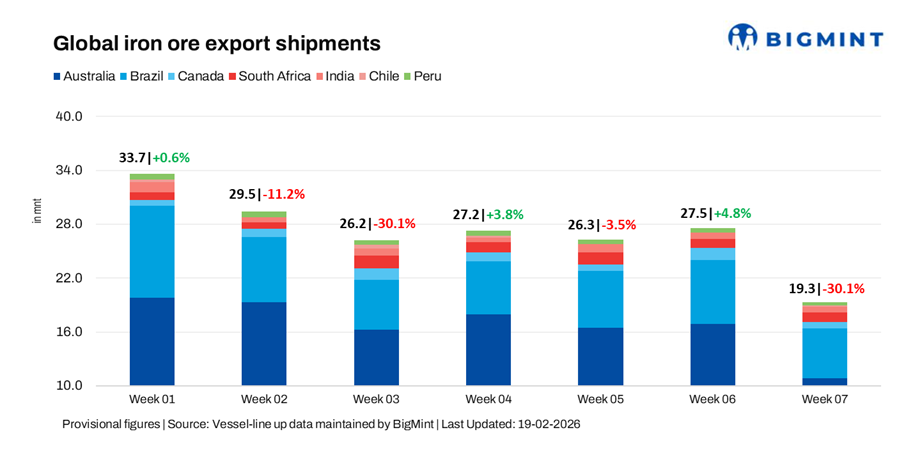

Global seaborne iron ore exports declined sharply by 30.1% w-o-w to 19.3 mnt in the week ending 13 February 2026 (week 07), compared with 27.5 mnt in week 06, as per BigMint’s vessel line-up data. Global export volumes plunged to their lowest since June 2025, since BigMint started tracking weekly data.

The decline was largely driven by sharp shipment cuts from major origins amid Chinese New Year holidays, with South Africa remaining relatively stable.

Country-wise trends

Port & shipper-wise trends

- Australia: China remained the dominant destination at 9.51 mnt. Port Hedland led Australian loadings at 6.51 mnt, driven by BHP (3.06 mnt) and Fortescue Metals (2.87 mnt), while Port Walcott shipped 1.30 mnt, entirely from Rio Tinto’s (1.30 mnt) Pilbara operations.

- Brazil: China imported 3.42 mnt. Port Ponta Da Madeira handled 2.30 mnt during the week, with the entire volume accounted for by Vale.

- Canada: Sept-Iles loaded 0.34 mnt, with Guinea and Nimba Mines contributing the entire volume. The sharp correction points to shipment rescheduling following last week’s spike, underscoring Canada’s typically volatile and cargo-driven export pattern.

- South Africa: Port Saldanha shipped 0.29 mnt to China. Although volumes rose w-o-w, exports remain relatively modest and continue to be highly sensitive to rail and port logistics constraints along the Saldanha corridor.

- India: China imported 0.11 mnt through Paradip, with OCL Iron contributing 0.058 mnt and Rungta Mines 0.052 mnt. Volumes remain highly freight-sensitive and are largely driven by short-haul demand from China.

- Peru: San Nicolas shipped 0.18 mnt, with Shougang Hierro accounting for the full volume. China was the sole destination for these exports.

- Chile: Caldera exported 0.035 mnt to China, with volumes remaining limited and largely driven by shipment timing.

Dry bulk iron ore freight market sentiment

Freight sentiment remained soft during the week as declining cargo volumes from Australia and Brazil reduced Capesize fixing momentum. Ample vessel availability, cautious Chinese procurement, Lunar New Year disruptions, and weak steel margins limited fresh spot activity.

Outlook

Global iron ore export volumes are likely to remain mixed in the subsequent week, driven by shipment scheduling and selective chartering. While Australia and Brazil may see normalisation after this week’s pullback, Chinese demand signals, port inventories, and freight fundamentals will continue to dictate export momentum.

Leave a Reply