- The Asian market remains reluctant to US scrap offers

- EU/UK cargoes compete with cheaper alternatives in Turkiye

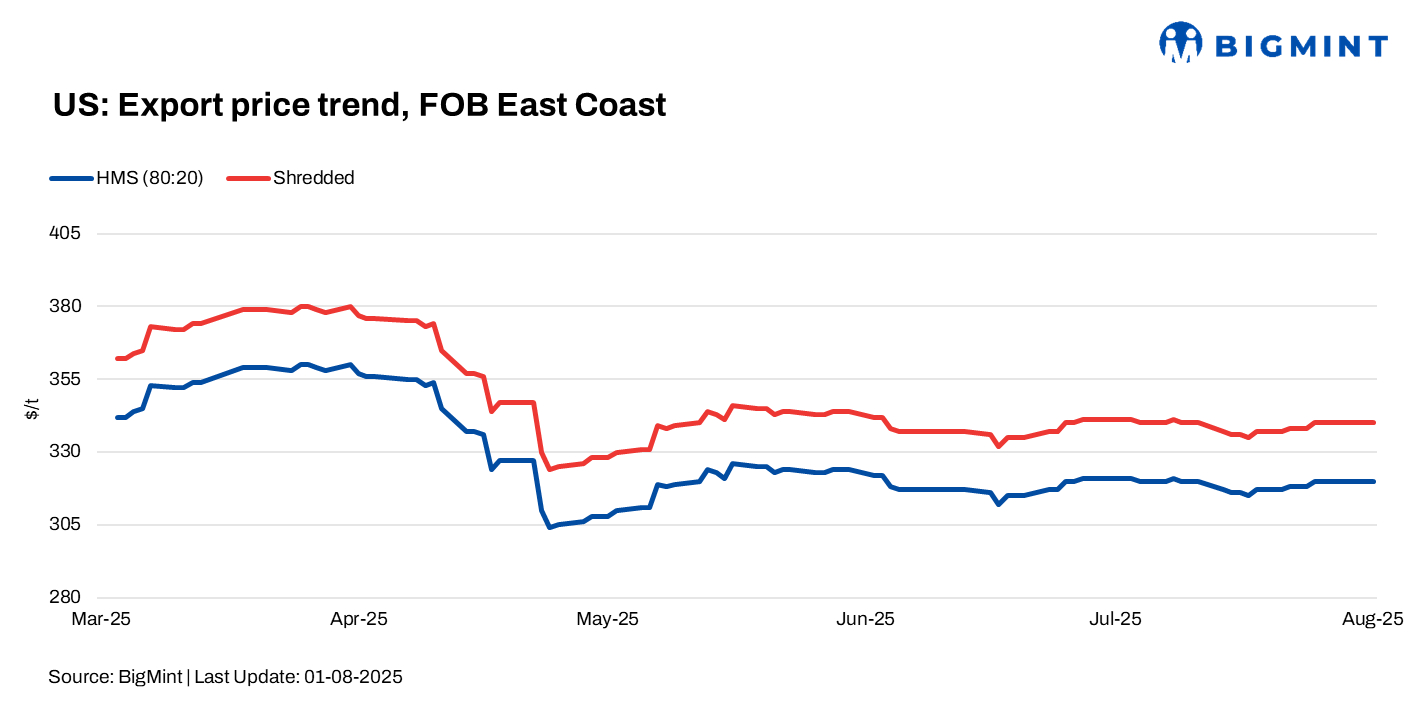

US ferrous scrap export prices remained stable w-o-w. The stability came as key markets like Turkiye held back from fresh bookings, awaiting clarity on finished steel demand and upcoming tariff policies, while South Asian buyers showed dull appetite for bulk inquiries amid liquidity concerns and seasonal slowdowns.

FOB assessments (US East Coast, bulk)

- HMS 80:20 – $320/t, stable w-o-w.

- Shredded – $340/t, stable w-o-w.

US-origin HMS 80:20, bulk – CFR assessments

- Turkiye – stable w-o-w at $346/t.

- Vietnam – down by $3/t w-o-w at $332/t.

- Bangladesh –up by $2/t w-o-w at $353/t.

Updates on key importers

Turkiye: Demand for US-origin HMS 80:20 in Turkiye stayed limited, with offer levels around $350/t CFR, as mills held back fresh bookings amid weak finished steel sales and uncertain near-term demand.

Factors weighing on Turkish buying interest

- Mills delayed purchases, awaiting clarity on steel sales.

- EU/UK cargoes at $340-343/t CFR offered cheaper alternatives.

- US recyclers kept offers firm despite muted Turkish interest.

With August requirements mostly secured, Turkish buyers remained on the sidelines, signaling that any pickup in demand will likely hinge on stronger rebar sales and clearer export orders in the coming weeks.

Bangladesh: US-origin HMS 80:20 bulk price for Bangladesh witnessed a rise with bulk offers heard at $358-360/t CFR Chattogram, although buyers held their quotes around $350-352/t with some shippers quoting up to $365/t. Suppliers from the US stayed firm, citing strong home demand, limiting price negotiations. Booking volumes stayed modest as buyers resisted higher levels.

A severe liquidity crunch and payment delays kept deals mostly on credit. Demand is expected to recover gradually after the monsoon and improved liquidity.

Vietnam: Demand for US-origin scrap in Vietnam remained weak. Deep-sea offers were heard at $340/t CFR, but bids lagged at $325-330/t, leaving the market sluggish as the wide gap stalled deal activity. Ample inventories and slow construction kept mills cautious, while rising Japanese inflows further pressured offers and reduced US-origin scrap demand.

Outlook

Market sentiment remains mixed. Some participants expect support from higher global offers and potential demand recovery in South Asia, while others remain cautious amid weak steel fundamentals and uncertainty over the enforcement of US tariff measures.

Leave a Reply