- Margins remain stable despite soft LME prices

- Zinc International’s production rises 50% y-o-y

Vedanta Limited recently revealed its Q1FY’26 performance in the zinc segment, marked by steady production, ongoing cost management, and progress on expansion initiatives.

Operational performance

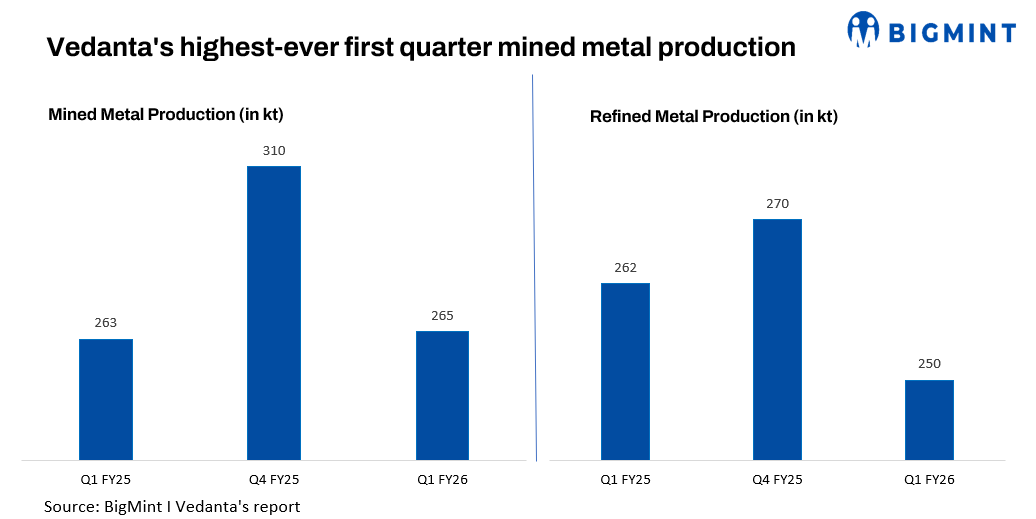

Hindustan Zinc Limited (HZL), a subsidiary of Vedanta, recorded its highest-ever Q1 mined metal production at 265,000 tonnes (t), a slight 1% increase y-o-y. However, refined metal output declined by 5% y-o-y to 250,000 t, attributed to scheduled maintenance. The cost of production (CoP) reached a record low of $1,010/t, a 9% y-o-y decrease, reflecting operational efficiencies.

Vedanta Zinc International’s operations posted a 50% y-o-y increase in mined metal production to 57,000 t, supported by a 74% y-o-y rise in output at Gamsberg. The cost of production improved to $1,269/t, a 21% y-o-y reduction.

Strategic growth

Vedanta approved a 250,000 tonnes per annum (tpa) metal capacity expansion at HZL. It also secured mineral blocks for potash in Rajasthan and rare earth elements in Uttar Pradesh, indicating a move towards resource diversification.

Sustainability focus

HZL was included in the top 1% globally in the S&P Global Sustainability Yearbook 2025. Broader ESG efforts at Vedanta include 48% water recycling, 72% waste utilisation, and 3.5 million trees planted as of Q1FY’26.

Financial highlights

Vedanta reported consolidated revenue of INR 37,434 crore, a 6% y-o-y increase, and EBITDA of INR 10,746 crore. Zinc India contributed INR 3,815 crore to EBITDA. Despite a 7% y-o-y decline in average zinc LME prices to $2,641/t, margins remained stable.

Outlook

The zinc business is expected to remain stable. Record-low production costs, increasing volumes at Gamsberg, and the planned 250,000 tpa expansion at HZL provide a basis for long-term growth. While LME prices remain soft, cost efficiency and progress in ESG initiatives are likely to support margins. The Gamsberg Phase 2 ramp-up and recent mineral block acquisitions may contribute to medium-term development.

Leave a Reply