- Limited scrap availability, firm offers support prices

- Turkiye, B’desh expected to begin pre-Eid restocking

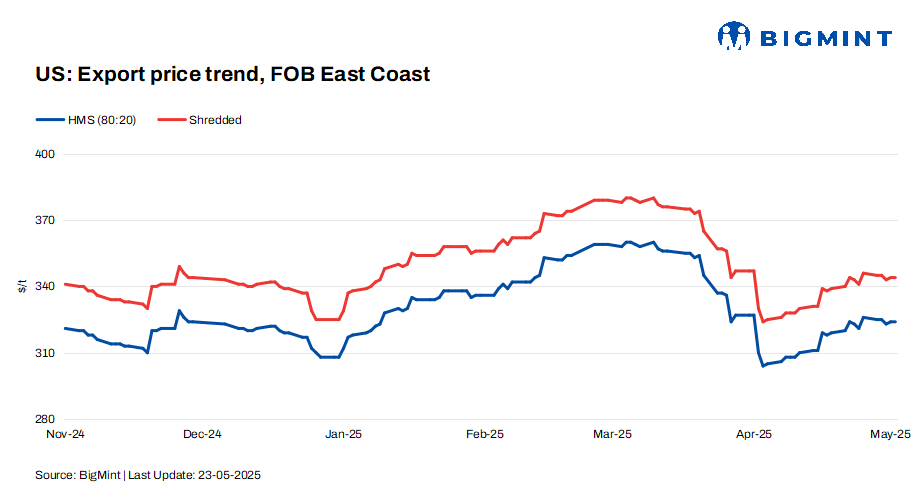

BigMint’s US ferrous scrap export index remained range-bound this week, edging down by $2/tonne (t) w-o-w, despite moderate activity following Turkish steelmakers’ relatively stable approach towards fresh bookings.

According to a market participant, “A US West Coast-based source noted that persistently low prices have significantly slowed scrap inflows into export yards. Sellers are unwilling to deliver at these levels, especially with high fuel costs and elevated operating expenses.”

FOB assessments (US East Coast, bulk)

- HMS 80:20 – $324/t, down $2/t w-o-w.

- Shredded – $344/t, down $2/t w-o-w.

Key importers

Turkiye: Demand for US-origin scrap in Turkiye showed modest improvement this week, despite trading activity being slow overall. Mills accepted slightly higher prices due to low scrap inventories for June shipments.

Most US suppliers held firm, offering HMS 80:20 at $350-352/t CFR, though no confirmed bids were heard. European offers remained slightly lower at $338-345/t CFR but still faced resistance from Turkish mills. Traders noted that tight availability and limited inventories supported firmer seller sentiment.

Other reasons for the rising demand in Turkiye are as follows:

- Firmer long steel sales helped mills absorb rising input costs.

- Mills are planning to restock ahead of Eid al-Adha.

Bangladesh: Demand for US-origin ferrous scrap in Bangladesh remained steady over the week, with moderate inquiries and stable workable levels, as mills showed selective buying interest.

Construction activity was moderate with the onset of the rainy season, and further slowdown is expected ahead of Eid next month. This kept overall scrap demand in check, although some mills are expected to resume restocking as the holiday approaches.

Additionally, market sentiment remained cautious due to persistent political uncertainties and tight liquidity, which continued to weigh on the domestic scrap and finished steel sectors.

Vietnam: Demand for US-origin scrap in Vietnam showed a slight improvement this week. The uptick was supported by easing US-China trade tensions, which helped boost seller optimism.

However, Vietnamese steelmakers remained cautious in accepting higher scrap prices due to weak downstream steel demand and sluggish finished product prices. Buying interest stayed limited amid ongoing market uncertainties.

A trader cited weak demand and a wide bid-offer gap, noting limited market impact from a brief billet shortage after a minor fire shut down Hoa Phat’s blast furnace in Dung Quat. Finished steel prices rose by $6-7/t early in the week.

CFR assessments (US-origin HMS 80:20, bulk)

- Turkiye: $347/t, stable w-o-w.

- Vietnam: $340/t, up by $2/t w-o-w.

- Chattogram: $373/t, up by $1/t w-o-w.

Outlook

Some exporters are unwilling to fulfill older orders at the previous contracted prices, hoping for a hike to negotiate higher, more favourable tags. This could lend short-term support to export values. With supply tightness and selective restocking ahead of Eid in key markets, firm sentiment may persist for early June.

![]()

Leave a Reply