- Vietnam stays wary amid muted demand, weak steel prices

- Taiwan’s H2 tags up $5/t on easing US-China trade tensions

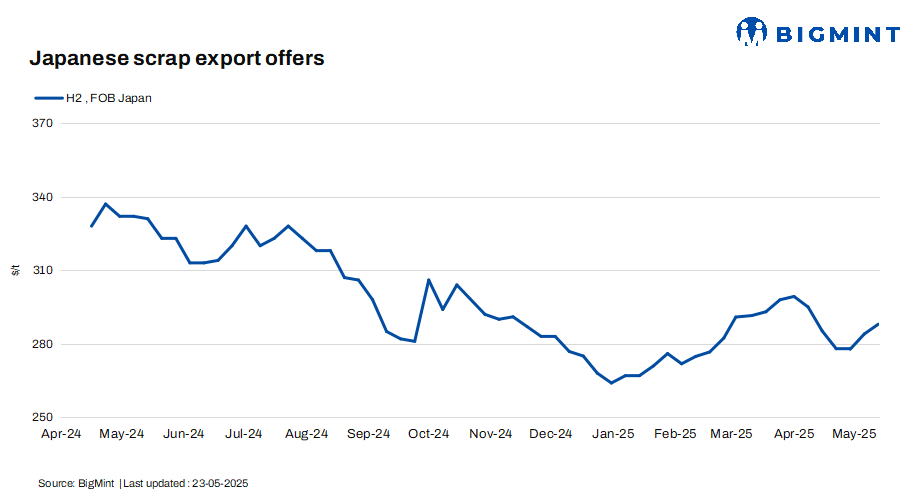

Japanese H2 scrap export prices dipped this week, driven by Tokyo Steel’s price cut and subdued interest from major overseas buyers. BigMint assessed H2 at JPY 41,200/tonne (t) ($287/t) FOB Tokyo Bay, down JPY 100/t ($1/t) from the previous week’s JPY 41,300/t ($288/t).

In its first scrap procurement price adjustment this month, Tokyo Steel reduced rates at its Kyushu plant by up to JPY 500/t ($3/t), effective 21 May 2025, while tags at all other plants were kept unchanged. Following the revision, H2 scrap prices at the Kyushu plant stood at JPY 40,500/t ($281/t).

Other market updates

Vietnam: Vietnam’s imported scrap market saw a modest $2/t rise, supported by easing US-China trade tensions, with Japanese H2 assessed at $325/t CFR. Sellers offered bulk Japan-origin H2 at around $320-325/t, but buyers remained cautious with bids near $315-320/t amid weak steel demand and soft downstream prices.

A fire at Hoa Phat’s Dung Quat blast furnace caused a temporary billet shortage, briefly pushing northern finished steel prices up by $6-7/t. Domestic scrap prices were mixed, with northern bids rising slightly and southern tags dipping.

Barring a slight revision, Vietnam maintained its anti-dumping duties on Chinese hot-rolled coil (HRC) imports to protect local producers. Despite some supply disruptions, weak demand and competitive pricing from major mills such as Formosa are expected to keep the market stable and range-bound in the near term.

South Korea: South Korea’s ferrous scrap inventory declined for the third consecutive week, dropping about 1% to 799,000 t, influenced by company-specific factors and maintenance schedules. Major steelmakers Hyundai Steel, Dongkuk Steel, and Hwanyang Steel increased scrap purchase prices by JPY 10,000/t ($7/t) across all grades, while SeAH Besteel raised tags by JPY 15,000/t ($11/t) for all grades.

The central region’s stock rose 2% to 432,000 t, while the southern region saw a 5% fall to 344,000 t. Despite it being the peak season, inventories remained low, with only a brief price-driven increase early in the month. Scrap supply remained tight as a result of April’s price cuts and the holidays in early May.

As shortages persisted, steelmakers responded by raising purchase prices to balance supply and demand. Further price hikes are possible, but market participants are cautious due to weak steel prices and rising costs.

Taiwan: Taiwan’s imported scrap market showed signs of recovery, with prices of Japan-origin H2 rising by $5/t w-o-w to $313/t CFR, marking a notable rebound after two months of weakness.

In response, Taiwan’s largest rebar producer, Feng Hsin Steel, raised both its rebar list prices and local scrap procurement prices by TWD 200/t ($7/t).

This marks the company’s first price hike in two months, driven by higher imported scrap costs and an improvement in domestic market sentiment. The uptick was also supported by the recent easing of US-China trade tensions, which helped lift steel market confidence.

Outlook

Japanese H2 prices are likely to remain under slight pressure due to Tokyo Steel’s cuts and weak demand, while Taiwan’s imported scrap market is rebounding, driven by improved sentiment and easing trade tensions. Vietnam’s market may remain cautious amid soft steel demand and anti-dumping measures, despite supply disruptions. South Korean steelmakers are expected to continue adjusting scrap purchase prices in response to low scrap inventories while balancing cost pressures.

![]()

Leave a Reply