- Eid holidays slow down import activity in Turkiye

- Bangladesh mills hold off from fresh scrap bookings

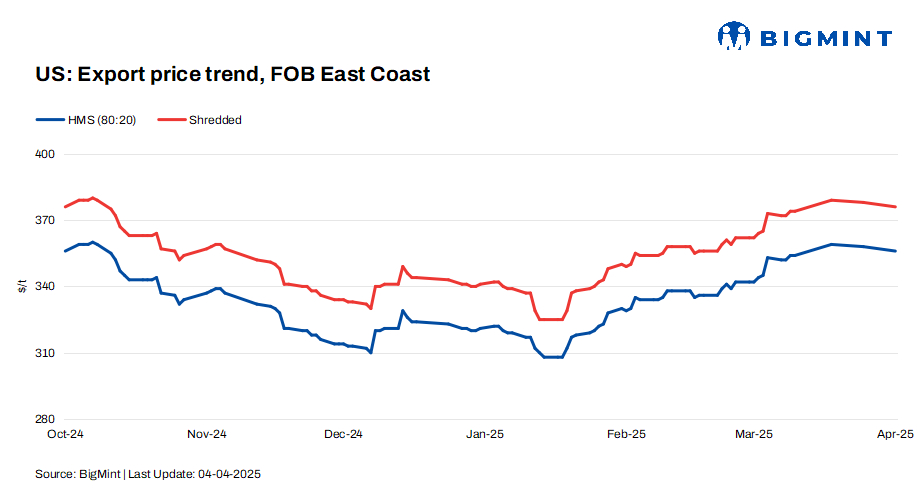

The US ferrous scrap export index inched down by $3/t w-o-w, largely driven by weak buying interest from key Asian and Turkish markets during the Eid holidays and trade-related uncertainties.

FOB assessments (US East Coast, bulk)

- HMS 80:20 decreased by $3/t w-o-w to $355/t.

Shredded dropped by $3/t w-o-w to $375/t

CFR assessments (bulk)

- HMS 80:20 was at $378/t CFR Turkiye, down by $3/t w-o-w.

- HMS 80:20 stood at $368/t CFR Vietnam, stable w-o-w.

- HMS 80:20 was at $384/t CFR Chattogram, stable w-o-w.

Updates on key importers

Turkiye: Demand for US-origin scrap in the Turkish market remained weak last week, largely due to the Eid holidays and ongoing uncertainty around tariffs and trade developments. Mills operated with caution, limiting fresh bookings, as they awaited clarity on broader economic measures.

Indicative offers for premium US HMS hovered at around $378-380/t CFR, but buying interest was muted, as mills remained sidelined.

Market participants noted that with only three working days during the week and most mills having already secured sufficient volumes for April and May shipments, there was little urgency to conclude new deals. The broader market remained quiet, as both buyers and sellers waited for clearer price directions. Until post-holiday demand picks up or significant price shifts occur, US-origin scrap is likely to face continued resistance from Turkish mills.

Bangladesh: Demand for US-origin scrap in Bangladesh stayed weak due to Eid holidays, with most mills running at reduced capacity and focusing on managing existing inventories. The ongoing slowdown in construction and infrastructure activity further dampened scrap procurement needs.

Offers from the US West Coast ranged at $385-390/t, but buyers showed limited appetite amid muted market sentiment. With Eid-related shutdowns extending into the next week, fresh deals are unlikely in the near term, and demand recovery is expected only after mid-April, when mills resume full operations.

Vietnam: Demand for US-origin scrap in Vietnam remained weak last week, with offers at around $370-374/t CFR failing to attract buyers. Mills opted for more competitively priced domestic scrap, while stable finished steel tags and a weakening yen further limited interest in imports.

Outlook

The US’s new 54% tariff on Chinese imports, effective 5 April, may weigh on global ferrous scrap demand by weakening China’s export-driven steel sector. Though direct steel trade with the US is limited, slower downstream activity in Asia could dampen scrap consumption and soften global prices, as buyers adopt a cautious approach amid trade uncertainties.

Leave a Reply