- Weak demand, lower billet prices pressure market

- Bangladeshi buyers remain away amid Eid holidays

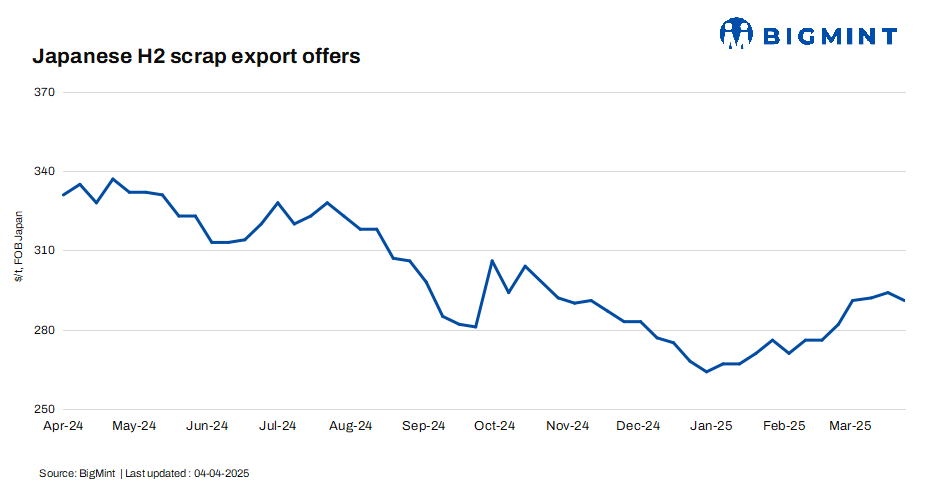

Japanese H2 scrap export offers fell by JPY 800/t ($5/t) w-o-w to JPY 43,500/t ($298/t) FOB Tokyo Bay. Weak demand and lower billet prices pressured the market, while many traders held back from offering ahead of the upcoming Kanto Tetsugen tender.

Market participants noted that there are still no strong drivers for an upward price movement. With large quantities of Russian billets previously booked at $448/t CFR, demand for scrap remains low.

Domestic FAS collection prices of H2 saw a slight increase w-o-w, to JPY 41,500-42,500/t ($284-291/t).

Other market updates

Vietnam: Vietnam’s imported scrap prices saw a slight decline from last week, as weak regional demand and lower billet prices continued to weigh on the market. Japanese H2 scrap offers to Vietnam ranged at $330-340/t CFR, down from the previous week’s $335-345/t. Buying indicatives from Vietnam were heard at around $330-335/t CFR, though overall buying remained sluggish.

South Korea: The combined ferrous scrap inventory of eight major South Korean steel mills rose 5.4% w-o-w to 767,000 t from 727,000 t.

Scrap iron inventory rose for the second week, driven by stockpiling amid lower prices. Stocks in the central region jumped 14% w-o-w to 378,000 t after a price cut on 3 April, while inventories in the south dipped 1.7% w-o-w to 389,000 t due to limited stocking amid production cuts.

Hyundai Steel’s Pohang plant resumed operations, boosting scrap consumption prospects. However, weak rebar demand led mills to cut production, with Hyundai Steel halting rebar output at Incheon for April.

Taiwan: Japanese H1:H2 scrap offers to Taiwan were heard at $330/t CFR, but supply remained limited. Sources indicated that traders might hold off on offering until Taiwan returns from the Qingming Festival and the Children’s Day holiday on 4 April.

As of 31 March, prices of US-sourced HMS 1&2 80:20 were reported at $318/t CFR Taiwan, edging down $2/t w-o-w, while Japanese-origin H2 stood at $335/t CFR Taiwan, higher by $10/t from two weeks earlier, according to a local source. There was no quotation for Japan-origin H2 over the previous couple of days.

Bangladesh: Bangladesh’s imported scrap market remained slow w-o-w, as buyers remained on the sidelines amid the Eid holidays, with mills operating at low capacity utilisation amid reduced steel consumption from end-users.

Japanese-origin H2 bulk prices stood at $370-375/t CFR Chattogram, unchanged w-o-w.

Outlook

Japanese H2 scrap export prices are likely to remain under pressure in the near term, with regional demand showing no signs of revival and billet prices staying competitive. The upcoming Kanto Tetsugen tender could provide some direction, but until then, cautious trading is expected. In Vietnam, sluggish buying and competitive billet prices suggest continued downside risks. South Korea’s rising scrap inventories and mixed regional trends indicate a cautious but watchful stance, especially with production cuts balancing out increased stockpiling. Taiwan’s market may remain quiet until post-holiday demand clarity emerges, although recent price movements show a mixed sentiment.

Leave a Reply