- Falling US coal output fails to support Atlantic prices

- Tighter supply in Indonesia, China keep Pacific prices firm

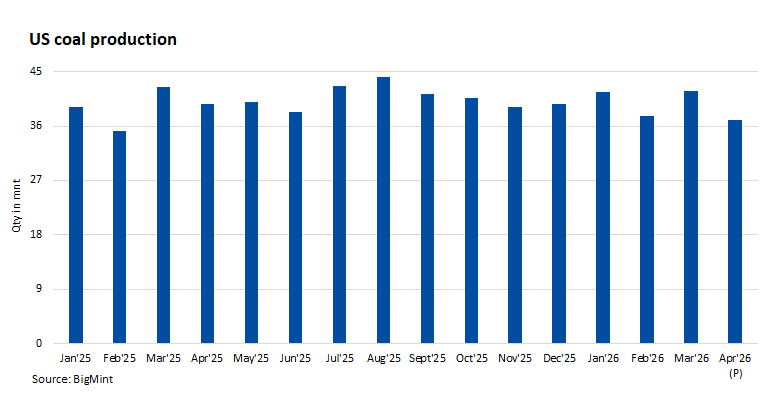

US coal production declined further in April, reinforcing the country’s long-term structural downtrend even as global thermal coal markets continue to move in sharply different directions.

US coal output was estimated at around 37-38 million tonnes (mnt) in April, down by roughly 10% m-o-m from March levels and lower y-o-y, reflecting persistent weakness across key producing regions, including the Powder River Basin and Appalachian coalfields. Cumulative production during January-April 2026 stood near 158 mnt, marginally lower compared with the same period last year.

While falling US output would historically have lent support to international coal prices, today’s market dynamics suggest a more fragmented picture. The global thermal coal market is increasingly shaped less by Atlantic supply fundamentals and more by regional drivers, particularly evolving conditions in Asia.

Atlantic markets lose momentum

In the Atlantic basin, thermal coal prices remain vulnerable despite structurally tighter global supply.

Delivered coal prices into northwest Europe have traded in the mid-$120s/t range, but recent price action suggests markets are struggling to sustain upward momentum. Prompt futures rallied intermittently on geopolitical headlines and energy market volatility but failed to maintain gains, reflecting fragile risk premia rather than genuine physical tightness.

The key challenge for Atlantic coal remains weak seasonal demand and improving gas market conditions.

European utilities are currently navigating a shoulder-season environment marked by moderate power demand, comfortable gas availability, and relatively adequate coal inventories at the Amsterdam-Rotterdam-Antwerp (ARA) hub. As renewable generation improves and coal burn remains constrained, inventories — while below historical norms — have not yet tightened sufficiently to create material procurement urgency.

A further easing in natural gas prices could add additional downside pressure.

Dutch Title Transfer Facility (TTF) gas prices have repeatedly struggled to sustain gains above the upper EUR 40s/MWh range as European storage injections continue steadily through late May. Although storage levels remain below year-ago levels, improving supply visibility and stable liquefied natural gas arrivals have reduced immediate concerns over fuel scarcity.

Should gas prices soften further, Atlantic thermal coal benchmarks such as API2 and DES ARA may struggle to find meaningful upside without a stronger weather or supply catalyst. Similarly, any easing in Middle East geopolitical tensions — particularly around Iran-related supply concerns — could unwind part of the energy risk premium currently supporting prompt fuel markets.

Asia’s tightness tells a different story

The outlook in the Pacific basin appears comparatively firmer.

Asian coal markets continue to draw support from supply-side uncertainty, particularly in China and Indonesia, even as demand remains seasonally mixed.

China’s domestic coal sector has shown fresh signs of tightening after coal output in several major producing provinces declined m-o-m during April. Market sentiment has also turned more cautious following a mining accident in late April, which prompted tighter safety inspections and heightened regulatory oversight ahead of the summer peak demand season.

While Beijing is expected to prioritise output growth to ensure adequate fuel availability, stricter inspections may temporarily slow supply responses, keeping domestic market balances tighter than previously anticipated.

At the same time, Indonesian export flows have remained uneven.

Seaborne shipments have occasionally lagged last year’s pace amid licensing bottlenecks, logistics frictions, and weather-related disruptions, limiting the pace of supply recovery for lower and mid-calorific value coal grades. This has helped preserve support for Pacific thermal coal benchmarks, particularly for cargoes into India, China, and other Asian import markets.

Summer demand remains the swing factor

Weather will ultimately determine whether current market tightness evolves into a stronger rally.

Early summer heat across parts of South Asia is already lifting electricity demand and thermal generation requirements. A hotter-than-normal season across Asia could tighten spot availability further, especially if China’s domestic supply recovery remains slower than expected or Indonesian cargo flows fail to accelerate meaningfully.

Conversely, benign weather conditions and smoother fuel availability could temper buying urgency and cap upside.

Diverging markets define the outlook

The widening disconnect between Atlantic and Pacific coal markets is emerging as one of the defining themes for the second half of 2026.

For now, Atlantic benchmarks remain neutral to slightly bearish near term, with prices exposed to softer gas markets and improving inventory conditions. By contrast, Pacific markets appear neutral to mildly supportive, underpinned by Chinese supply uncertainty, uneven Indonesian exports, and the prospect of stronger summer electricity demand.

The result is an increasingly decoupled thermal coal market – one where declining US production matters less than where the tonnes are needed most.

Leave a Reply